What is Marketing Control?

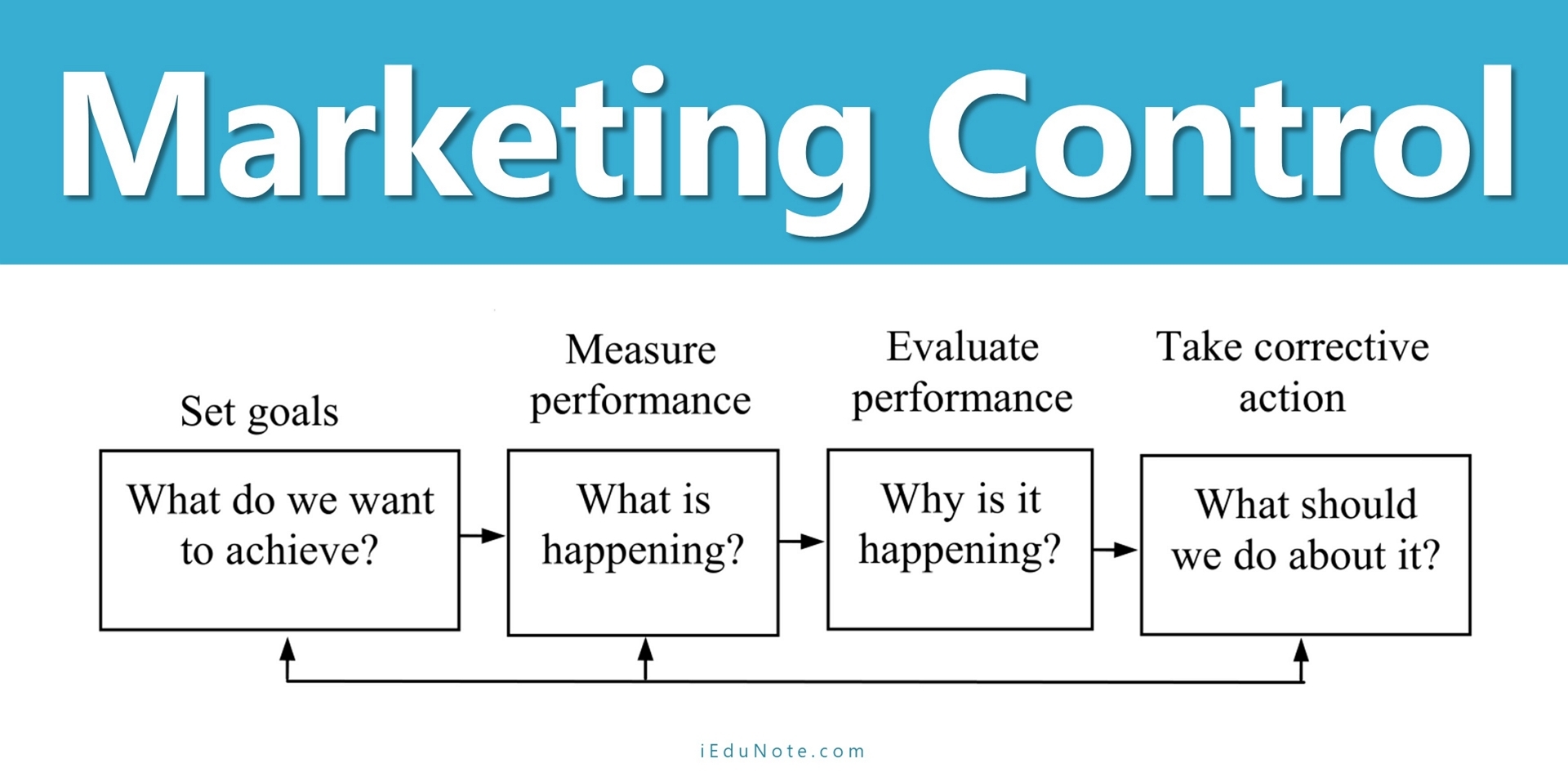

Marketing control is the process of measuring and evaluating the results of marketing strategies and plans and taking corrective action to ensure that marketing objectives are accomplished.

It consists of four steps, shown in the following figure:

Management first sets specific marketing goals and then measures its performance in the marketplace and evaluates the causes of any gap between expected and actual performance.

At length, management takes corrective action to close the gaps between its goals and actual performance. This may warrant changes in the action programs or even changes in the plans.

