The Basel Committee, established by the central bank Governors of the Group of Ten countries at the end of 1974, meets regularly four times a year. It has about twenty-five technical working groups and task forces, which also meet regularly.

The Committee’s members come from;

- Belgium,

- Canada,

- France,

- Germany,

- Italy,

- Japan,

- Luxembourg,

- Netherlands,

- Spain,

- Sweden,

- Switzerland,

- The United Kingdom, and

- The United States.

Countries are represented by their central bank and the authority with formal responsibility for the prudential supervision of the banking business where this is not the central bank.

The present Chairman of the Committee is Mr. Nout Wellink, President of the Netherlands Bank, who succeeded Mr. Jaime Caruana on July 1, 2006. Its Vice-Chairman is Mr. Nicholas Le Pan, Superintendent of Financial Institutions in Canada.

The Committee does not possess any formal supranational supervisory authority, and its conclusions do not and were never intended to, have legal force.

Rather, it formulates broad supervisory standards and guidelines and recommends statements of best practice in the expectation that individual authorities will take steps to implement them through detailed arrangements – statutory or otherwise – which are best suited to their national systems.

In this way, the Committee encourages convergence towards common approaches and common standards without attempting detailed harmonization of member countries’ supervisory techniques.

Rationale of Basel

Some fundamental objectives lie at the heart of the Committee’s work on regulatory convergence. These are:

Soundness and Stability

The framework should strengthen the soundness and stability of the international banking system.

Fair and Consistent

The framework should be fair and have a high degree of consistency in its application to banks in different countries to diminish an existing source of competitive inequality among international banks.

Establish Minimum Levels of Capital

The agreed framework establishes minimum capital levels for internationally active banks. National authorities will be free to adopt arrangements that set higher levels.

Capital Adequacy

The framework is mainly directed toward assessing capital with credit risk (the risk of counterparty failure).

In assessing bank progress in member countries toward meeting the agreed capital standards, the Committee will consider any differences in existing policies and procedures for setting the level of provisions among countries’ banks and in the form in which such provisions are constituted.

Ownership Structure

The Committee also provides guidelines for ownership structures and the position of banks within financial conglomerate groups undergoing significant changes.

The Committee will be concerned with ensuring that ownership structures should not be such as to weaken the bank’s capital position or expose it to risks stemming from other parts of the group.

Stabilizing Financial Market

This Accord is to improve the stability of financial markets by setting a floor for reserved capital held by the world’s largest banks; this will be referred to as the “Regulatory Capital” or “Solvency.”

Risk-weighted Assets

The committee also provides guidelines for risk-weighted assets and sets a benchmark for banks.

Basel Capital Accord-1

Major Findings of Basel Capital Accord

This is divided into three sections. The first two describe the framework:

- Section I – The constituents of capital

- Section II – Risk Weighting System

- Section III – Target Standard Ratio

Section I – The constituents of capital

- Core capital (basic equity): The Committee considers the key element of capital on which the main emphasis should be placed as equity capital and disclosed. The Committee has therefore concluded that capital, for supervisory purposes, should be defined in two tiers in a way that will have the effect of requiring at least 50% of a bank’s capital base to consist of a core element comprised of equity capital and published reserves from post-tax retained earnings (tier I). The other capital elements (supplementary capital) will be admitted into tier 2 up to equal to that of the core capital.

- Supplementary capital:

- Undisclosed reserves: Under this heading are included only reserves that, though unpublished, have been passed through the profit and loss account and are accepted by the bank’s supervisory authorities.

- Revaluation reserves: revaluations can arise in two ways:

- From a formal revaluation, carried through to the balance sheets of banks’ own remise.?, or

- From a notional addition to the capital of hidden values that arise from holding securities in the balance sheet valued at historical costs.

- Such reserves may be included within supplementary capital provided that the assets are considered by the supervisory authority to be prudently valued, fully reflecting the possibility of price fluctuations and forced sale.

- General provisions/general loan-loss reserves: General provisions or general loan-loss reserves are created against the possibility of losses not yet identified. They do not reflect a known deterioration in the valuation of particular assets. These reserves qualify for inclusion in tier 2 capital. General provisions/general loan-loss reserves that qualify for inclusion in tier 2 under the terms described above do so subject to a limit of 1.25 percentage points of weighted risk assets.

- Hybrid debt capital instruments: In this category fall, several capital instruments combine certain characteristics of equity and certain characteristics of debt. They are unsecured, subordinated, and fully paid up, not redeemable, and available to participate. Each of these has particular features that can affect its quality as capital.

- Deductions from capital: It has been concluded dial the following deductions should lie made from the capital base to calculate the risk-weighted capital ratio. The deductions will consist of goodwill, investments in subsidiaries engaged in banking, and financial activities not consolidated in national systems. The deduction for such investments will be made against the total capital base.

Section II – Risk Weighting System

The Committee considers that a weighted risk ratio in which capital is related to different categories of an asset or off-balance-sheet exposure, weighted according to broad categories of relative riskiness, is the preferred method for assessing banks’ capital adequacy. Committee believes that a risk ratio has the following advantages over the simpler gearing ratio approach:

- Provide a fairer basis for making international comparisons between banking systems whose structures may differ.

- Allows off-balance-sheet exposures to be incorporated more easily into the measure;

- It does not deter banks from holding liquid or other assets which carry low risk.

