The term “equity capital” represents shareholders’ contributions to the bank. At every level, from the inception to the liquidation, a bank requires capital of different extents. In brief, we can say that capital is the nerve center of a bank.

All the activities of a bank are based on capital. Banks can’t operate their activities without capital. Even the promoters require capital to decide regarding the bank or perform preliminary activities. For this reason, supreme importance is given by law to capital-related issues.

Bank Capital Management: Types, Functions, Planning, Importance

What is Bank Capital?

The term bank capital refers principally to funds contributed by the bank’s owners, consisting mainly of stocks, reserves and those earnings that are retained in the bank.

Office equipment, human resources, etc., are required to initiate a banking business. Without capital, it is not possible at all. Even liquidation of a bank is impossible without capital. So, we can say that from the inception to the liquidation of a bank, capital plays a vital role.

Types of Bank Capital

Generally, bank capital is of two types:

- Primary Capital,

- Secondary Capital.

Elements of primary bank capital are;

- Ordinary/Common Stocks/Shares.

- Perpetual Preferred Stock.

- Capital Surplus (Share Premium) is provided by the owners.

- Undistributed profit.

- Mandatory convertible instrument/ debentures/bonds.

- Reserves for loan losses.

Elements of secondary bank capital are;

- Limited life preferred stock.

- Subordinated notes and debenture.

- Mandatory convertible instruments not eligible for primary capital.

How to Raise Bank Capital – Instruments of Raising Bank Capital

The instruments used by new banks or existing banks for collecting capital can be of two types:

- Equity-based instruments,

- Debt-based instruments.

Equity-based capital raising instruments are;

- Common stock

- Preferred stock

- Convertible Preferred stock

- Adjustable-rate preferred stock

- ESOP= Employee stock option plan

- ESOTS= Employee stock option trusts

Debt-based Capital raising instruments;

- Capital Notes

- Capital Debenture

- Convertible Debt

- Variable Rate Debt

- Option rare Debt

- Leasing Arrangement

Importance of Bank Capital

The banking business is based on trust. A lack of trust in the public regarding the activities of a bank automatically creates panic among depositors.

Well-structured banks’ premises, building layouts, use of high-technology increase the goodwill. Existing clients become satisfied and proud of this.

On the other hand, potential clients approach these banks for better service. These are possible only when the bank has a better capital base and does not face financial difficulty raising the above assets.

So, it is easy to understand that the importance of capital to the bank is enormous.

The importance of bank capital is discussed below:

Bank capital is required;

- To create & maintain public confidence.

- To provide resources for normal hazards and unforeseen contingencies.

- To act as a cushion in times of restricted monetary policy (i.e., when bank rate increases etc.)

- To raise awareness that bank owners have slaked along with the depositors in the supply of loanable funds.

- To obtain permission to open new branches, and

- To avoid punitive measures by the regulatory agency for reasons of capital inadequacy.

1. To create & maintain public confidence

Both existing and potential depositors are interested in those banks which own an adequate volume of capital. The depositors bear relatively less risk when the bank has an adequate volume of capital at its command.

Thus, capital adequacy increases the bank deposits creating & maintaining the confidence of the existing and potential depositors.

2. To provide for normal hazards and unforeseen contingencies

Banks may face unforeseen contingencies and financial risks in their day-to-day business. Adequate capital helps banks overcome unforeseen contingencies and losses from bad debt, non-performing customers, irresponsible employees, etc.

3. To act as a cushion in times of restricted monetary policy (i.e., increase bank rate, etc.)

The shortage of loanable funds arises when the government takes any restrictive monetary policy.

Providing loans according to the policy and target of the bank is crucial for its goodwill & income.

On the other hand, restricted monetary policy in the time of disbursing previously granted loan commitments adversely affects the loan activities of the bank.

Banks may be embarrassed to the existing and potential loan clients in such a case. To avoid this type of situation, banks should keep a sufficient amount of bank capital.

4. To raise awareness that bank owners have a stake along with the depositors in the supply of loanable funds

Bank depositors often think that the bank is operating the business by using only their deposited money. This presumption should not be correct if adequate capital is raised. To minimize the risk, deposit insurance schemes and statutory laws to maintain the minimum required level of capital have been enacted.

