All profit organizations and many non-profit organizations must set prices on their products or services. Although the role of nonprice factors in the modern marketing process is increasing, the price remains an important element in the marketing mix.

In a popular sense, price is the amount of money charged for a product or service. Price is the sum of all the values expressed in monetary terms that consumers part with for the benefits of having or using the product or service. The price goes by many names; rent for houses, the fee to a physician, airfare, interest charged by banks, and so on.

All profit organizations and many non profit organizations must set prices on their products or services. Price is the only element in the marketing mix that fetches revenue; all other elements represent costs.

What are the Factors Affecting Price Decisions in Marketing?

A company’s pricing decisions are influenced both by internal company factors and external environmental factors.

- Internal Factors Affecting Pricing Decisions

- Company’s Marketing Objectives.

- Marketing Mix Strategy.

- Costs.

- Organizational Considerations.

- External Factors Affecting Pricing Decisions

- Market and Demand.

- Competition.

- Other Environmental Elements.

Let’s try to understand them one by one.

Internal Factors Affecting Pricing Decisions

four internal factors that affect the company’s pricing are;

- Company’s Marketing Objectives.

- Marketing Mix Strategy.

- Costs.

- Organizational Considerations.

1) Marketing Objectives

The company must decide on its strategy for the product before setting the price. The task of pricing becomes fairly direct if the company has selected its target market and positioning carefully.

For example, if Toyota decides to produce a new sports car to compete with European sports cars in the high-income segment, it will have to charge a high price. Thus, the pricing strategy is significantly influenced by decisions on market targeting and positioning.

The company might have other objectives. The clarity of the objective makes it easy to set the price. Common objectives sought by marketers are survival, current profit maximization, market-share leadership, and product-quality leadership.

These objectives can be stated as under:

- Survival

- Current Profit Maximization

- Market Share Leadership

- Product-Quality Leadership

Survival

Companies set survival as their prime objective if they are troubled too much capacity, intense competition, or changing consumer wants.

To keep the production running, a company may set a low price, expecting to increase demand. Here, survival gets priority over profits. As long as a company’s prices cover variable costs and some fixed costs, it can carry on business.

However, survival as an objective can be adopted only in the short-term. In the long-run, the company must find out the ways for adding value. Otherwise, it might have to quit its business.

Current Profit Maximization

Many companies accept current profit maximization as their pricing goal. They anticipate what demand and costs will be at different prices and choose the price to produce the maximum current profit, cash flow, or return on investment.

In all cases, a company is interested in current financial results rather than long-run performance.

Market Share Leadership

Some companies intend to achieve market-share leadership. They feel that the company with the largest market share will enjoy the lowest and highest long-run profit.

To emerge as the market share leader, these companies set prices as low as possible. In this regard, a company can pursue a specific market-share gain.

For example, the company wants to increase its market share from 20 percent to 25 percent in one year. It will look for the price and marketing program that will achieve this goal.

Product-Quality Leadership

A company might be interested in achieving product-quality leadership.

This generally warrants charging high prices to cover such quality and the high cost of R&D. For example, Sub-Zero makes the Rolls-Royce of refrigerators – custom-made, built-in units that look more like hardwood cabinets or pieces of furniture than refrigerators.

By offering the highest quality, Sub-Zero sells more than $50 million worth of fancy refrigerators a year, priced at up to $3,000 each.

A company might also use price to accomplish other more specific objectives.

It can set prices to prevent competitors from entering the market. It can even set prices at competitors’ levels to stabilize the market. Prices can be set for ensuring loyalty and support of intermediaries or to avoid government intervention.

Prices can be reduced for the time being to create interest for a product or pull more customers into a retail store. One product may be priced to help the sales of other products of the company.

Thus, the role of pricing is important in accomplishing the company’s objectives at various levels.

Non-profit and public organizations may seek several other pricing objectives. A college aims for partial cost recovery, knowing that it must rely on private donations and public grants to cover the remaining costs.

A non-profit clinic may adopt a policy of full cost recovery in its pricing. A social service organization may set a social price geared to varying income levels of different clients.

2) Marketing Mix Strategy

Price is one of the four marketing mix tools that a company uses to accomplish its marketing objectives. Price decisions must be synchronized and coordinated with product design, distribution, and promotion decisions to constitute a uniform and effective marketing program.

Decisions made for other marketing-mix variables usually affect pricing decisions.

For example, producers using many intermediaries who are supposed to support and promote their products may have to provide larger middlemen margins into their prices.

Companies often make their pricing decisions first. Then other marketing-mix decisions are made based on the price they set. Here, price is a key product positioning factor determining the product’s market, competition, and design. The desired price determines what features the product will possess and what production costs it can afford.

Many companies follow such price-positioning strategies with a technique called target costing.

Contrary to the usual practice, target costing starts with a target cost followed by designing a new product, determining its cost, and then judging the suitability of its price.

HP(Hewlett-Packard) calls this process “design to price.” After being battered for years by lower-priced rivals, HP(Hewlett-Packard) used this approach to create its highly successful, lower-price personal computer line.

Starting with a price target set by marketing, and with profit-margin goals from management, the design team determined what costs had to be to charge the target price.

From this crucial calculation, all else followed.

To achieve target costs, the design team negotiated doggedly with all the company departments responsible for different aspects of the new product, and with outside suppliers of needed parts and materials.

HP(Hewlett-Packard) engineers designed a machine with fewer and simpler parts, manufacturing overhauled its factories to reduce production costs, and suppliers found ways to provide quality components at needed prices.

By meeting its target costs, HP(Hewlett-Packard) was able to set its target price and establish the desired price position. As a result, sales and profits soared.

Other companies give more emphasis on other marketing tools than price to create nonprice positions.