The framework of weights has been kept as simple as possible, and only five weights are used – 0, 10. 20, 50, and 100%.”

Categories of risk captured in the framework

There are many different kinds of risks against which banks’ managements need to guard. For most banks, the major risk is credit risk, that is to say, the risk of counterparty failure, but there are many other kinds of risk – for example, investment risk, interest rate risk, exchange rate risk, and concentration risk. The central focus of this framework is credit risk and, as a further aspect of credit risk, country transfer risk.

The Committee considered the desirability of seeking to incorporate additional weightings to reflect the investment risk in holdings of fixed-rate government securities – one manifestation of interest rate risk, which is, of course, present across the whole range of a bank’s activities on and off the balance sheet.

For the present, it was concluded that individual supervisory authorities should be free to apply either a zero or a low weight to claims on governments (e.g., 10% for all securities or 10% for those maturing in less than one year and 20% for one year and over).

Section III – Target Standard Ratio

In the light of consultations and preliminary testing of the framework, the Committee is agreed that a minimum standard should be set now, which international banks generally will be expected to achieve.

Accordingly, the Committee confirms that the standard target ratio of capital to weighted risk assets should be set at 8%, of which the core capital element will be at least 4%).

Bank capital essentially provides a cushion against failure. If bank losses exceed bank capital, the bank will become capital insolvent. Thus, the higher the bank’s capital, the higher the bank’s solvency.

Up until the 1990s, bank regulators based their capital adequacy policy principally on the simple leverage ratio defined as; “Leverage Capital = Capital / Total Assets.”

The larger this ratio, the larger the cushion against failure. The problem with the previous ratio is that it doesn’t distinguish between the assets according to their risks.

The asset risk can increase (increase the likelihood of insolvency), and the capital can stay the same if the bank satisfies the minimum leverage ratio. In other words, the leverage ratio sets the minimum capital ratio, not the maximum insolvency probability.

In 1988 the Basel committee on banking supervision’ introduced the Basel I accord or the risk-based capital requirements to deal with the weaknesses in the leverage ratio as a measure for solvency.

The 1988 Accord requires internationally active banks in the GIO countries to hold capital equal to at least 8% of a basket of assets measured differently according to their riskiness. The definition of capital is set (broadly) in two tiers.

Tier 1 is shareholders’ equity and retained earnings, and Tier 2 is additional internal and external resources available to the bank.

The bank has to hold at least half of its measured capital in Tier 1 form.

According to the debtor category, a portfolio approach was taken to measure risk, with assets classified into four buckets (0%, 20%. 50%, and 100%).

This means that some assets (essentially bank* holdings of government assets such as Treasury Bills and Bonds) have no capital requirement, while claims on banks have a 20% weight, translating into a capital charge of 1.6% of the value of the claim.

However, virtually all claims in the non-bank private sector receive the standard 8% capital requirement.

According to the Basel accord, the risk-based capital ratio can be measured as; “Risk-Based Capital Ratio= Capital / (Risk – Adjusted Assets).”

The 1988 Accord has been supplemented several times, with most changes dealing with off-balance-sheet activities.

Limitations of Basel Capital Accord 1

If the great merit of Basel I was its simplicity, it became criticized for the oversimplification of its risk categories. The limitation of the Basel Accord I is discussed below:

Vague Minimum Capital Requirement

Under the current Accord, capital requirements are only moderately related to a bank’s risk-taking. The requirement on credit exposure is the same whether the borrower’s credit rating is triple-A or triple-C.

Moreover, the requirement often hinges on the exposure’s specific legal form.

For example, an on-balance sheet loan generally faces a higher capital requirement than an off-balance sheet exposure to the same borrower, even though financial engineering can make such distinctions irrelevant from a risk perspective.

Lack of Risk Sensitivity

This lack of risk sensitivity under the current Accord distorts economic decision-making.

Banks are encouraged to structure transactions to minimize regulatory requirements or, in some cases, to undertake transactions whose main purpose is to reduce capital requirements with no commensurate reduction in actual risk-taking.

As an example, no capital charge is assigned to loans or loan commitments with a maturity of less than one year. Perhaps not surprisingly, 364-day facilities have risen in popularity.

Fails to Mitigate Bank Risk

The current system fails to recognize many techniques for actually mitigating banking risks. A closely related concern is that the current Accord is static and not easily adaptable to new banking activities and risk management techniques.

Costly

Some banks may have been reluctant to invest m better risk management systems because they are costly and would not provide tangible regulatory capital benefits.

Ineffective supervision

Although both banks and supervisors have been working to improve their assessments of capital adequacy, these assessments continue to center on comparisons of actual capital levels against the regulator) minimums.

Bank examiners continue to focus on these ratios partly because they are pan of the legal basis for taking supervisory Reflecting supervisors’ emphasis on regulatory capital ratios, financial markets and rating agencies tend to focus on them as well.

Consequently, in some cases, supervisors and even the banks themselves may have limited information about a bank’s overall risk and capital adequacy. It is difficult to ensure that banks and supervisors promptly respond to emerging problems in this setting.

Exposure to Risk

The Basel Accord is mainly directed toward assessing capital concerning credit risk (the risk of counterparty failure). Still, other risks, notably interest rate risk and the investment risk on securities, need to be considered by supervisors in assessing overall capital adequacy.