5. To obtain permission to open new branches

The banking regulatory authority takes the amount of capital to expand the banking activities and establish new branches. The debt-asset ratio passes within the control limit when a bank operates with adequate capital, keeping the banking business in a balanced order.

So, before expanding the operation or increasing the number of branches, the desired level of bank capital must be maintained. Otherwise, the bank regulatory body may refuse to give a license to increase the number of branches.

6. To avoid punitive measures for reasons of capital inadequacy

Government or bank regulatory bodies periodically check the bank’s statement and conduct field investigations by their representative officials to get information about the financial condition and adequacy of a bank’s capital.

When any bank violates the rules & regulations or guidelines, the bank is served a warning and or even punished by regulatory bodies. Thus, the bank must maintain capital less than the regulatory authorities to avoid such punitive actions and run the business with a reputation.

Functions of Bank Capital

Capital is significant for the activities of a bank. The functions of bank capital are discussed below:

1. To acquire the physical plant and necessities needed to render Banking Services:

Physical infrastructures like- office equipment, furniture, employees, etc., are required to start a banking business. Capital is inevitable to acquire these assets. The larger the amount of capital of a bank and the more attractive multistoried building a bank has more valued clients will be attracted.

2. To act as one of the sources of funds for loans and investments

The purpose of investment and loan activities is to increase the income of the bank. Banks may meet up a portion of the loan and investment demand by raising capital. Though most of the loan and investment activities are operated with the depositors’ money, sometimes the bank operates this activity with its own capital, especially at the preliminary phase of the banking business.

3. To protect the uninsured depositors in the event of insolvency and liquidation:

Recently, the bank regulatory authority has looked into serving an order of deposit insurance to ensure the safety of the deposits in a bank liquidation or failure; deposits that are not insured need to be returned from the bank’s capital resources.

4. To act as an unanticipated Loss Absorber

Hazards, business losses, and unforeseen contingencies like bad-debt misfeasance on the part of the employees when they occur at any time may call for a huge amount of money. Capital plays an important role in resolving such types of losses.

5. To serve as a regulator restraint

Govt or bank regulatory authority provides the direction of bank capital adequacy and capital reserve amount.

The bank regulatory authorities often inspect the bank to verify the level of capital maintained. If the bank fails to maintain the required level of capital, the regulatory authority takes legal and pecuniary punitive action against the bank.

A bank can avoid this type of punitive action by maintaining sufficient capital. According to a legal requirement, total capital cannot be less than 8% of the weighted average risky asset. Equity capital can never be less than 4% of the weighted average risky asset.

So, a bank needs to follow the statutory requirement to avoid difficulties likely to be faced in times of default.

From the above analysis, we can say that from the inception to the liquidation, at every step, capital is very much important for a bank.