Operating control involves checking ongoing performance against the annual plan and taking corrective action if necessary.

Its purpose is to ensure that the company achieves the sales, profits, and other goals set out in its annual plan. It also involves determining the profitability of different products, territories, markets, and channels.

Strategic control involves looking at whether the company’s basic strategies are well-matched to its opportunities.

Marketing strategies and programs can quickly become outdated, and each company should periodically reassess its overall approach to the marketplace. An important tool for such strategic control is a marketing audit.

The marketing audit is a comprehensive, systematic, independent, and periodic examination of a company’s environment, objectives, strategies, and activities to determine problem areas and opportunities. The audit provides—useful input for a plan of action to improve the company’s marketing performance.

Types of Marketing Control

Two major types of marketing control are common. The first is the control of day-to-day operations; thus, implementation control involves ongoing activities and uses the organization’s regular accounting and reporting procedures to analyze marketing plans and actions.

Primarily, implementation control seeks to answer the question, ‘Are we doing things right?’ Strategic control involves major strategic directions. This process seeks to answer the question, ‘Are we doing the right things?’ Rather than relying on regular ongoing reports, in general, strategic control involves special studies and procedures.

Implementation Control

Implementation control is the responsibility of functional level managers within a marketing organization. A product manager may be responsible for a sales promotion campaign of toilet soap; an advertising manager will monitor the execution of programs created by an advertising agency.

If one objective is to increase the number of sales calls by 10 percent, the sales manager is accountable for ensuring that sales representatives actually make those additional calls. Each marketing manager is assisted by the work of accountants in their organization.

Major Methods of Implementation Control: The following sections investigate three major methods of controlling marketing activities: sales analysis, cost analysis, and profitability analysis.

Each type of analysis has its own goals up to a point, yet the three methods are cumulative. Since sales minus cost equal profits, these factors clearly interrelate. As we discuss each method, their cumulative nature should become clear.

1. Sales Analysis

Sales analysis compares actual with estimated sales. Sales are analyzed weekly (weekly, monthly, quarterly) and cumulative (year-end). Overall corporate or business unit sales are evaluated at strategic levels.

By contrast, operational and functional managers analyze sales at a micro-level of component factors, such as product, region, or sales territory.

Sales analysis gives experienced managers much more than simple measurement. If sales of one product are up by 25 percent while another product’s performance is 10 percent behind the goals, the manager will study the reasons for the first product’s success and the second product’s less than desirable performance.

If sales of the latter product in the Chittagong division, for example, are found to be 15 percent behind target where other regions are within goals, corrective action will be indicated in the Chittagong region.

Market share analysis is an evaluation of the firm’s performance in comparison to that of its competitors. Such analysis gives executives a broad view of the company’s performance.

For example, suppose that sales are exactly as forecasts: up by 5 percent over the previous year.

However, if industry sales are up 10 percent, the organization is losing market share and is falling behind its competitors. This comparative picture will serve as another indicator of the need for corrective action.

Marketers compile information for sales analysis from their internal records; it flows automatically from the Marketing Information System (MKIS).

However, market share figures are more difficult to obtain since they are based on sales outside the organization. Overall market share may be calculated with relative ease if a trade association reports industry totals.

Sales Component Analysis

Overall, company sales can give only a general idea of marketplace performance, trends, and market share. Both sales analysis and market share analysis are more valuable when data can be broken down into various sales components.

Managers can better plan and take corrective action if they can analyze sales by components such as product line, products, region, district, sales territory, and customer type or size.

The sales invoice is a basic source of information. Computer programs easily summarize sales of any component or combination of components that managers think will be important in marketing control.

Again, we must emphasize the role of the MKIS in providing disaggregated sales information. Managers with access to the MKIS can get regular reports for the time period considered useful.

2. Cost Analysis

Just as sales analysis deals with revenues, cost analysis deals with expenses. With marketing cost analysis, various costs are broken down and classified to determine which costs are associated with specific marketing activities.

Cost analysis involves the reallocation of the natural accounts of financial accounting to the functional accounts of managerial accounting to control marketing costs.

This process involves breaking down marketing costs and assigning them to specific marketing activities or units, such as products, geographic units, channels of distribution, or market segments.

Natural accounts and functional accounts

Natural accounts are the usual financial accounting units found on the official statements of an organization. Our interest here is in the expense accounts, such as rent, salaries, advertising, marketing research, and supplies. Most of these accounts do not show what purpose – for what product – these expenses were incurred.

