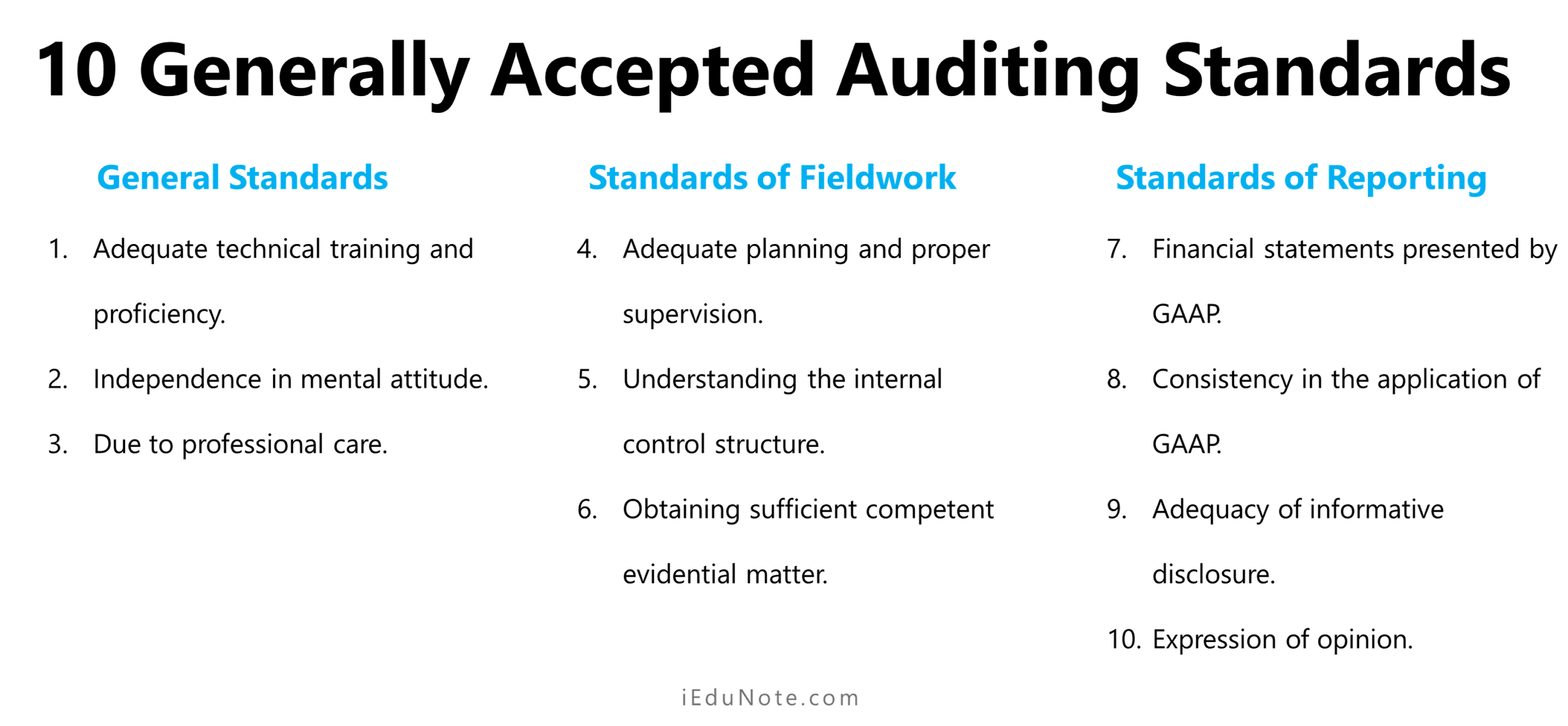

It is worth noting that the procedures performed in completing the audit have several distinct characteristics.

For instance, they do not pertain to specific transaction cycles or accounts; they are performed after the balance sheet date; they involve many subjective judgments by the auditor and are usually performed by audit managers or other senior members of the audit team.

The auditor’s responsibilities in completing the audit involve completing the fieldwork, evaluating the findings, and communicating with the client.

1. Completing The Audit Field Work

1. Making a Subsequent Events Review

Subsequent events are events and transactions that occur after the balance sheet date but before the issuance of the financial statements and the auditor’s report.

In effect, the subsequent events period extends from the balance sheet date to the end of the fieldwork.