Ignore Fiscal Treatment

The Committee is aware that differences between countries in the fiscal treatment and accounting presentation for tax purposes of certain classes of provisions for losses and capital reserves derived from retained earnings may, to some extent, distort the comparability of the real or apparent capital positions of international banks.

Convergence in tax regimes, though desirable, lies outside the competence of the Committee, and tax considerations are not addressed in this Basel.

Ignore Operational Risk

Because of a flat 8% charge for claims in the private sector, banks have the incentive to move high-quality assets off the balance sheet (capital arbitrage).

Thus, reducing the average quality of bank loan portfolios. In addition to that, the 1988 accord does not consider the operational risk of banks, which becomes increasingly important with the increase in the complexity of bank activities.

Basel Capital Accord – II

The rationale behind the Enactment of Basel Accord – II

Since introducing the original Accord, banking (risk management practices, supervisory approaches, and financial markets) has undergone a significant transformation. Consolidation has produced concentration in the banking industry.

Advanced risk management techniques have evolved, resulting in more specific and detailed treatments of risk. A deficiency of the original Accord is its relative inflexibility in addressing these new realities, especially to large entities.

To address Basel I’s limitations, and the Basel Committee decided to draft a new version of the Accord in 1999. The Basel II Accord is expected to be finalized and published by the end of 2003 and implemented by the year-end 2006.

The Four principle rationales behind the enactment of the Basel II arc:

- Promotes soundness and stability of the global banking and financial system.

- Enhances competitive equality.

- Provides a more competitive approach to addressing risks and promotes best practices in risk management.

- The original accord failed to address Credit Risk fully and Operational Risk.

- Provides a more widely applicable approach to the capital assessment process.

- Basel II is more sophisticated in its treatment of offsetting factors that may protect a bank from loan losses arising from default, such as collateral, guarantees, securitization, and other credit derivatives.

- Basel II is designed to be a more sophisticated framework, reflecting the complexities of modem bank balance sheets.

- Under Basel II’s more sophisticated “Internal Ratings Based (IRB) approach,” banks with sufficient capability can calculate their own risk weightings using internal loan data rather than the standardized weightings specified in the framework.

Basel Accord II Overview

In April 2003, the Basel Committee released a “third consultative paper,” this document is the foundation of the New Capital Accord, Basel II. Comments on this document were submitted, and many valuable improvements have been made.

The result of the final improvements is a new framework described in the document “International Convergence of Capital Measurement and Capital Standards,” released in November 2005. The principle changes in the New Basle II Accord are enumerated here below:

- Banks are granted greater flexibility to determine the appropriate level of capital to be held in reserve against their risk exposure.

- However, banks must carry a greater responsibility to have effective and supervised systems to determine capital linked to this flexibility.

Also, carry a greater responsibility to their requirements to disclose their approaches and processes, which are applied to measure the required capital.