The first step in cost analysis typically requires that some of the natural accounts’ costs be reclassified into functional accounts, which divides expenditures for their purposes.

A certain portion of the rent, for example, would be assigned to marketing research. Some costs, such as supplies, must be reclassified among various functions; supplies are obviously needed by advertising, the sales force, and marketing research.

Allocating costs

Typically, functional costs are allocated to products, geographic areas, market segments, and even specific customers. Allocation of marketing costs usually requires the advice and counsel of the organization’s accounting department.

Accountants have the specialized training necessary to decide the fairest and most useful method of allocating functional costs.

Cost Analysis by Product, Geographic Area, or Customer

Although marketers ordinarily get a more detailed picture of marketing costs by analyzing functional accounts than by analyzing natural accounts, some firms need an even more precise cost analysis – especially if they sell several types of products, sell in multiple geographic areas, or sell to a wide variety of customers.

Activities vary in marketing different products in specific geographic locations to certain customer groups. Therefore, the costs of these activities also vary.

By allocating the functional costs to specific product groups, geographic areas, or customer groups, a marketer can determine which of these marketing entities are the most cost-effective to serve.

By comparing the costs of previous marketing activities with results generated, a marketer can allocate its marketing resources more effectively in the future.

Marketing cost analysis allows a firm to evaluate the effectiveness of an ongoing or recent marketing strategy by comparing sales achieved and costs incurred. By pinpointing exactly where a firm is experiencing high costs, a marketing cost analysis can help isolate profitable or unprofitable customer segments, products, or geographic areas.

In some organizations, personnel in other functional areas – such as production or accounting – think that marketers are primarily concerned with generating sales regardless of the costs incurred.

By conducting cost analyses, marketers can undercut this criticism and put themselves in a better position to demonstrate how marketing activities contribute to generating profits.

3. Profitability Analysis

Sales analysis and cost analysis are instrumental in diagnosing how well a company’s marketing plan is being implemented. The third type of analysis used for implementation control uses sales and costs to determine profits.

- Profitability analysis provides information on individual units’ profit performance within an organization to determine appropriate corrective action.

- Profitability analysis also provides vital information that allows marketing managers to control the future of their marketing units more effectively.

- Profitability analysis starts with identifying the functional expenses, assigning the functional expenses to marketing entities, and preparing a profit and loss statement for each marketing entity.

This form of implementation control goes beyond sales analysis and beyond cost analysis. It reaches all the way to the ultimate questions, taken together:

Did the margins and profits during the specified period show the healthy base of profits to which we have become accustomed?

Strategic Control

The control of marketing implementation is an ongoing process designed to keep the organization on course. While it is obviously essential to ask if we are doing things right regularly, it is important to ask if we are doing the right things on occasion.

This requires a broad overview of the entire marketing organization. Hard questions must be asked about the strategy being followed; the organization’s fundamental assumptions must be reevaluated.

One key problem in trying to control an organization’s strategy is that its management team is so involved in setting that strategy to find it difficult to call the strategy into question. A formal set of procedures is needed to ensure that managers will carry out a genuine marketing strategy control.

This set of procedures is known as the “marketing audit.” We have discussed this aspect in the evaluation of marketing activities section.

Once the audit process is complete, the marketing executive can make necessary changes in the existing program or modify plans.

When an audit was designed to control a presently running program, the marketing executive can decide if any strategy changes are needed and plan accordingly.

When the audit was for performance review, the executive will apply lessons learned to new programs and determine the competitive position of the product.

A marketer should keep in mind that a marketing audit can only identify strengths and weaknesses in a marketing program, but it cannot solve any existing problems.

Solving the problem is the marketing executive’s job, and it is not always easy to make adjustments in existing programs.

Different parties relating to the company have already formed images and expectations about the product and the channel, promotion, and price strategies. When rapid and radical shifts in the marketing program occur, a marketer risks alienating a sizable portion of the core market.

However, if adjustments are not made, the company’s profitability will suffer. Thus, the marketing executive must be cautious in fully analyzing and planning all possible program changes before taking action.

Without a few exceptions, a marketer brings changes in his programs step by step, not making changes everywhere at a time. He also notifies his middlemen, suppliers, and customers of the changes he is about to bring in programs.

To make consumers aware of the company’s program, he develops a well-thought promotional program. Thus, a marketer brings changes in his marketing program once all related plans are set.