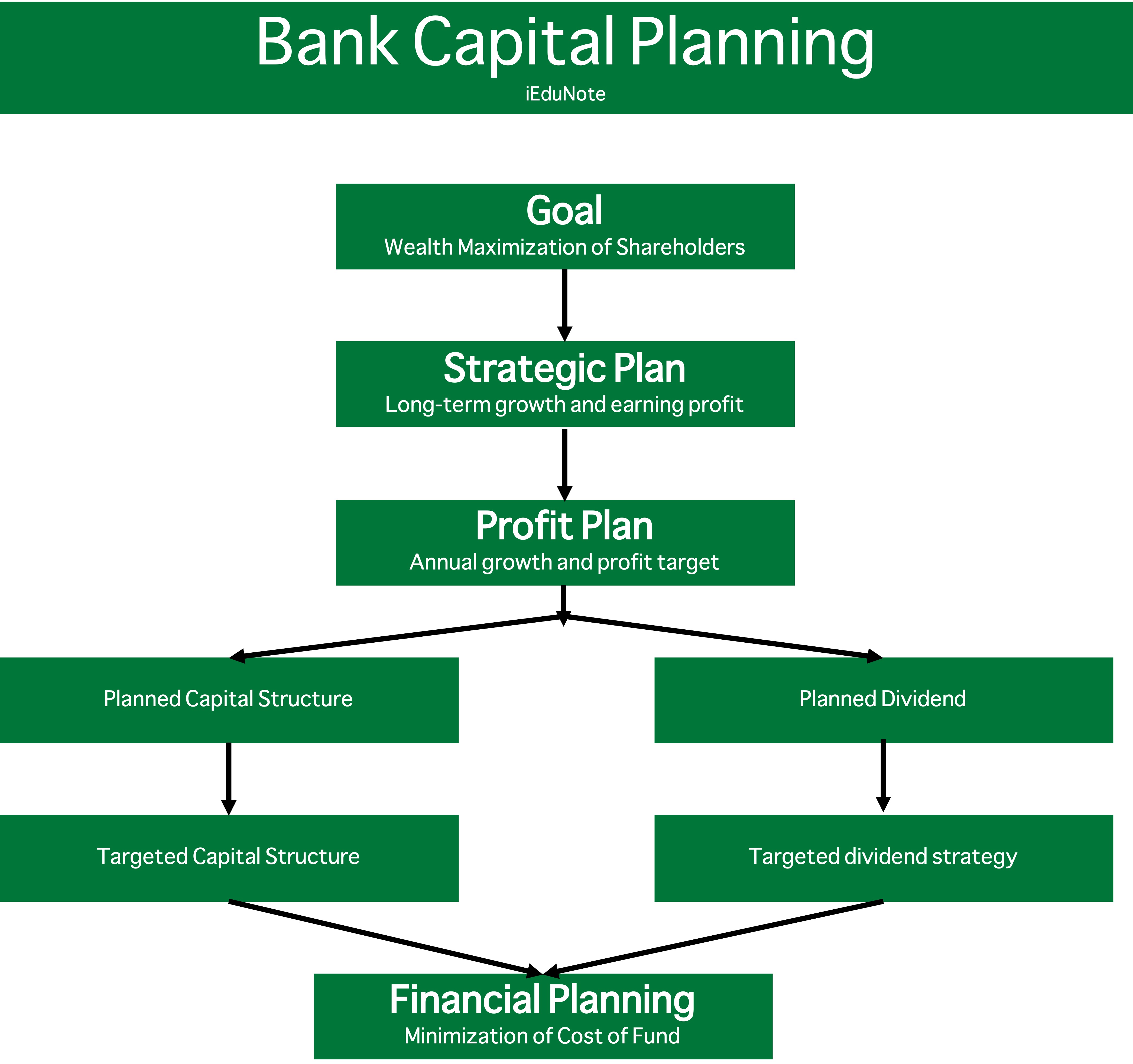

Bank Capital Planning

Bank capital planning is a procedure of determining the capital levels and capital mix of a bank. In a broad sense, bank capital planning is a process of assessing the total capital requirement for a particular time period and determining the portion of capital to be collected either from internal (owner’s equity) or external (debt borrowings) sources.

In determining bank capital structure, top priority should be given to attaining the profit target and controlling the risk by minimizing the cost of collecting funds.

The following diagram can easily understand this:

Both taking effective decisions regarding capital structure and efficiently implementing them is imperative to attain the wealth maximization goal. To implement various investment decisions of a bank, debt capital is required along with its equity capital.

So, we understand combining a bank’s equity and debt capital in a healthy proportion by capital structure.

Capital is inevitable to run banking activities. A bank mainly collects capital from four sources. These are Ioan, common shares/ stocks, preferred shares, and retained earnings.

Usually, every bank uses these four sources in different proportions in their capital mix. The bank’s capital structure is the combination of long-term debt sources like debenture, long-term loans, preferred shares, common shares, and different types of reserves.

Bank Capital Planning Process

Overall asset and liability management (A/L management) of a bank is a pan of bank capital planning process. The first step of the planning process starts from the expected profit earnings for the forthcoming years.

Capital planning is done when fixing the profit by forecasting future interest and non-interest income and interest and non-interest expense.

Generally, the bank capital planning process is accomplished by the following three steps:

- Generate Pro-forma balance sheets and income statements for the bank.

- Assume/select a dividend layout.