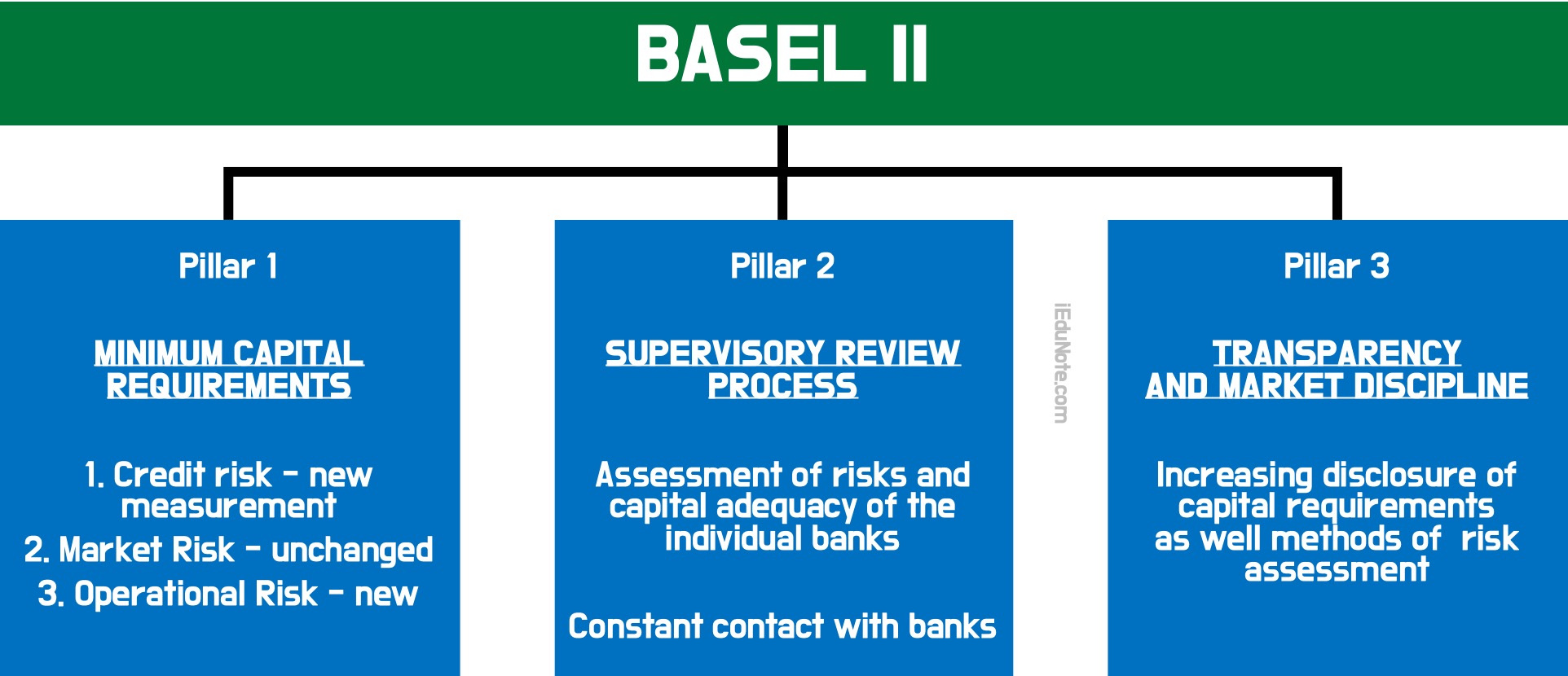

390 Figure 2: The three pillars- main elements of the new Accord

Capital Risk calculation under Basel II

Basel II at a glance

| PILLAR | Feature | Description | Impact |

|---|---|---|---|

| PILLAR 1 Minimum Capital Requirements | New methodologies for credit risk weights | Current Rules recognize only the highest quality collateral (i.e., cash) & guarantees (i.e., from OECD-incorporated banks). Basel II will recognize a wide range of mitigants, the benefits increasing with the bank’s sophistication. | Regulatory Capital will become much closer aligned to economic capital. There will he a change in the attractiveness to engage in certain business lines. Sophisticated hanks likely to sec reduction in required capital. |

| PILLAR 1 Minimum Capital Requirements | Recognition of Credit Risk Mitigants | Current Rules recognize only the highest quality collateral (i.e., cash) & guarantees (i.e., from OECD-incorporated banks). Basel II will recognize a wide range of mitigants, the benefits increasing with the bank’s sophistication. | Less sophisticated banks are likely to see an increase in required capital. Barriers to entry will increase. Sophisticated banks are able to align capital to support business goals tactically. |

| PILLAR 1 Minimum Capital Requirements | Introduction of specific Operational Risk | Current Rules require banks to hold capital against credit risk and market risk. Basel II is most likely to require a separate capital charge for Operational Risk (OR) | |

| PILLAR 2 Supervisory Review | Standard rules and powers for the regulators for policing the new more complex framework. Standardization ACTOSS countries for a set of minimum requirements | More bureaucracy for the industry to deal with. | |

| PILLAR 3 Market Discipline | Standardized requirements for the banks to disclose allocation and risk information to the markets beyond current accounting guidelines. | Investors will be better informed about banks’ risk and capital allocation. Shareholders may demand more information from non compliant Basel II institutions. |

fig-392

The soundness of the banking system is one of the most important issues for the regulatory authorities and the financial system’s stability.

The new accord Basel 11 introduces new approaches to capital adequacy that is appropriately sensitive to the degree of risk involved in a bank’s positions and activities and better measure the insolvency probability.

Basel II also introduces two new pillars; the review process and market discipline.

The two new pillars are introduced to assess the availability of the minimum requirements to implement the new approaches suggested in the accord and help market participants better understand banks’ risk profiles and the adequacy of their capital positions.

Weaknesses of Basel Accord II

Unfortunately, the new framework has several fundamental weaknesses. These are discussed below.

- Relies on Banks’ Own Risk Estimates

- Regulatory Arbitrage: It relies on banks’ own risk estimates. This is not incentive The review was prompted largely by observing banks in large financial centers increasingly circumventing the rules by regulatory arbitrage. The conclusion that the Committee came to at the beginning of the process was dial differences between regulatory and economic capital caused regulatory arbitrage. The way to eliminate regulations at bitrate was to make the regulatory rules converge on economic capital, that is, to make the rules risk-sensitive. “The Committee expects dial the New Accord will enhance the soundness of the financial system by aligning regulatory capital requirements to the underlying risks in the banking business and by encouraging better risk management by banks and enhanced market discipline, said the BCBS Secretarial (2001). Given the flood of regulatory arbitrage, this was the obvious conclusion draw, but it was wrong. The review has run into severe difficulties as a result. Because they have limited liability, banks shift risk to others but keep the reward and benefit much from the risk.

- Agency Problem: Banks also suffer from internal agency problems that induce their trader and credit officers to seek risk. Banks may manage their risks perfectly for shareholders but pose too much risk to others. A set of rules designed to eliminate the private incentives for regulatory arbitrage will not reflect the social risks. There should be incentives for regulator/ arbitrage ‘Risk-sensitivity’ if it means sensitivity to privacy risks, which is, therefore, the wrong goal. Instead, capital requirements should be related to social risk.

- Insufficient Private Risk Measure: Ranks private risk measures need to be adjusted to measure social risk. The value at risk roles, for example, multiply banks’ risk estimates by a factor of at least three. This can help correct failure externalities, albeit only under the wrong assumption that all talk failures pov the same risk to the system. However, when their own estimates are used to set capital, banks have an incentive to manipulate them. There are two protections against this distortion: ex-pint punishment for bad model performance and minimum standards judged by supervisors. Inherent data problems rule out the possibility of an automatic penalty function, and so the regime relies entirely on an increasingly baroque set of supervisory standards. Supervisory judgment is prone to failure. These protections will therefore be insufficient.

