What is the Expectation Gap in Audit?

Auditing expectation gap or simply expectation gap is the term used to signify the difference in users’ expectations of financial statements and auditor’s expectations concerning audited financial statements.

Although it’s about expectations, its scope and meanings have been defined in several ways.

The difference in expectation can arise in the performance, i.e., the level of performance users expect from the auditor and how the auditor performs.

The expectation gap can also be explained as the difference between the effectiveness of audit engagement, what users believe, and what the auditor believes.

Expectation-gap related to audit can also be explained as the difference between the expectation of the user and the auditor himself on the responsibilities of the auditor; it can also refer to differences in understanding regarding the nature of audit engagement, i.e., what users believe an audit is and what audit is.

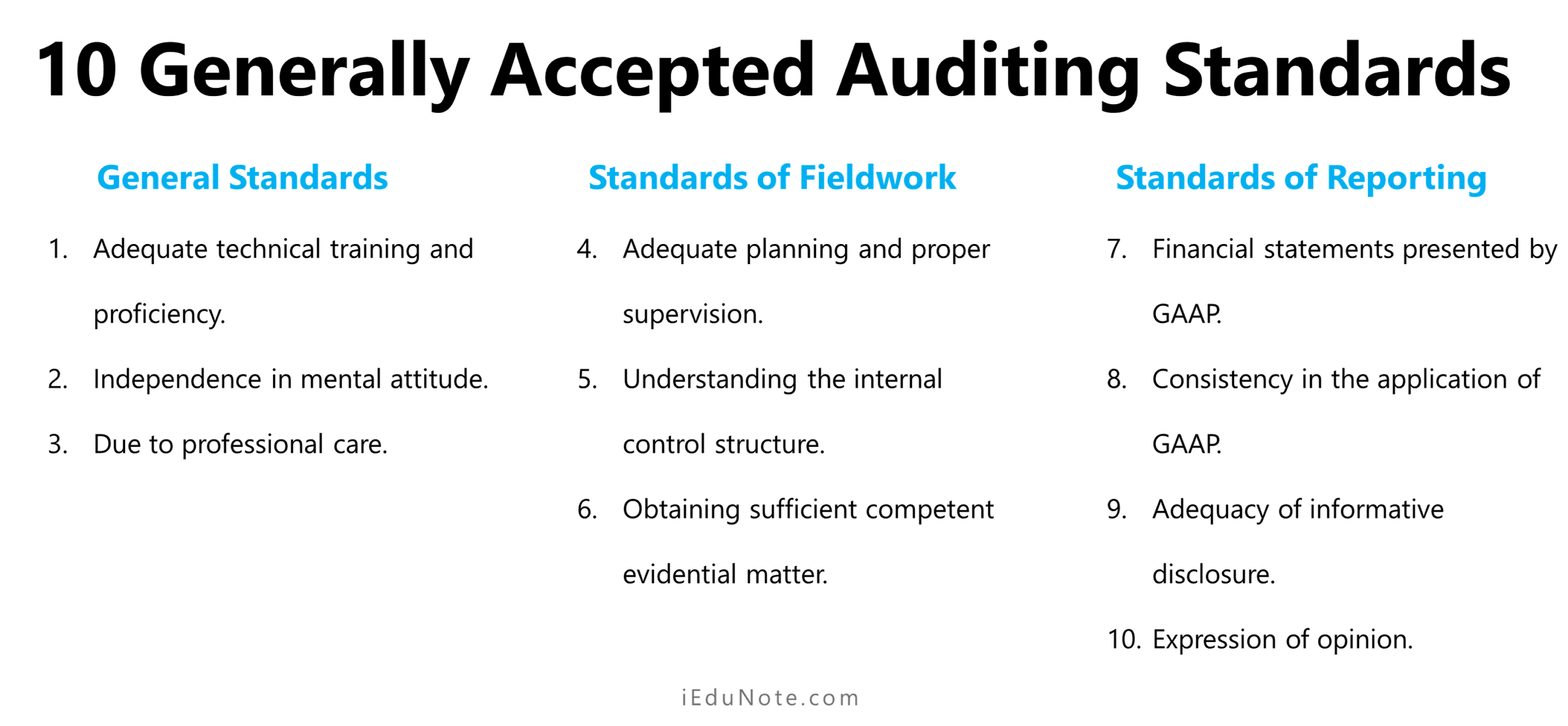

Auditors’ Responsibilities and Expectation Gap

Users of audited financial statements expect to:

- Perform the audit with technical competence, integrity, independence, and objectivity.

- Search for and detect material misstatements, whether intentional or unintentional.

- Prevent the issuance of misleading financial statements.