- Analyze the costs and benefits of alternative sources of external capital

The first step determines the funds required to finance the bank’s assets. The excess of expected assets over the expected liabilities is the equity capital.

Primary and secondary capital must equal the minimum statutory level of capital as usually stipulated by the regulatory authorities.

In the second step, funds to be collected from internal and external sources are forecasted. Dependency on external capital remains low if the dividend is not paid. If the dividend is paid, dependency on external capital increases.

Payment of dividends creates pressure on capital, while banks have to declare dividends to meet the expectation of the shareholders and to maintain goodwill in the market. Dependency on external capital varies with the rate of dividend.

In the third step, bank management needs to analyze the costs and benefits of alternative sources of external capital. According to risk management, too much dependency on an alternative should be avoided. But the possibility of taking any alternative sources to meet future needs should not be blocked.

Measures of Capital Adequacy of a Bank

Adequacy is a relative term. The amount of capital that is adequate for a bank may prove to be inadequate for another bank. The depositors of a bank often argue that the bank capital should be higher to minimize the risk of their deposited money.

On the other hand, the rate of dividends reduces if the capital is increased.

So, the owners of a bank often want to keep a lower capital level.

To eliminate the dispute between these two parties, bank regulatory authorities in the USA and several other western countries have promulgated the statutory level of bank capital by risky assets considering the interest of both the bank shareholders and the depositors.

Shareholders can reduce risky bank assets by employing efficient management through the board of directors. Thus bank shareholders can indirectly keep the bank capital at the expected level. A bank’s capital adequacy can be different depending on the working area, scope and time.

Risk adequacy differs from bank to bank because of bank size, time, quality of technical know-how, and differences in weighted risky assets of loans & advances. The lesser the possibility of recovering invested capital of a bank, the higher the risk will be.

- Quality of Bank Management

- Liquidity of Assets

- The history of earnings and retention thereof

- The quality and character of ownership

- The burden of meeting occupancy expenses

- The potential volatility of deposit structures

- The quality of operating procedures

- The bank’s capacity to meet the present and future financial needs of their trade areas considering the competition they face:

- Variation in the use of technology

- Need for replacement of assets

The measures of capital adequacy of a bank are briefly discussed below:

1. Quality of Bank Management

The extent of professional & technical ability, training, social status, etc., of the management of a bank highly influences its capital management. The more efficient and developed the bank’s management, the less capital it requires to carry out banking activities.

Honest and efficient bank officers carefully perform their expected activities. The main responsibility of bank officers is to choose the right and efficient borrowers. Personal and close monitoring of loans can keep the loan activities remain safe from becoming sick cases.

On the other hand, if deposit management is well and efficient, more loanable funds can be raised at a relatively low cost. Experienced and intuitive bank officers try to manage time deposits by avoiding volatile deposits.

Efficient management can increase funds by collecting quality time deposits. Investing in safe government bonds and securities can reduce the risk-based capital amount.

2. Liquidity of Assets

A bank requires the appropriate level of liquidity to meet the day-to-day requirement of cash. The more efficient a bank is in liquidity management, the less capital adequacy a bank will be. A bank can do profitable business even with lower capital if it can manage liquidity efficiently. A bank with more efficient liquidity management needs less money to maintain its liquidity position. So banks with efficient liquidity management can invest more in less risky earning assets.

3. The history of earnings and retention thereof

The more undistributed profit and history of successive profitability a bank has, the more capital its owners have.

In that situation, banks are not required to collect money from external interest-bearing sources as such continuous better-earning rates and increasing rates of retention of earnings will require fewer funds from shareholders as capital.

4. The quality and character of ownership

Suppose a bank has many shareholders, and each of the shareholders holds a few numbers of shares. In that case, the capital cannot be increased due to higher dividend expectations by the shareholders for any amount of profit.

On the other hand, banks, whose shareholders want to accumulate their capital by retaining their earnings, will have no capital adequacy problems.

Thus, the type of shareholders & their degree of expectation for cash dividends conspicuously determine the bank’s capital adequacy.

