Investment and loans are the two strategies for the utilization of bank funds. Although the main purpose of these two strategies is to earn a profit, they have many dissimilarities. Let’s understand how bank investment works.

Meaning and Definition of Bank Investment

Investment is using money to make more money to gain income, increase capital, or both. The term investment includes public and private funds for a relatively long period to earn income.

So, by bank investment, we mean that part of a bank’s loanable funds is employed in the money market or capital market by purchasing securities to earn profit.

11 Characteristics of Bank Investment

Bank investments have different aspects in comparison to loans. Let us discuss some important features of the bank investment:

Nature of Fund

Banks invest with the residual fund after meeting the reserve and loan requirements. Banks have instances of utilizing funds only for loan purposes without making any investment.

But there are no instances of using the excess funds to make only investments and giving no loans. So. bank investment means utilizing residual funds profitably after meeting loan requirements.

Third Line of Defense

Based on liquidity, primary and secondary reserve act as the first and second lines of defense. A bank loan is called an illiquid asset.

A bank loan is a such asset of a bank that cannot be used in a time of liquidity crisis. A bank’s investment in securities can be used as the third line of defense in that situation.

Creditor status of Bank

In the case of a loan or investment, the bank takes the creditor position. In the case of a loan, the bank is one of the few big Creditors of the borrower. But in the case of investment, the bank is one of many creditors to the issuer/seller of the instrument.

Initiative of Transactions

In the case of Ioan, the initiative of the transaction comes from the borrower. But in the case of investment, the transaction initiative comes from the bank’s part.

The volume of Investment Relative to the size of the Bank

Banks provide loans to creditworthy borrowers and make a profit. On the other hand, relatively small banks make investments of different maturities through the financial market to meet liquidity and profitability.

From the analysis of the usage of bank funds, it is found that small banks make investments by one-third of the funds available for making a profit. But large-sized banks invest not more than 20% of their funds.

Personal Vs. Impersonal Transaction

In the banks’ loan activities, there is a personal transaction between the bankers and the borrowers. But in the case of investment, there is no direct transaction between the main issuers of securities and the banks.

Secondary Reserve Assets vs. Investment Assets

Short-term securities are used as secondary reserve assets and investment assets. But in the case of investment, medium and long-term financial instruments should be used.

Fluctuations of Market Price

Financial instruments are affected by the fluctuation of the market price. But the loan amount is accumulated and increased by non-payment of loan installments.

Negotiation

Borrowers can bargain with the bank about loan amount installment security and interest, i.e., the borrower and the bank can enter into the discussion. But there is no such provision for debenture purchasing banks as conditions are pre-fixed.

Knowledge of Use of Fund by the provider of Funds

Banks know what the borrower will do with the loaned amount. That is, in the case of loans, banks know the purpose.

But when banks invest funds, they do not know what the issuer of financial security will do with that fund. As the provider of funds, banks don’t have any knowledge regarding the purpose of the loan.

Termination

In the case of a loan, successful termination depends on the willingness and the ability of the borrowers rather than the bank. But the holders of debt instruments may terminate the same at their will.

5 Objectives of Bank Investment

Loan activities are the traditional technique of profit earning of banks. Some purposes recently gained popularity for non-loan bank investment.

Maximization of the wealth of Shareholder

The main purpose of each bank activity is to maximize the shareholders’ wealth by earning appropriate profits. Credit risks are the barriers to maximizing shareholders’ wealth.

So, banks invest part of their loanable funds to earn profit and maximize shareholders’ wealth with minimal risk.

Diversification of Risk

Banks should not use the fund to provide the loan only. Banks also invest in the debt instruments issued by well-known companies to reduce the risk of the use of funds.

Supporting income

Interest receipts, commissions, charges, and fees are the main sources of bank income.

On the other hand, dividend/income from purchasing securities, bonus shares, and capital appreciation are considered supporting income received from an investment, which, along with conventional incomes, contributes a lot to strengthening a bank’s financial position.