- Cannot Protect the System: Even if the incentives to manipulate the estimates can be corrected, there is a further problem. What protects the individual bank may not protect the system. Important properties – such as risk, correlations, liquidity – of the very system that the Basel Committee is trying to protect are not exogenous but defined by the collective behavior of banks and other financial institutions If banks manage risk in the same way shocks, news, and changes of opinion have a greater effect.

- Risks Derive from Bunks Behavior: Danielvwn. Shin and Zigrand (2002) show that adding a value at risk constraint affects the demand for assets, hence prices and price distributions. Their simulations suggest that general use of VaR lowers asset prices, increases their volatility, and increases the amplitude and duration of asset price response to large shocks. The same authors compare the fallacy of using policy purposes models that assume homogeneity of risk to the Lucas Critique. The risks derive from banks’ behavior and are not invariant to changes of regime.

- Lack of Better Risk Management: Regulators have not explained or tested the claim that using sophisticated quantitative models represents “better risk management” from the point of view of anyone but bank shareholders. Yet so confident is the Committer that models are better fit the new framework contains a capital incentive to move to the more sophisticated approach. For example, regulatory capital on a given portfolio will rise during downturns and fall during upswings, increasing the amplitude of economic cycles. This is because banks prefer to estimate risk over short horizons. Minimum data requirements do not cover a full cycle nor docs the forecast horizon. ‘Risk-sensitive’ rales will reward short-term lending, reducing the extent to which bank systems provide liquidity insurance to customers.

- Ineffectiveness of IRB Approach: The new framework, in which several approaches to credit and operational risk are available, replaces one form of regulatory arbitrage with another. The 1RB approach generates higher capital requirements than the standardized approach on lower-quality assets but lower requirements on higher-quality assets. Banks on the IRB approach may branch into jurisdictions where only the standardized approach is offered or vice versa. Adverse selection is seen as a price worth paying to achieve a framework applied by different banks and contains incentives to improve risk management. But if the IRB approach is not a better form of risk management from a social perspective, these costs may not be worth bearing.

- Fails to achieve its objectives: The second problem is that supervision may fail to achieve its objectives for any one of a large number of reasons.

- Lack of Skill, Power, and Incentives of Supervisors: Supervision has two advantages over formal regulation: supervisors use a broad range of information, notably of a soft, subjective nature: and they generally try to encourage improvements in risk management, which is for many risks a more efficient form of insurance than capital. However, in reality, supervisors may not have the skill, the power, or the incentives to supervise effectively. A supervisory regime such as Basel 2 requires powerful yet benevolent supervisors, the stock of which is supervision. On the other hand, it requires bureaucrats to exercise discretion, which may be used for good or ill. Therefore, the effectiveness of supervision depends on supervisors’ incentives and others such as bankers, politicians, and auditors. These incentives are affected by formal constraints, such as the law. But also by informal constraints of culture and norms, which vary across countries and persist over time. It is easy to build incentive mechanisms that fail to achieve regulatory objectives and difficult to build mechanisms that succeed. Organizational structures give even the most public-spirited supervisor reasons to misbehave.

- Lack of Access to Information: The power of supervision also depends on convention and norm, rather than on formal law; the tools of persuasion are subtle, and persuasion is difficult to monitor Supervision is intrinsically interpersonal, and human relationships can distort Furthermore, supervision is a complex activity in which the supervisor acquires and processes a great deal of information and makes decisions under uncertainty. Rationality is bounded. Moreover, even the richest supervisory agencies possess scant information about the relationship between supervisors’ actions and bankers’ behavior. Whether supervisory actions are effective or entirely superstitious is not known. In summary, the new regime is founded on a largely untested belief that supervision works. It is not robust to supervisor failure.

- Problems of Supervisor Approach: A shift towards banks’ internal risk measures and supervision implies a shift from rules to This has hugely important implications barely considered by the Committee. Standards work better in some jurisdictions than others. High-level principles and qualitative standards delegate to bureaucrats the task of giving content to the law. Not all legal and political systems can easily accommodate this delegated administrative approach. Supervision is inherently flexible and individualistic. There is great scope for unfairness; indeed, it is hard to apply judgment fairly, particularly where different individuals judge different cases, as is inevitably the case in supervision. The same issues arise with model recognition. There is no guarantee of consistency even within countries. The supervisory approach, therefore, creates some overwhelmingly difficult problems of law, politics, and equity.

- Cannot serve the primary purpose of the international capital adequacy regime: The primary purpose of the international capital adequacy regime is to protect against international competition in laxity (Kapstein. 1989), and the new regime will fail to achieve its purpose Regulators impose externalities on each other because banks may branch across borders under home country regulation, affecting competitive conditions in other countries. Regulators respond strategically to other regulators’ laxity by increasing their own. The 1988 Accord appears to have reversed the long-term trend towards lower capitalization.

- Standards are not contractible: Another regulator’s standard can only be observed by observing both the formulation of the standard and every decision and the information used to give content to the standard in every case. Therefore, low regulatory and supervisory standards are easy to disguise, as the IMF has observed. Peer pressure will have a less disciplinary effect in the new world than in more easily observable, rule-based regimes like the 1988 Accord. And markets have neither the information nor the incentives to punish those inadequately supervised.

