Auditing standards require that the auditor and the client agree on the engagement’s terms. The agreed terms must be in writing, and the usual form would be a letter of engagement.

Any other form of appropriate contract, however, may be used. It is a written contract between the auditor and the client, stating both parties’ understanding of the professional relationship.

In the interest of both the client and auditor, the auditor sends an engagement letter, preferably before the commencement of the engagement, to help avoid misunderstandings concerning the engagement.

So what is an audit engagement letter, how does it work, what are its contents, and how to format it? Let’s learn.

What is an Audit Engagement Letter?

The audit engagement letter confirms the auditor’s acceptance of the audit and includes the responsibilities’ objective, scope, and extent of the audit.

The audit engagement letter documents and confirms the auditor’s acceptance of the appointment, the objective and scope of the audit, the extent of the auditor’s responsibilities to the client, and the form of any reports.

Issuance of the engagement letter is one of the procedures to be followed before the commencement of an audit and is in response to the appointment for a new audit assignment.

An engagement letter is sent by an auditor to his client after the receipt of the communication regarding his appointment, but preferably before the commencement of the engagement, spewing out the extent of his responsibilities to avoid any misunderstanding concerning his engagement and documents and confirming the acceptance of appointment, the objectives, and scope of the audit, the extent of responsibilities and the form of reports to be made to the client.

Objectives of Engagement Letter

The main objectives of an engagement letter are as follows:

- It clearly defines the extent of the auditor’s responsibilities and minimizes the possibility of any misunderstanding between the client and the auditor.

- It provides written confirmation of the auditor’s acceptance of his appointment, the scope of an audit, and the form of his report.

- The client becomes aware of the directors’ statutory responsibilities, which in no way are diminished by the appointment of an auditor.

- Management is informed that the audit tests would be based upon the results of an evaluation of internal control.

- The client has explained the statutory requirements of the company’s ordinance, and through the matters to be reported are satisfied by law, the auditor would be free to report on the matter in respect of which he is not satisfied.

- The client becomes informed about the other professional services that the auditor can provide.

- The client is briefed that the discovery of fraud is not the main aim of the audit.

- The scope of special or additional work is also determined.

- The basis of the computation of frees is brought to the client’s knowledge.

Engagement Letter to Whom Sent

It should be sent to the following:

- The engagement letter should be sent to all new clients soon after the appointment as an auditor and, in any event, before the commencement of the first audit engagement.

- As soon as a suitable opportunity occurs, an engagement letter may also be sent to existing clients to whom no such letter has previously been sent.

- When there is a change in the nature and scope of assignment or a change in the job specification, management, size and line of business, and data processing method, the communication of such a letter assumes greater importance.

- When an auditor of a parent company is also the auditor of its subsidiaries, a separate engagement letter should be sent to each company audited by him.

- When there are joint auditors, an engagement letter in similar terms is sent by each auditor when no joint letter is sent.

Contents of Engagement Letter

1. Auditor’s Responsibilities

The engagement letter should explain the statutory and professional duties and reporting responsibilities.

2. Management’s Responsibilities

The engagement letter should point out the management’s statutory responsibilities for maintaining proper accounting preparation of financial statements, an institution of internal control, selection and application of accounting policies, and safeguard of assets.