Some users have concluded that these expectations are not being met, leading to what has become known as the expectation gap. The expectation gap relates mainly to three troublesome areas;

- detecting and reporting on errors and irregularities, especially fraud,

- detecting and reporting on illegal client acts, and

- reporting whether there is uncertainty about the ability of an entity to continue as a going concern.

These are explained below;

Errors and Irregularities

The primary factor distinguishing errors from irregularities is whether the underlying cause of a misstatement is intentional or unintentional.

The term errors refer to unintentional misstatements or omissions in the financial statements, whereas the term irregularities refer to intentional misstatements or omissions in the financial statements.

When the auditor concludes that the financial statements are materially misstated due to an error or irregularity, the financial statements are not prepared in conformity with GAAP.

Accordingly, the auditor should insist that the financial statements be revised by management. When this is done, the auditor should issue a standard auditor’s audit report and express an unqualified opinion.

However, when the financial statements are not revised, the auditor should express a qualified opinion or an adverse one because of the departure from GAAP and disclose the reasons in the audit report.

Illegal Client Acts

Therefore, an auditor must be ethical and professional.

An illegal act involves paying bribes, making illegal political contributions, and violating specific laws and governmental regulations. The effects on the audit report of an illegal act are the same as for irregularities.

When an illegal act having a material effect on the financial statement is not properly accounted for or disclosed, the auditor should express a qualified opinion or an adverse opinion because the financial statements are not prepared in conformity with GAAP.

Suppose the auditor cannot obtain sufficient evidence about an illegal act. In that case, there is a scope limitation, and the auditor should express a qualified opinion or disclaim an opinion on the financial statement.

If the client refuses to accept the auditor’s report, the auditor should withdraw from the engagement and indicate the reasons for the audit committee in writing.

Doubts to Continue as a Going Concern

An auditor is not responsible for predicting future conditions or events.

However, SAS 59 – The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern; provides that the auditor has a responsibility to evaluate whether there is substantial doubt about the entity’s ability to continue as a going concern for a reasonable period.

When the auditor concludes that there is substantial doubt about the entity’s ability to continue as a going concern during this period, the auditor should state this conclusion in the audit report:

- Suppose the management’s disclosures in the financial statements concerning the entity’s ability to continue as a going concern are considered adequate by the auditor. In that case, an unqualified opinion should be expressed, and an explanatory paragraph should be added following the opinion paragraph describing the uncertainty concerning management’s disclosures.

- Suppose the auditor considers the management’s disclosures in the financial statements adequate. In that case, there is a departure from GAAP, and the auditor should express either a qualified opinion or an adverse opinion and explain the reasons in an explanatory paragraph preceding the opinion paragraph.

Narrowing The Expectations Gap

An auditor must reduce audit risk to an acceptably low level to attain reasonable assurance.

But what is reasonable?

On careful analysis of this gap, one of the critical reasons for widening the gap is a lack of understanding of different connected factors. And this is not only a lacking on the part of users of financial statements but also the auditor sometimes.

If the following efforts are invested in these areas, then expectations can be bridged to a great extent:

- Users must understand why auditors can only provide reasonable assurance and not absolute assurance and what are the inherent limitations of the audit.

- Users must understand that general-purpose financial statements are meant for the general needs of users, even if they have been audited in the best way possible. Still, it does not mean audited financial statements can help in any decision-making situation.

- Users must realize that auditor’s work is relative to circumstances that require the use of judgment, which may be wrong. Although the auditor works diligently, it does not always mean if a judgment is wrong, then the auditor is guilty of ignorance; rather, it will be assessed based on what the auditor could do and what he did.

- Although auditors and management are required to produce financial statements that are easy to understand, users are also expected to have a certain degree of relevant knowledge on how to use and interpret financial statements. Financial statements are not for everyone to read and act upon.

- For auditors to understand users’ expectations, they must arrange workshops or seminars so that users at least feel that they have been auditors and must not rule out everything based on a lack of knowledge on the part of users.

- An auditor must make audit reports easy to understand for the masses and avoid a great extent of any technical jargon that can impair an ordinary person’s understanding who lacks skillful insight into financial statements.

- An auditor already provides less than absolute assurance, so he must not leave any effort undone to maintain a reasonable level of assurance by complying with the requirements of relevant auditing standards. For example, proper planning, an appropriate understanding of the entity to design further audit procedures, maintaining a skeptical attitude, reducing sampling risk to an appropriate level, etc.

One of the biggest reasons for this gap is the auditor’s responsibility to detect fraud.

When it comes to fraud, users require an auditor to act as an investigator, and the auditor is expected to unearth even the most sophisticated fraud events.

However, users do not agree with the explanation that the auditor is not responsible for detecting fraud; it is managed as they feel the auditor’s role is much more than just a confirmation of management’s assertions.

This area is still developing, and audits as a profession are facing great challenges in this regard.

Source

Provided by iedunote: https://www.iedunote.com/