- National discretion: The number of areas where national regulators choose between different options has jumped sharply. National discretion is useful only when Basel Committee members cannot agree on a single approach. So by a revealed preference argument, they can be expected to use that discretion differently. National discretion is equivalent to a hole in the international regime. A national discretion checklist recently published as a companion to a Basel Committee survey lists 44 areas of national discretion. Arguably, it no longer makes sense to say that member countries are joined with one Accord 20. When it comes to Pillar 2. there is little desire for coordination. Institutional arrangements and attitudes to supervision differ widely across countries, and there is little common understanding of the role and purposes of supervision.

- Excessive faith in disclosure requirements: The final problem is excessive faith in disclosure requirements. The modem rationale for bank regulation is based on asymmetries of information and externalities. Banks know more than their depositors and regulators and less than their borrowers. Disclosure requirements are that they reduce the asymmetries Disclosure may not have the desired disciplinary effect. A supply of accurate and timely information is necessary but not sufficient to discipline bankers (Karacadag and) Taylor, 2000). There are several steps in the process of market discipline, and all may fail.

- Costly: Market participants must change their behavior in response to new information. Lamfalussy (2000) reports that bank lenders ignored relevant information in the public domain, notably BIS statistics showing a build-up of external debt and a shortening of its maturity for some time before the Asian crisis hit. (The 1996 BIS Annual Report noted that Thailand had become the biggest debtor in the world.) They must acquire, process, and act on information. This is costly – and may be subject to increasing marginal costs – and so participants will not act hyper-rationally but with ‘bounded rationality.’ Satisfleers use rules of thumb. Participants must also be incentivized to acquire and process information, so they must believe themselves to be uninsured; such a belief would be irrational in many countries.

- Cannot Create Market Efficiency and Discipline: The market price of bank liabilities must reliably reflect participants’ judgments of the ‘fundamental’ risks of the bank rather than estimates of other people’s judgments. Market efficiency requires traders unconstrained by liquidity constraints or risk-aversion and willing to trade against noise traders. Even when the market disciplines, it does not necessarily do so beneficially. Expectations about average opinion drive markets. There is no reason to assume that ‘average opinion’ should become more stable with more information. In fact, more information can reduce heterogeneity among participants. Market participants react to public information by revising their estimates of fundamentals and revising their estimates of others’ actions, which also depend on public information. As a result, they place too much weight on public information, overreacting to noisy public signals.

- The problem of overreaction: Regulators are well aware d the problem of overreaction when it comes to suggesting that their own assessments of banks (CAMELS ratings, individual capital requirements) might be published. In Europe, the latest draft directive (European Commission Services. 2002) Article 128 states that individual ideal capital requirements above the minimum shall not be published. The IMF/World Bank assessments of countries’ financial sectors are not generally published for the same reason.

- Lack of Corporate Governance Standards: Foe bank managers to respond to market discipline by reducing risk, their personal welfare must fall with the price of the bank’s liabilities. This requires strong corporate governance standards.

In the new regime, market participants will be required to understand each bank’s risk measurement system and compare banks’ risks. Somehow correct for differences in reporting systems.

They will also be expected to use the soft information required in Pillar 3 to correct supervisors’ different standards. The Basel 2 disclosure requirements embody an Optimistic view of the benefits of greater disclosure.

Comparison between Basel Accord I and Basel Accord II

The Bank of International Settlements’ goal with the original Accord was to level the playing field between banks of all sizes across different countries by regulating capital requirements.

Conversely, Basel II offers significantly more sophisticated approaches for capital allocation and rewards organizations that are capable of implementing such sophisticated methods

3asd U utilizes three mutually reinforcing pillars to support its approach to capital allocation:

- Minimum Capital Requirements.

- Supervisory Review.

- Market Discipline.

| Points of Difference | BASEL I | BASEL II |

|---|---|---|

| Minimum Capital Requirement | The definition of capital tn Basel D v .11 not modify and tiiat the minimum raucs of capital to nsk-weighted assets including operational and market risks will remain 8% for local capital. Tier 2 capital will continue to be limited to 100% of Tier 1 capital The main changes will come from the inclusion of lhe operational nsk and the approaches to measure the different kinds of risks. | But according to the Basel 1 the risk-based capital ratio can be measured as Total Risk – Based Capital Ratio = Capital / (Risk – Adjusted Assets) |

| Risk Sensitivity | Basel I Accord sets a capiul requirement simply in terms of credit risk (the principal risk for banks, though the overall capital requirement (i.e., the 8% minimum ratio) was intended ro cover other risks as well. | To introduce greater nsk sensitivity, Basel IT introduces capital charge for uperatic-nal risk (for example the risk of loss from computer failures. poor documentation or fraud) Many mayor banks now alkx ne 20 or more of their internal capital tn operational risk. |

| Risk weights | Under Basel I individual risk weights depend on a board category of borrower. | Under Basel II the nsk weights are to be rerined by reference to a rating provided by an external credit assessment institutions (such as a raring agency) that meets strict standards or by relying on internal rating based (IRB) approaches where the banks provide the inputs for the risk weights. Both the external credit nsk assessment and the internal rating approaches require credit information and minimum requirement the hanks have to fulfil. |