3. Scope of Audit

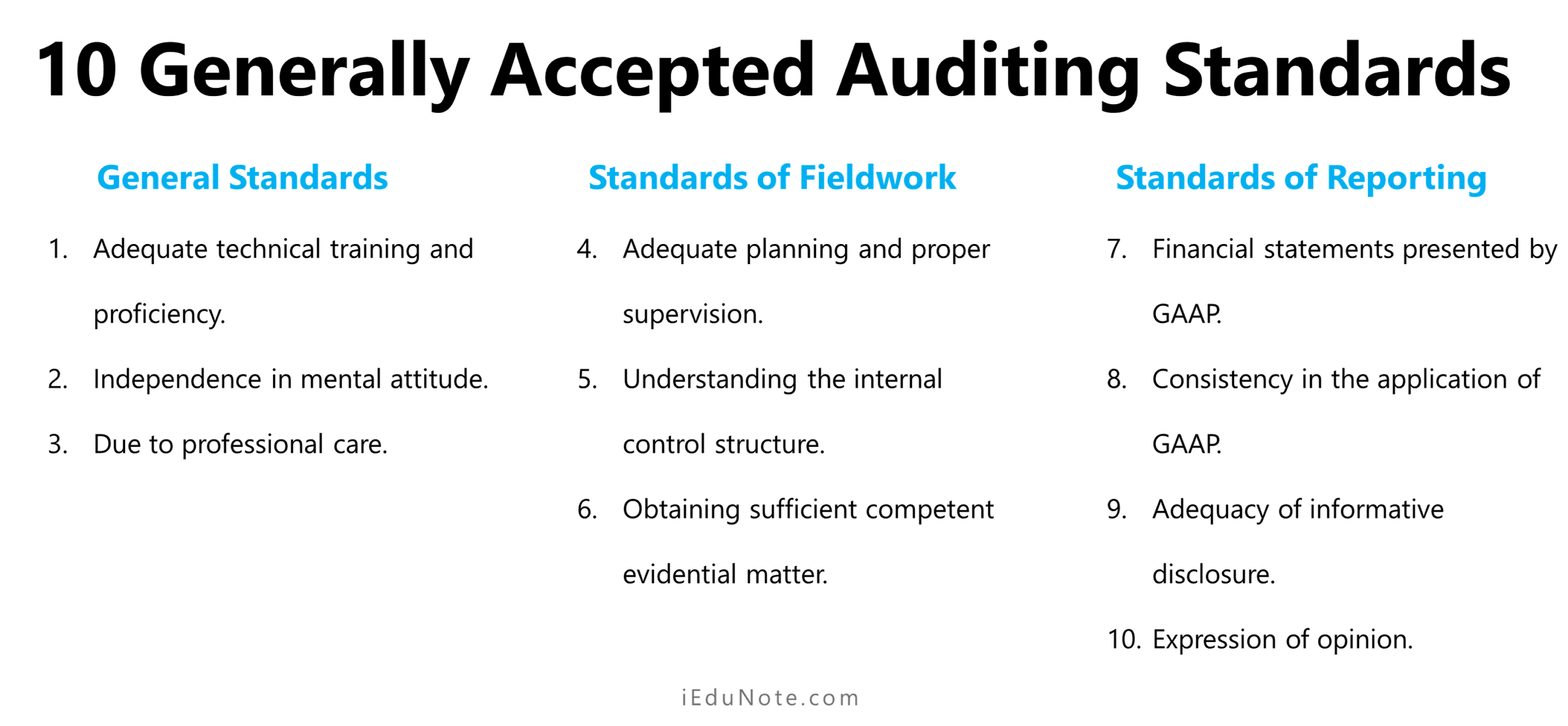

It should be indicated that the audit will be conducted following the international auditing standards and regarding relevant international statements on auditing. It should be pointed out that the auditor would satisfy himself:

- by conducting adequately necessary tests and procedures;

- the extent of substantive tests will depend upon an assessment of the accounting system and proper evaluation of internal control;

- he will expect relevant and reliable evidence from the management in matters where independent audit evidence is unavailable.

Check our article on the scope of the audit.

4. Management’s Representations

It should indicate that the auditor, before finalization of the audit, -may seek written representation from the management in respect of matters having a material effect on financial statements.

5. Irregularities and Fraud

The engagement letter should clarify that management is responsible for preventing and detecting irregularities and fraud. It should be made clear that an audit’s main purpose is not to discover fraud and defalcations.

6. Other services

The engagement letter should adequately describe the nature and scope of services that an auditor may carry out in addition to his responsibilities as an auditor.

7. Fees

The fees and the basis on which the same is computed.

8. Client’s Confirmation

The engagement letter should include a request to management that they confirm in writing an agreement to the terms of an engagement letter.

Acceptance of a Change in Engagement

Before completing the engagement, an auditor who is required to change the engagement to one which provides a lower level of assurance should consider the appropriateness of doing so.

A request from the client for the auditor to change the engagement may result from a change in circumstances affecting the need for the service, a misunderstanding as to the nature of an audit or related service originally requested, or a restriction on the scope of the engagement, whether imposed by management or caused by circumstances.

A change in circumstances that affects the entity’s requirements or a misunderstanding concerning the nature of service originally requested would ordinarily be considered on a reasonable basis for requesting a change in the engagement.

Before agreeing to change an audit engagement to a related service, an auditor who was engaged to perform an audit following International Standards on Auditing (ISAs) would consider any legal or contractual implications of the change in addition to the above matters.

Where the terms of the engagement are changed, the auditor and the client should agree on the new terms.

Obtaining the Audit Engagement

Professional standards require that audit firms establish policies and procedures to decide whether to accept new clients and retain current clients.