Source of supplementary liquidity

Primary reserve and secondary reserve are the conventional sources of banks’ liquidity. But if the primary and secondary reserves are not enough to meet the liquidity requirement, a liquidity crisis may occur.

In this case, as the third source of liquidity, investments by banks can be used as supplementary assets.

Reducing tax liability

Earnings from loans are always taxable. The rate of tax varies with varying levels of income. In this situation, banks can invest in different types of shares, bonds, and debentures that are tax-free or tax exempted, thereby enjoying reduced tax amounts.

11 Functions of Bank Investments

The invested assets of banks positively contribute to the bank’s success as an institution. The main functions of bank investments are:

- Maintaining a trend of stable income

- Meeting the liquidity gap

- Diversifying the risk of bank funds

- Avoiding centralization of the use of bank funds

- Enhancing income through capital appreciation

- Reducing tax liability

- Arranging protection against interest rate fluctuation

- Ensuring flexibility of asset mix

- Discharging social responsibility to raise goodwill and the reputation of the bank

- Participating in the management of the company by purchasing shares

- Playing an important role in establishing and developing the capital market

Through investment activities, banks can keep the flow of income stable. As a result, it will be easier for banks to face the liquidity crisis by selling the invested securities from time to time.

Risks can also be diversified by investing in the securities of many companies. Besides, a bank’s investment can increase the income generated from capital appreciation.

Tax liability can be reduced if the bank invests in the bonds or shares eligible to enjoy tax benefits according to the government’s tax policy.

The ups and downs in the interest rate level often put the bank at risk. The income generated from capital appreciation plays a vital role in reducing the loss caused by the change in interest rate. Bank cannot increase or decrease illiquid assets whenever required.

But, the investments can easily be liquidated to fulfill the bank’s sudden liquidity requirement. Moreover, banks perform their social responsibilities by investing in the securities of the companies engaged in social welfare, approved by the government.

Bank investment preserves the interest of both the bank owners and the general people of the country, directly or indirectly. In underdeveloped countries, banks contribute a lot to developing the capital market by actively participating in the transaction.

4 Rationale for Using Bank Funds in Non-Loan Investment

That investment could be an earning source was almost unknown before the Second World War. Now, the question is, what is the rationale for using loanable funds in non-loan investment activities?

There are some logics of utilizing bank funds on non-loan investments. These logics are as follows:

Illiquidity of Loan

Generally, the loan is tough to convert into cash before maturity.

Risk of Loan

There are very few examples of 100% recovery of bank loans. That is, late payment of loans, along with the possibility of bad debt, is a widespread phenomenon.

Adverse local economic condition

Generically, loans can be considered local transactions. Any unexpected adverse event in the locality under the bank’s purview may cause an economic downturn in that particular locality and the banks. Therefore, the loan demand will be reduced, and the risk of non-recovery of loans will be increased.

Taxability of Bank Loan Income

Incomes from loans must be fully taxable, so the amount of tax payable often becomes higher. Investment activity has emerged to eliminate the above-mentioned limitations of loans and earn more profit.

The above four limitations of loans can be avoided by investing in the short term and long-term securities.

That is, debt instruments can be converted into cash with little risk of loss of principal value.

Because, unlike loan defaulters, the issuer of debt instruments is not unable or unwilling to make payments to holders of debt instruments.

On the other hand, it is difficult to sell the instruments in the money and capital markets with little loss of principal value rather than presenting them to the issuer of those instruments.

The risk related to the recovery of invested funds in securities is less than that of a loan. Bank loan activities are affected by unexpected local conditions.

Income from security is tax-free, eligible to get a tax rebate, and in some cases, eligible to enjoy a concessionary tax rate. But investment in securities is less affected by local economic conditions. Rather, it is affected by the impact of the national economic conditions on the money market and capital market.

For these reasons, banks invest in the money market and/or capital market instruments such as shares, bonds, debenture, and other financial instruments of well-known companies to make a profit and ensure the best use of their non-loan investment funds.

Administrative Structure of Investment Activities

Banks have separate departments/sections to perform their investment activities. Legally, the Board of Directors is responsible for managing the Bank’s investment portfolio. Formulating investment policy is the responsibility of the Board of Directors.