| Grater Incentives to Beaks | But Basel 1 cannot create such an Incentive to Banks. | According to Basel II Changes to the minimum capiul requirements expected that the amount of capital currently required co be held by hanks will change dramatically. Some large sophisticated banka may find a significant surplus created by rhn change. This could provide capital tor repatriation as well as serving an incentive for addincrial M&A activities. |

| Reduce Large Basks Dominance | During the period of Basel I the gap between the largest, most sophisticated banks and the rest will continue to grow. As evidenced by previous industry consolidations, global “super banks’ could start to dominate many business lines. | This disparity may make it less attractive for institutions considering an entrance into this market after implementation or Basel II. |

| Category of Borrower | Under Basel 1 individual risk weights depend on the board category of borrower (i.e. sovereigns, banks or corporate). | Under Basel 2 die risk weights are to be refined by reference to a rating provided by an external credit assessment institution (such as a rating agency) that meets strict standards. For example, for corporate lending, die existing Accord provides only one risk weight category of 100% but the new Accord will provide four categories (20%, 50%. 100% and 150%). The following table illustrates the relation between the risk weights and credit assessment for corporate lending. Banks’ exposures to die lowest rated corporates are captured in the 150% risk-weight caterogy. 150% risk-weight caterogy assigned for example to unsecured portions of assets that are past due for more than 90 days, net of specific provisions. Similar frameworks for sovereigns and banks credit risk weighs will be applied. |

| Challenge conventional wisdom | Basel I encourages conventional wisdom in Business line & it encourages basic corporate banking. | Basel II will challenge conventional wisdom behind business lines, as the profitability of areas such as basic corporate banking could be transformed. Banks will develop new strategies to address these new realities. |

| Employment Economic Capital Model | Basel I does ignore RAROC model | It is expected that there will be a greater alignment of economic and regulatory capital, encouraging the industry to better price and manage risk. Many banks already employ economic capital models such as RAROC (Risk Adjusted Return on Capital) to price risk in transactions. Basel II attempts to bring these two numbers (economic and regulatory capital) closer together. |

| Supervisory Review | In Basel I the risk weights were fixed and the implementation of the accord was straightforward. | In Basel I the bank can choose from a menu of approaches the credit, market and operational risks. This process of choosing the approach requires the review of the availability of the minimum requirements to implement the approach. In addition to that, in IRB approaches the risk weight 15 computed from inputs from the bank (like the probability of default). It is necessary in this case to make sure that the hank inputs are measured or estimated in an accurate and robust manner. Basel committee suggests four principles to govern the review process which was discussed in the previous part |

| Market Discipline | This pillar does not exist in Basel I | The third pillar in Basel II aims to bolster market discipline through enhanced disclosure by banks. Effective disclosure is essential to ensure that market participants can better understand banks’ risk profiles and the adequacy of their capital positions. The new framework sets out disclosure requirements and recommendations in several areas, including the way a bank calculates its capital adequacy and its risk assessment methods. The core set of disclosure recommendations applies to all banks, with more detailed requirements for supervisory recognition of internal methodologies for credit risk, mitigation techniques and asset securitization. |

The new Basel Accord and Developing Countries

1. The supply of external funds

a) Cost of External Borrowing

A change of regime is likely to affect bank lending in at least three important ways: price, maturity, and volatility. The three are connected. Because lenders can withdraw costlessly from short-term debt, the change in the supply of credit in response to a shock is greater if the debt is short-term.

So, short-term debt generally carries liquidity risk. On the other hand, since the term structure of rates is average upward-si oping, it is usually cheaper to borrow short-term.

The new Accord is likely to change the cost of external borrowing for many governments and banks in developing countries.

Risk weights for sovereign or interbank lending in the 1988 Accord are based on OECD membership and external or internal credit quality ratings in the new regime. In the new approaches, loans to some countries, notably Turkey, will attract higher risk weights than they do at present.

On the other hand, borrowers in highly-rated countries outside the OECD, such as Botswana, will benefit.

That is not an unintended side-effect. The changes are designed to improve bonks’ incentives to distinguish between different risk levels and thus allocate credit more efficiently. Borrowers should consider fave incentives to improve their credit rating rather than to join the OECD.

b) Maturity of Financial Flows

The second potential impact is on the maturity of financial flows. The Basel Accord favors short-term lending to non-OECD banks. Intel bank lending of up to one year (in foreign currency) receives a 20% risk weight, lending over a year 100%. Therefore, if Atami changes behavior, it will shorten the maturity profile of lending to non-OECD banks, increasing these borrowers’ liquidity risk.

c) Volatility of Flows

The third impact is on the volatility of flows. Private capital flows are cyclical and unstable. The proximate cause of cases is a sharp reversal in net private capital flows.

Reversals of private capital flow as a proportion of GDP amounted to 12% in Mexico 19X1-3. 6% in Mexico 1994-95. 20% in Argentina 1982 83. and 7% in Chile 1981-83 (Ocampo. 1999).

In summary, bank lending from industrial countries is still likely to be weighted towards the short term and maybe even more volatile,

2. Bank Regulation in Developing Countries

If implemented by local regulators, Basel II will also affect intermediation by domestic institutions. Let’s find out whether the Basel 2 regime is appropriate for developing countries’ circumstances.

There are several differences between high-income and developing countries relevant to the prudential regime in developing countries.