During this period, the auditor is required by GAAS to discover the occurrence of any subsequent event that has a material effect on the financial statements.

However, the auditor has no responsibility to discover subsequent events between the end of fieldwork and the issuance of the audit report.

2. Reading Minutes of Meetings

The reading of minutes of meetings of stockholders, the board of directors, and its subcommittees may reveal information about matters that have audit significance. These should be read as soon as they become available.

3. Obtaining Evidence Concerning Litigation, Claims, and Assessments

In completing an audit following GAAS, the auditor must determine whether litigation, claims, and assessments are reported in conformity with accounting standards.

Management represents the primary source of such information, whereas a letter of audit inquiry to the client’s outside legal counsel is the auditor’s primary means of corroborating this information.

4. Obtaining a Management Representation Letter

The auditor must also obtain written representations from management regarding the matters that are either individually or collectively material to the financial statements.

Such a letter complements other auditing procedures and may reveal matters not otherwise discovered by the auditor.

It should be noted that the refusal by management to provide such a letter in effect limits the scope of the audit and could result in the auditor not issuing a standard audit report.

5. Performing Analytical Procedures

Performing analytical procedures at the end of the fieldwork is a required part of an overall review.

It assesses the conclusions reached during the audit and evaluates the overall Financial statement preparation.

The procedures are applied to critical audit areas identified during the audit and are based on financial statement data after all adjustments and reclassifications have been recognized.

2. Evaluating The Findings

After an audit team collects the facts and completes its investigation, it is time to determine its results.

For audits, the results are called reported audit findings.

The first step is to evaluate the evidence against the audit criteria. The evidence is the factual information collected or observed during the audit performance.

The audit criteria are the standards, procedures, regulations, or objectives the organization was audited against. The criteria represent requirements the organization must comply with.

Informing an opinion on whether the financial statements are presented fairly, in all material respects, and in conformity with the applicable financial reporting framework, the auditor should take into account all relevant audit evidence, regardless of whether it appears to corroborate or contradict the assertions in the financial statements.

In the audit of financial statements, the auditor’s evaluation of audit results should include evaluation of the following:

- The results of analytical procedures performed in the overall review of the financial statements (“overall review”);

- Misstatements accumulated during the audit, including, in particular, uncorrected misstatements;

- The qualitative aspects of the company’s accounting practices;

- Conditions identified during the audit that relate to the assessment of the risk of material misstatement due to fraud (“fraud risk”);

- The presentation of the financial statements, including the disclosures; and

- The sufficiency and appropriateness of the audit evidence obtained.

When evaluating whether the financial statements are free of material misstatement, the auditor should evaluate the qualitative aspects of the company’s accounting practices, including potential bias in management’s judgments about the amounts and disclosures in the financial statements.

Suppose the auditor identifies bias in management’s judgments about the amounts and disclosures in the financial statements.

In that case, the auditor should evaluate whether the effect of that bias and the effect of uncorrected misstatements results in a material misstatement of the financial statements.

Also, the auditor should evaluate whether the auditor’s risk assessments, particularly the assessment of fraud risks and related audit responses, remain appropriate.

3. Communicating With the Client

1. Communication of Internal Control Structure Matters

Communication of internal control structure represents significant deficiencies in the design or operation of the internal control structure, which could adversely affect the organization’s ability to record, process, summarize, and report financial data consistent with the assertions of management in the financial ‘statements.

The communication should be made promptly, either during the audit or after its conclusion.

2. Communicating Matters About Conduct of Audit

Communication with the audit committee requires the auditor to communicate certain matters about the conduct of the audit to those responsible for overseeing the financial reporting process.

Normally this responsibility is assigned to an audit committee of the board of directors or a group with equivalent authority, such as a financial committee.

The communication may be oral or written and may occur during or shortly after the audit.

When the communication is in writing, the report should indicate that it is intended for the audit committee, the board of directors, and, if appropriate, management.

3. Preparing Management Letter

Auditors observe many facets of the client’s business organization and operations during an audit engagement.

After an audit, many auditors believe it is desirable to write a letter to management, known as a management letter, that contains recommendations not included in the required communication with the audit committee.

These recommendations usually relate to improving the efficiency and effectiveness of the company’s operations. Management letters may include comments on:

- Internal control structure matters that are not considered to be reportable conditions.

- Management of resources such as each inventory and investment.

- Tax-related matters.