5. The burden of meeting occupancy expenses

The fixed assets of a bank or rented assets are considered non-productive assets of the bank. The more a bank spends on these non-productive assets like floor space and building, including furniture, fixtures, etc., the more capital it will require for comfortable operation.

Despite this, to attract customers and increase banks’ goodwill, some banks use luxurious and high-rent houses to operate their banking activities.

6. The potential volatility of deposit structures

If the deposit structure is volatile & risky, more liquidity deeds will command more capital. The more efficient a bank in deposit management is, the less it will collect sensitive & volatile deposits.

A bank needs to keep less cash if it has more time to deposit and efficiently predict the depositors’ withdrawal rate in terms of frequency and amount.

So, sensitive deposits and their ratio to total deposits play an important role in determining a bank’s capital adequacy.

7. The quality of operating procedures

The more efficient and perfect the operating procedure of a bank is, the more effective the day-to-day activities of a bank will be.

The banks with efficient operating procedures have less sensitive deposits and can effectively operate less risk-intensive loan activities.

And thus, such banks will require less capital than other banks operating with lengthy & time-consuming traditional inefficient procedures.

8. The bank’s capacity to meet the present and future financial needs of their trade areas considering the competition they face:

A bank carries out its business and social responsibilities for meeting the personal and business loan demand in the areas where the bank works, known as the command area of the bank. The extent of the severity of competition and demand for loans in the operation area largely determines the bank’s capital adequacy.

9. Variation in the use of technology

We are living in the age of technology. The bank which uses improved technology for providing quality service requires more capital than the banks which don t use such technology.

Instruments for e-banking, computerization, ATM, and protective arrangements will require more funds and more capital.

10. Need for replacement of assets

Fixed assets like land, building, furniture, machinery, and motor vehicles must sometimes be replaced because of their obsolescence and expiration.

This may cause demands for the huge fund. A bank that does such a replacement operation needs more capital than the other bank that does not require the replacement of assets.

Test of Capital Adequacy of Bank

The amount of capital adequacy varies from front bank to bank. It may also vary in the same bank with the change of the environment of banking.

4 types of capital adequacy tests have been more or less in use. These are:

- Measurement by ratios

- ABC measurement technique,

- Rule of 20 test

- Weighted Asset test

1. Measurement by ratios

The US Federal Reserve System first used a group of ratio-based tests in 1950. Later security analysts, commercial officers, and bank regulatory agencies experimented with the different ratios measurements. The capital deposit ratio was the first measurement used to determine capital adequacy. Mostly used four other ratios for the purpose arc:

- Equity capital to total assets

- Equity capital to risky asset

- Equity capital to total deposits

- Equity capital to loan and discounts

In addition to the above set of ratios, bank regulatory agencies and other interested parties have used another set of five ratios at different points in time. These are:

- Total capital to total assets

- Loans to total capital

- Classified assets to total capital

- Fixed assets to total capital

- Assets growth rate to capital growth rate

It should be mentioned that since 1970 Federal Reserve System, comptroller office of the US government, and Federal Deposit Insurance Corporation has been using additional 3 ratios:

- Rate of net sensitive assets /Total Assets

- Reserves for charge offs/Net Charge-offs

- Net Charge offs/loans

2. ABC Measuring

ABC is the acronym of “Analyzing Bank Capital.” In 1956, the Federal Reserve Board of the United States developed the rules for measuring bank capital adequacy. Those banks that have less liquid assets face the necessity of more capital. The measuring technique compares capital adequacy and liquidity.

The ABC rule was used until the advent of the “Test of capital adequacy based on risky assets.” It depicts that the adequacy of the capital varies with the liquidity requirement. The more liquid assets, the less the capital is required and vice versa.

Rule of 20 Test

In 1973 a bank specialist named GJ Vojta developed the rule of 20 test. The main features of this rule are-

Test of satisfaction for earning profits:

- To evaluate the level of quality of management, the classified problem loans must not be more than 50 percent.

- A bank’s assets or liabilities must not be concentrated on a single client or a single economic sector of commerce and industry.

- The total amount of capital must not exceed 20% of risky assets and must not fall below 5% of risky assets.