In actual practice, the Board usually delegates these responsibilities to a committee known as I/C, i.e., Investment Committee works through a department viz. Investment Department. The Investment Department of a commercial bank normally performs the functions as under:

- To carry out regular studies of trends in security markets.

- Select securities for long-term investment purposes.

- To undertake trade and switching functions.

- To undertake security issues.

- To evaluate securities to determine associated credit and money rate risks.

- To keep in a safety vault all the security instrument

- To maintain proper records of all the securities held by the banks.

The chief of the investment department is known as the chief investment officer. We have already known that the activities of the investment department are monitored and controlled by the board of directors through a permanent investment committee.

The permanent investment committee, including directors, approves investment policies and strategies. Investment policies and strategies, once approved, are translated into reality by the chief investment officer.

The administrative structures of the investment department are as follows:

Bank’s Investment Policy

Before investing, if there is a clear direction and established guidelines for investment, the possibility of error and confusion in the decision will be reduced; bank investment policy may be written or verbal.

But, some bank officers think those written investment policies are not so reliable. Due to changes in economic conditions, the number of investable funds or any other change can make the written investment policy ineffective or useless.

But this opinion is not acceptable because written investment policy must be changed and modified with the changing circumstances. However, there are four principal reasons for having a written bank investment policy:

- Portfolio constraints, goals, and objectives become clear.

- A written policy also provides a continuing understanding of these constraints, goals, and objectives.

- Provides continuity of approach, and

- Provides a definite basis for the evaluation of operational performance.

Even if written, the policy should provide scope to accommodate reasonable flexibility as and when required, especially with the dynamic economic and business conditions.

The factors of effective and useful investment policy are:

The necessary factors in the packet for an effective and appropriate investment policy are mentioned in the list above.

These factors are self-explanatory. However, the number of investable funds should be determined properly. The purpose of investment should also be determined.

The strategies required to be applied in investment activities should also be specified earlier. The investment officers’ responsibility, authority, and scope of activities should be clearly specified in the policy, and every employee should understand these instructions clearly.

A satisfactory liquidity level can be maintained by investing the maximum possible funds if there are clear guidelines for adjusting investment activities and liquidity.

The investment officers can successfully and flawlessly perform their activities if there is a clear and proper direction regarding the risk diversification of the portfolio of investments.

Bank Investment and Expected External Environment

It is obviously difficult to forecast key elements of the external environment, such as the economy’s growth, interest rates, inflation, and unemployment.

Weaknesses in many past forecasts indicate that forecasting is still more an art than a science. Nevertheless, forecasting general trends in key economic indicators is important in managing the security portfolio. Nearly every security decision has an implicit forecast of the external environment.

For example, the decision between buying long-term versus short-term bonds generally contains an implicit forecast for interest rates and the future inflation rate.

However, it is preferable to make security decisions consistent with an explicit forecast rather than make security decisions containing an implicit forecast that may or may not be consistent with what the portfolio manager believes will happen.

Most bank managers have some predictions for the future external environment.

Whether these predictions are correct is not the major concern; the point is that a bank’s security management decisions should be consistent with these predictions.

Furthermore, because of the uncertainty of any economic predictions, decisions should be made with adequate safeguards to protect the bank from incorrect predictions.