The economic climate is riskier and subject to greater uncertainty: financial agents hast greater opportunities and incentives to engage in redistributive rather than productive activities: and most have lower skills.

In Developing Countries;

- The economic environment is riskier.

- Currency and debt crises are more frequent.

- The constraining behavior of the institutions is weaker, and financial actors have private interests that diverge from so to interests. Law and its enforcement are often weaker.

- Weak enforcement may be caused by low supervisory resources, collusion, or forbearance by the regulator, but it often arises to want support from the government or judiciary.

Nature of Application of Basel Accord

This official position is that countries are under no obligation to comply with an Accord to which they haw not contributed hit are encouraged m do so.

In practice, the incentives to comply are stronger than is generally recognized. Over a hundred countries claim to have implemented the Accord. There are several possible explanations:

- Official sector discipline

- Market discipline

- Market access requirements

- Reputation

- International spillovers

- Production efficiency

Crises to Overcome in the Developing Countries

Caprio and Honohan (1997), reviewing the common elements of banking crises, argue that; “a strategy for the prudential policy must address three main weaknesses: the impossibility of fine-tuning bank safety margins in the uncharted territory that is banking in the developing world: the need to provide insulation against the large shocks to which these economies are prone; and the lack of enforcement that results from the concentration of political power in many such countries.”

In the same spirit, they propose the following Principles:

Reductionism and holism

The banking system is made up of financial institutions, some of which are very large. These institutions interact directly and affect each other indirectly through their behavior. The system has properties, such as market liquidity and interconnectedness, that are hard to understand by observing an individual bank.

Liquidity requirements could be used for the banking system capital requirements for depositors. However, both tools can be used to achieve both objectives; there are significant economies of scope.

In summary: regulators and supervisors should pay more attention to the systematic impact of their interventions.

Carrot and stick

Bank shareholders and managers do not bear all the consequences of their risk-taking. Without fear of loss, bankers will seek risk. The objective of a prudential regime is to restrain bankers if their risk appetites are excessive.

Anything that does that is incentivecompatible. And. since all prudential regulations designed to limit risk-seeking are imperfect, bank managers will seek ways to circumvent them.

In summary: regulators must punish failure and reward success. Risk sensitivity is neither necessary nor sufficient.

Boom and bust

Endogenous booms and busts characterize a liberalized financial system. There is too much lending, and then too little. In upswings, risks are underpriced, and in downswings, they are overpriced. Easy credit encourages asset price inflation; more valuable asset prices can be used to secure more credit, and so on.

In the downswing, the borrower’s ability to repay diminishes while the unsecured exposure increases due to falling collateral values. The risks revealed in the downswing are accumulated in the years of fat cows.

In summary: by varying rules rather than supervision, regulators should lighten banks’ belts in good times and loosen them in bad.

Rules and standards

Rules exist to prevent people from harming others, but they do so inefficiently, producing imperfect or downright perverse responses to individual circumstances. They are also perishable since people learn over time how to avoid them.

Discretion, benevolently and competently exercised, can potentially produce better responses in each case.

Regulatory Luddism is, of course, not optimal either. Waiting until a crisis proves the rules to be ineffective is extremely costly. A policy-making function should be forward-looking and responsive to macro-prudential indicators and information collected by supervisors.

In summary, regulators should rely to a large extent on simple, verifiable rules.

Price and quantity

Pursuing the requisite architectural analogy, let us consider how a structural engineer would decide what architectural structure loads could be. Engineers wish to guard against catastrophic structural failure.

They must balance, at the margin, the cost of failure with the cost of safety measures. These calculations are usually prescribed by law, perhaps because engineers do not necessarily bear all the social costs if their building fails (although they can be sued for damages).

In summary: regulators should use hard limits and stress tests.

Home and host

The Basel 2 framework relies on assumptions that are likely to fail. Developing countries are vulnerable to external shocks: shocks to external bank lending flows may be exacerbated by Basel 2, and there is no true international lender of last resort. Developing countries should therefore need to consider designing their regime.

In summary: to increase the effectiveness of their prudential regimes, regulators should consider requiring foreign branches to incorporate locally.

Some for one and one for some

I suggested earlier that the content of the new proposals was inappropriate for developing countries because the process was flawed.

The principles outlined above-suggested changes to the content; here, I consider whether developing countries could change the process, that is, the international structure of rulemaking.

In summary: developing country regulators should act collectively to change the rules of the game.

Conclusion

Given its objectives and strong analytical foundations, the New Basel Accord opens the door to many research questions.

The impact of the proposal on the global banking system through possible changes in bank behavior; a set of issues around risk analytics such as model validation, correlations, portfolio aggregation, operational risk metrics, and relevant summary statistics of a bank’s risk profile; issues brought about by Pillar 2 (supervisory review) and Pillar 3 (public disclosure).

The output of the risk calculations under the New Basel Accord may also change bank behavior as some internal risk metrics are disclosed to the public.

With this in mind, our view for a future research agenda focuses less on regulatory design.

Instead, the agenda might be better oriented towards understanding the Accord’s likely impact on the banking system, possible changes in bank behavior through different uses of the risk measurement framework, and important analytical issues around model development and validation in both credit and operational risk narrowly and the development of relevant risk summary statistics more broadly.

Undoubtedly, given its scope and complexity, the Accord provides many opportunities for researchers to contribute to the policy debate and implement these proposals.