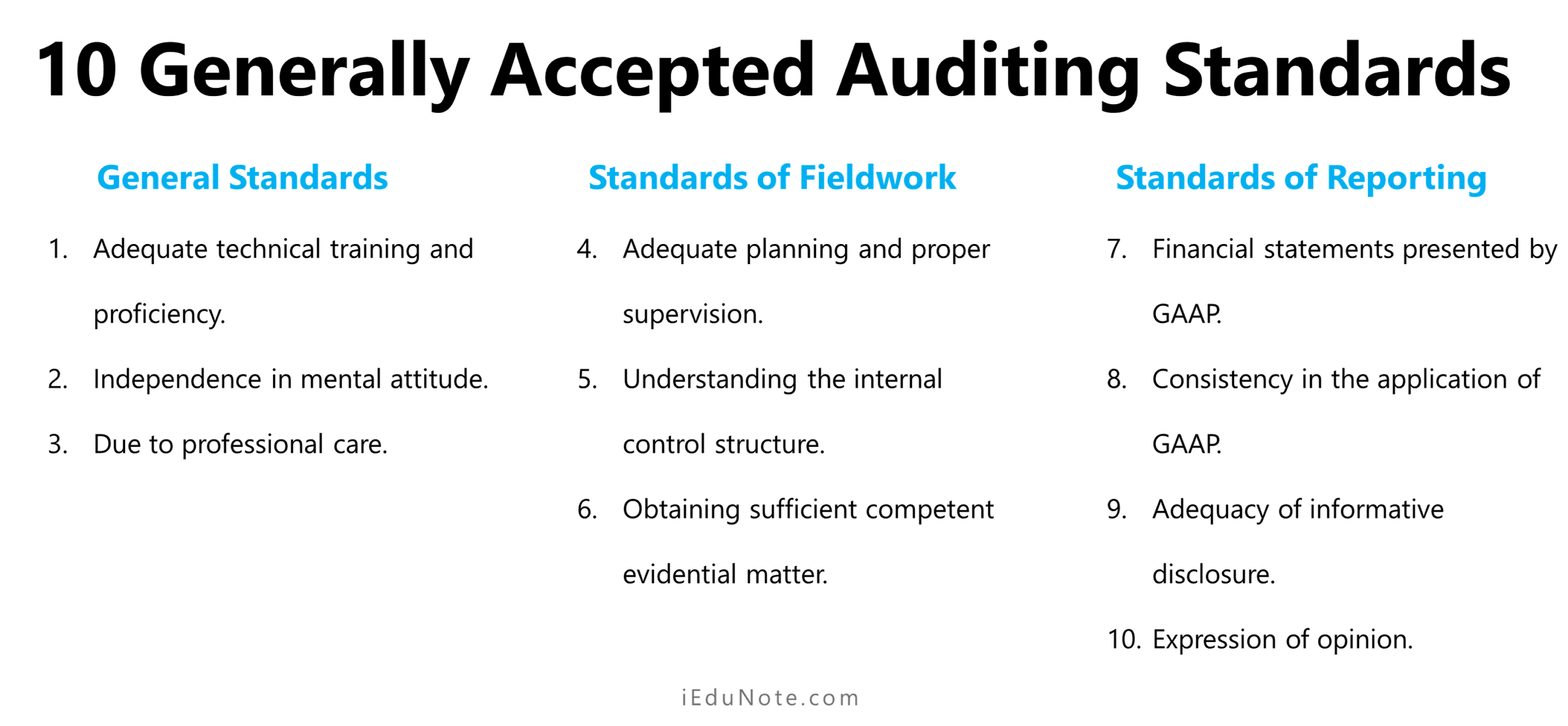

Audit evidence is the information the auditor collects and bases the audit on. Let’s try to find the meaning and definition of audit evidence, what is sufficient for appropriate audit evidence, and how to collect audit evidence.

What is Audit Evidence?

Audit evidence is all the information used by the auditor in arriving at the conclusions on which the audit opinion is based and includes the information contained in the accounting records underlying the financial statements and other information.