Test for examining possible losses:

The main factors through which the possibility of future loss of the bank is determined are:-

- Credit Risk

- Investment Risk

- Operating Risk

- Fraud Risk

- Liquidity Risk

- Fiduciary Risk

These risks can be analyzed in two ways-

- Normal losses: This type of loss occurs in a stable working environment. This loss can be managed from the bank’s traditional current income or surplus.

- Unexpected Losses: This type of loss occurs in an unpredictable economic situation. The extent of this loss is far greater than that of normal loss. A sufficient amount of capital, i.e., a large capital base, is required to recover such unexpected losses.

Generally, “the rule of 20 test” includes two types of tests:

- The earning test

- Test of coverage of unanticipated losses by capital funds

According to the canting test, undistributed profit must be double of unanticipated annual losses. The unanticipated annual losses are determined by calculating the moving average of the average losses for the last 5 years.

The assessment of the test is complicated. According to the test of coverage of unanticipated losses by capital funds, the unanticipated loss will be double the 5-year loan loss amount, at least. As such, the test failed to draw wide popularity.

Weighted Asset test

This test is described in section 6.2 of this chapter. This test is widely applied in many countries, including the USA and Bangladesh.

Arrangement of Safety of Bank Capital

From 1950 to date, we can find that despite using high technology in the banking industry, the number of failed banks cannot be reduced to zero.

Again, the causes of the failure of a bank are not too difficult to identify. The main reasons for bank failure are small capital, unqualified & inefficient bank employees, inaccurate loan policies, etc.

The safety of bank capital can be ensured in three ways:

- Internal Actions,

- The bank regulatory agencies take action, and

- Social awareness.

Internal Action

Internal action means taking the right action at the right time to control or at least minimize the factors that appear to pressure the bank’s capital. Some of these internal steps are indicated below;

- Reducing the pressure on capital through professionalism & quality of management;

- Before committing a large volume of transactions, a final decision is to be made after piously examining whether the transaction violates any rules or regulations;

- Efficient and honest bank officials should be assigned to analyze the loan proposals and to make the final decision regarding big loans or investments as the case may be;

- Based on favorably managing risky assets, take technically appropriate decisions while making investments in less risky securities in the light of creating a favorable atmosphere;

- In the deposit mix process, steps must be taken to keep the amount of sensitive/volatile deposits below a predetermined level; and

- Based on risk analysis, remain extra cautious in making loans and advances to multi-sector economic projects to reduce credit risks.

Steps taken by the regulatory bodies

- Necessary information and periodical statements relating to deposits and loans must be submitted to regulatory bodies, such as the Central Bank, Deposit Insurance Corporation, and other relevant agencies/organizations. Based on the careful analyses of these statements, any suggestions, advice & guidelines as and when provided by these agencies must be followed and put to practice immediately or without showing any excuse whatsoever;

- Deposits eligible for insurance must be insured by making regular insurance premiums to transfer the deposit risks to the insurance corporation. No attempt should be made to save premium money by not insuring deposits leaving deposits uninsured, and such default may cause a sudden problem for the bank.

- Moreover, the bank itself may seek advice from the appropriate regulatory agencies on some self-detected problems when faced and piously adhere to the guidelines provided by these agencies.

Social Consciousness

Some stakeholders or outsiders are interested in the bank’s growth, who often provide useful advice by observing the financial statements.

Much valuable advice of the interested parties, including auditors, be carefully considered, and those found useful must put to practice to avoid possible crises and complexities.

For example:

- Like all other companies, banks must be periodically audited by professional external audit firms. These firms, when conducting audits, usually detect irregularities in the maintenance of accounts, commitments of frauds, embezzlement, etc., done during the period under review. Responsibilities for such offenses are located, and appropriate corrective actions are to be undertaken without any loss of time;

- Taking necessary actions based on the recommendations when provided by the shareholders in an annual general meeting regarding the apprehended possible risks associated with capital, loans, and deposits;

- Taking necessary actions when weaknesses are detected based on the analytical judgments of the operations by the researchers regarding capital, loans, and deposit risks; and

- Taking proper initiatives to rectify the mistakes and discrepancies in the capital, loan, and deposit management as observed and identified by the reporters in the newspapers, journals, etc.