The purpose of such policies is to minimize the likelihood that an auditor will be associated with clients of which the auditor is not independent, lacks integrity, or accepts an engagement they do not have the skill or competence to perform.

If an auditor is not independent of a client, it can lead to non-compliance with ethical requirements and bad publicity.

If an auditor is associated with a client who lacks integrity or the auditor does not have the skill and competence to perform the audit, the risk increases that material misstatements may exist and not be detected by the auditor.

Steps in Accepting an Audit Engagement

Sample of Audit Engagement Letter

The following letter is for use as a guide in conjunction with the considerations outlined in this ISA and will need to be varied according to individual requirements and circumstances.

| To the Board of Directors or the appropriate representative of senior management: You have requested that we audit the balance sheet of …………………………………………. as of ………………………………………….. and the related statements of income and cash flows for the year then-ending. We are pleased to confirm our acceptance and our understanding of this engagement using this letter. Our audit will be made with the objective of our expressing an opinion on the financial statements. We will conduct our audit following International Standards on Auditing (or refer to relevant national standards or practices). Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatements. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management and evaluating the overall financial statement presentation. Because of the test nature and other inherent limitations of an audit, together with the inherent limitations of any accounting and internal control system, there is an unavoidable risk that even some material misstatements may remain undiscovered. In addition to our report on the financial statements, we expect to provide you with a separate letter concerning any material weaknesses in accounting and internal control systems which come to our notice. We remind you that the responsibility for the preparation of financial statements including adequate disclosure is that of the management of the company. This includes the maintenance of adequate accounting records and internal controls, the selection and application of accounting policies, and the safeguarding of the assets Of the company. As part of our audit process, we will request from management written confirmation concerning representations made to us in connection with the audWe look forward to full cooperation with your staff, and we trust that they will make available to us whatever records, documentation, and other information are requested in connection with our audit. Our fees, which will be billed as work progresses, are based on the time required by the individuals assigned to the engagement plus out-of-pocket expenses. Individual hourly rates vary according to the degree of responsibility involved and the experience and skill required. This letter will be effective for future years unless it is terminated, amended, or superseded. Please sign and return the attached copy of this letter to indicate that it is in accordance with your understanding of the arrangements for our audit of the financial statements. XYZ & Co. Acknowledged on behalf of ABC Company by (signed) Name and Title Date:…………… |

Engagement Letter in Case of Audits of Components

When the auditor of a parent entity is also the auditor of its subsidiary, branch, or division (component), the factors that influence the decision whether to send a separate engagement letter to the component include the following:

- Who appoints the auditor of the component?

- Whether a separate auditor’s report is to be issued on the component.

- Legal requirements.

- The extent of any work performed by other auditors.

- Degree of ownership by a parent.

- Degree of independence of the component’s management.

Engagement Letter in Case of Recurring Audits

On recurring audits, the auditor should consider whether circumstances require the terms of the engagement to be revised and whether there is a need to remind the client of the existing terms of the engagement.

The auditor may decide not to send a new engagement letter each period.

However, the following factors may make it appropriate to send a new letter:

- Any indication that the client misunderstands the objective and scope of the audit.

- Any revised or special terms of the engagement.

- A recent change of senior management or those charged with governance.

- A significant change in ownership.

- A significant change in the nature or size of the client’s business.

- Legal or regulatory requirements.

Acceptance of a Change in Engagement

If the auditor is asked to change the engagement to one that provides a lower level of assurance, he should consider the appropriateness.

Suppose the audit is a statutory audit (also known as a financial audit). In that case, the auditor must provide an appropriate audit as required by law, giving reasonable assurance of the truth and fairness of the engagement.

If the terms are changed, the auditor and the client must agree. If the auditor and the client cannot agree, the auditor should withdraw from the existing arrangement.

In the case of accepting the change in an engagement letter, the following actions could be taken:

- Before completing the engagement, an auditor who is requested to change the engagement to one which provides a lower level of assurance should consider the appropriateness of doing so.

- Where the terms of the engagement are changed, the auditor and the client should agree on the new terms.

- The auditor should not agree to a change of engagement without reasonable justification.

- Suppose the auditor cannot agree to a change of the engagement and is not permitted to continue the original engagement. In that case, the auditor should withdraw and consider whether there is an obligation, contractual or otherwise, to report to other parties, such as those charged with governance or shareholders, the circumstances necessitating the withdrawal.