Auditors are not expected to examine all information that may exist.

Audit evidence, cumulative in nature, includes audit evidence obtained from audit procedures performed during the audit and may include audit evidence obtained from other sources, such as previous audits and a firm’s quality control procedures for client acceptance and continuance.

Evidence includes highly persuasive information, such as the auditor’s count of marketable securities, and less persuasive information, such as responses to questions of client employees.

An auditor must gather sufficient and appropriate audit evidence and test them to make a judgment of opinion. The use of evidence is not unique to auditors.

Evidence is also used extensively by scientists, lawyers, and historians.

In gathering evidence to support his assertions, the auditor is often confronted with two issues;

- What evidence will be relevant to assess an assertion with greater reliability?

- How much evidence is to be obtained?

Auditors are not expected to examine all information that may exist.

Sufficient Appropriate Audit Evidence

The auditor should design and perform audit procedures that are appropriate in the circumstance to obtain sufficient appropriate audit evidence. Sufficiency is the measure of the quantity of audit evidence.

Appropriateness is the measure of the quality of audit evidence, that is, its relevance and reliability in providing support for or detecting misstatements in the classes of transactions, account balances, and disclosures, and related assertions.

The auditor should consider the sufficiency and appropriateness of audit evidence when assessing risks and designing further audit procedures.

The quantity of audit evidence needed is affected by the risk of misstatement (the greater the risk, the more audit evidence is likely to be required) and the quality of such audit evidence (the higher the quality, the less the audit evidence that may be required).

Accordingly, the sufficiency and appropriateness of audit evidence are interrelated.

However, merely obtaining more audit evidence may not compensate if it is of lower quality.

Techniques for Gathering Audit Evidence

Some common ways of obtaining sufficient appropriate audit evidence to support the conclusion on the true and fair view of the financial statements.

Auditors used different methods of collecting audit evidence.

Cumulative audit evidence includes audit evidence obtained from audit procedures performed during the audit and may include;

1. Inspection

The inspection involves examining records or documents, whether internal or external, in paper form, electronic form, or other media, or a physical examination of an asset.

Inspection of records and documents provides audit evidence of varying degrees of reliability, depending on their nature and source and, in the case of internal records and documents, on the effectiveness of the controls over their production.

An example of inspection used as a test of controls is the inspection of records for evidence of authorization.

2. Observation

Observation consists of looking at a process or procedure performed by others, for example, the auditor’s observation of inventory counting by the entity’s personnel or the performance of control activities.

Observation provides audit evidence about the performance of a process or procedure.

Still, it is limited to the point in time at which the observation takes place and by the fact that the act of being observed may affect how the process or procedure is performed.

3. External Confirmation

An external confirmation represents audit evidence obtained by the auditor as a direct written response to the auditor from a third party (the confirming party), in paper form, or by electronic or another medium.

External confirmation procedures frequently are relevant when addressing assertions associated with certain account balances and their elements.

4. Documentation

Documentation is the auditor’s examination of the client’s documents and records to substantive the information that is or should be included in the financial statements.

The documents examined by the auditor are the records the client uses to provide information for conducting its business in an organized manner.

Because each transaction in the client’s organization is normally supported by at least one document, there is a large volume of this type of evidence available.

5. Recalculation

Recalculation consists of checking the mathematical accuracy of documents or records. Recalculation may be performed manually or electronically.

6. Reperformance

Reperformance involves the auditor’s independent execution of procedures or controls originally performed as part of the entity’s internal control.

7. Analytical Procedures

Analytical procedures evaluate financial information by analyzing plausible relationships among financial and non-financial data.

Analytical procedures also encompass such investigation as is necessary for identifying fluctuations or relationships that are inconsistent with other relevant information or differ from expected values by a significant amount.

8. Inquiry

Inquiry consists of seeking information from knowledgeable persons, both financial and non-financial, within or outside the entity.

An inquiry is used extensively throughout the audit and other audit procedures. Inquiries may range from formal written inquiries to informal oral inquiries.

Evaluating responses to inquiries is an integral part of the inquiry process.