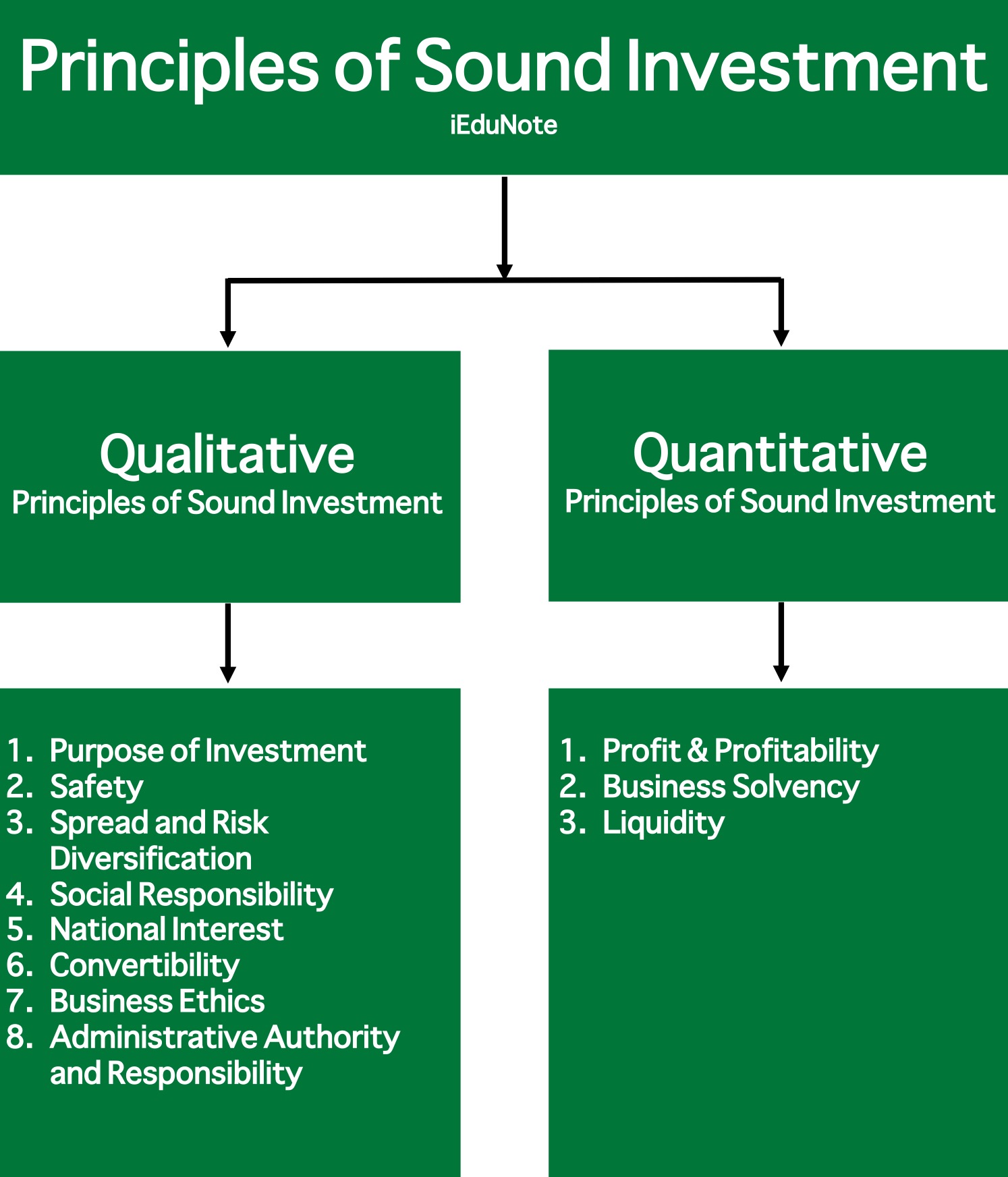

11 Principles of Sound Investment

Investment activities of banks are more recent than loan activities. Banks started to utilize funds by making investments due to diversification of the sources of profit. Depositors’ money is the main source of banks’ funds.

So, if banks fail to repay the money on demand, they will lose public confidence and business. For this reason, the bank should follow sound investment principles before investing the funds.

8 Qualitative Principles of Sound Investment By Bank

Purpose of Investment

Commercial banks applied different strategies to ameliorate their income. Investment is one of them. Investments can be made to adjust liquidity to reduce tax liability or diversify risk.

The investment policy should include the specific steps and types of investments to achieve specific purposes. In this case, the investment officer can avoid the wrong decision and make the right decision at the right time.

Safety

Bank’s investment officer must consider the effect of price fluctuation of financial instruments before investing. If the security price fluctuates, banks have to face a serious problem. So, at the time of investment, the investment officer should focus on credit rating and the company’s past performance.

Spread and Risk Diversification

In the banking business, risks are diversified along with the profitability of the investment. Investment officers must follow the credit rating of the companies and then invest in a diversified portfolio of assets, not in a single asset.

Social Responsibility

The reputation and success of the banking business depend on the banks’ social responsibility. Banks can perform their social responsibility by purchasing securities issued by the government or government-approved companies.

National Interest

Bank’s investment should be made within the preferred scopes/sectors of the government or regulatory authorities, directly or indirectly, based on the annual development planning, five-year planning, inflation, and tax policy. The patronage and participation of banks in national development are highly coveted.

Convertibility

Investment in securities is easily convertible into cash. Bank investment officers must invest in those easily convertible securities into cash with little risk of loss of principal value.

Business Ethics

Investment is one of the ways of earning income. Banks should not invest in businesses with unethical activities.

Administrative Authority and Responsibility

The responsibilities of determining the investable funds, selecting securities with appropriate maturity, and analyzing credit proposals are distributed, and appropriate authority should be delegated precisely. Imprecise and vague responsibilities create the opportunity for negligence.

3 Quantitative Principles of Sound Investment By Bank

Profit & Profitability

Like any other business, the bank aims to maximize the shareholders’ wealth. Banks should invest in relatively high-quality securities after proper and effective analysis.

If investment income is not satisfactory, it will not be possible to make an adequate profit after meeting the cost of the fund.

Business Solvency

As a profitable business organization, a bank has to maintain business solvency. So, banks must maintain such a liquidity position, which will ensure the ability to satisfy the needs of depositors.

Liquidity

Liquidity and profitability are the two important considerations of the bank. Banks should invest by keeping the liquidity at a satisfactory level.

Conclusion

Bank investment policies are influenced by the general economic outlook, particularly the outlook for interest rates. If the outlook is for rising interest rates, banks probably will confine their purchases to short-term maturities.

On the other hand, if the outlook is for declining interest rates, banks may be willing to hold longer-term maturities. Although banks are willing to hold their investments to maturity, they are sensitive to the risk of a fall in the prices of guilt-edged securities.

When such a fall in security prices is feared, they generally refrain from adding to their investments, even though their liquidity position may support an increase.

Portfolio management, in essence, involves a compromise between maximizing return opportunities and minimizing risk exposure.

A logical step in the portfolio planning process is to classify various types of securities according to the objectives they are designed to meet and the risk they assume or protect against.

It is essential to limit portfolio diversification to reasonable proportions.

Otherwise, the burden of appraisal and periodic reviews might become an onerous task. A portfolio should never include more securities that can be diligently reviewed periodically.

To facilitate this, a limit should be placed on the total number of securities included in a portfolio. Once the limit is reached, any new acquisition should be matched with the disposal of an existing holding.

As stated in some earlier sections, investment securities provide an alternative source of income for commercial banks, especially when loan demand is relatively low during slowdowns in economic activity.

Bank policy should maximize the return on the securities portfolio per unit of risk within regulatory and market constraints.

In this regard, bank management needs to consider the tax implications of municipal securities, default risk and call risk of municipal and corporate bond securities, interest rate risk of longer-term securities, and marketability of securities.

The effects of investment policy on the risk and return of the bank’s total assets should also be evaluated in a portfolio context, where diversification benefits may be gained by purchasing securities with return patterns that are not perfectly positively correlated with the return pattern of other bank assets.

Bank portfolio management has recently been confronted with new and greater problems.

Bond prices and interest rates have become much more volatile. Banks have expanded their activities into new areas of operation, and attention has been focused on managing liabilities and assets.

These changes have begun to raise many searching questions about portfolio management in general and various investment techniques and strategies in particular.

We do not claim that the guidelines discussed in the preceding pages will provide all the answers to bank portfolio-related questions.

We neither feel that following these guidelines and principles will guarantee superior investment performance. However, they will provide a solid framework within which a bank can achieve improved investment results more surely and easily.