Often, the desired strategy is not to charge the lowest price. Instead, marketing offers are differentiated, which justify a higher price.

A company may set an initial price of $20,000 for its refrigerator, offering no post-sales service. Alternatively, it can make the initial price of the same refrigerator $22,000, offering 1-year free servicing.

Thus, the marketer must take into account the total marketing mix when setting prices. If the product is positioned on nonprice factors, then decisions about quality, promotion, and distribution will have a significant influence on price.

If the price is considered to be a more important positioning factor, then the price will have a significant bearing on decisions made about the other marketing-mix elements.

Therefore, it will be pragmatic for the companies to consider price and all the other marketing-mix elements when developing the marketing program.

3) Costs

Costs set the lowest level of the price below, which the company can not charge for its product. The company wants to charge a price that covers all of its costs for producing, distributing, and selling the product and brings a good return for its effort and risk.

A company’s costs may play an important role in its pricing strategy. Companies having lower costs can set lower prices, which generates greater sales and profits. Let’s we will discuss the different types of cost:

Types of Costs

A company’s costs are of two types, fixed and variable.

Fixed costs, also termed as overhead, are costs that do not vary with production or sales level. For example, a company must pay rent, heat, interest, and employee salaries regardless of its output.

Variable costs vary directly with the volume of production. Each TV set produced by Sony involves the cost of the picture tube, speaker, transformer, packaging, and other inputs. These costs tend to be the same for each unit produced. They are called variable costs because their total varies with the number of units produced.

Total costs are the sum of the fixed and variable costs for any given level of production. The producer wants to charge a price that will at least cover the total product costs at a given level of production.

The company must monitor its costs carefully. If the companies cost of production and sale are more than those of its competitors’, the company will have to charge a higher price or make less profit. Such a situation is disadvantageous from a competitive viewpoint.

In pricing prudently, producers should know that costs vary with different levels of production. Suppose a transistor radio manufacturer has a plant to manufacture 500 radio sets per day. It may find that cost per radio set is high if it produces only a few per day.

But as production moves up to 500 radio sets per day, the average cost falls.

This is because fixed costs are spread over more units, with each one bearing a smaller fixed cost. The manufacturer can try to produce more than 500 radio sets per day. Still, average costs will increase because the plant becomes inefficient due to various problems arising from overcapacity utilization.

If the manufacturer felt it could sell 1,000 radio sets a day, it should consider building a larger plant using more efficient machinery and work arrangements.

Eventually, the manufacturer may find that a 1,500 daily production plant is the best size to build if demand is adequate to support this level of production.

Costs also vary with the production experience gain by a producer.

Suppose a transistor radio manufacturer runs a plant that manufactures 1,500 radio sets per day. As the manufacturer gains experience in manufacturing radio sets, it learns how the better way of doing it.

Workers’ efficiency increases, work becomes better organized, and the manufacturer adopts better equipment and production processes.

With a higher volume of production, the manufacturer becomes more efficient and acquires economies of scale. Consequently, the average cost tends to fall with accumulated production experience.

4) Organizational Considerations

A company’s management must decide who should be given the responsibility of setting prices. Companies deal with pricing in several ways.

In small companies, prices usually are set by top management rather than by the marketing or sales departments.

In contrast, in large companies, pricing typically is handled by divisional or product line managers. In industrial markets, salespeople may be authorized to negotiate with customers within certain price ranges.

Even so, top management sets the pricing objectives and policies, and it often accepts the prices suggested by lower-level management or salespeople.

In industries where pricing is a basic factor, companies will organize a pricing department to set the best prices or assist others in setting them.

This department is accountable to the marketing department or top management. Others who can contribute to pricing include sales managers, production managers, finance managers, and accountants.

External Factors Affecting Pricing Decisions

Various factors affect the pricing decisions of a company.

- Market and Demand.

- Competition.

- Other Environmental Elements.

The influences of these factors can be stated as under:

1) The Market and Demand

While cost considerations set the lower limit of prices, the market demand sets the upper limit. Both consumer and industrial buyers weight the price of a product or service against the benefits of having it.

So, before setting prices, the marketer must appreciate the relationship between price and demand for its product.

The following discussion explains how the relationship between price and demand varies for different types of markets and examines how buyer perceptions of price affect the pricing decisions.

Methods for measuring the price demand relationship have also been discussed in this lesson.

Pricing in Different Types of Markets

The seller’s pricing considerations vary with different types of markets. Economists identify four types of markets, each posing a different pricing challenge.

In a situation of pure competition, the market consists of many buyers and sellers trading with a uniform commodity such as rice, steel, company shares.

No single buyer or seller has a significant influence on the going-market-price because buyers can procure as much as they need at the going price.

Nor the sellers ask for less than the market price because they can sell all they want at this price.

Its price and profits go up, and new sellers can easily enter the market. In a typical competitive market, marketing research, product development, pricing, advertising, and sales promotion play a negligible role. Thus, sellers in these markets do not put much emphasis on marketing strategy.

In a situation of monopolistic competition, the market consists of many buyers and sellers who transact over a range of prices rather than a single market price.

A range of prices prevails because sellers can differentiate their offers to buyers. The producer offers products with varied quality, features, or style. Even the accompanying services are also varied.

Buyers notice a difference in sellers’ products and are ready to pay different prices for them. Sellers tend to make differentiated offers for different customer types.

Besides, sellers use branding, advertising, and personal selling to make their offer distinctive.

As there operate many competitors, each firm is less affected by competitors’ marketing strategies than in oligopolistic markets.

In an oligopolistic situation, a few sellers operate in the market. They are highly reactive to each other’s pricing and marketing strategies. The product can be homogenous or heterogeneous.

The oligopolistic market consists of few sellers because new sellers find it quite hard to make their way into the market. Each seller monitors competitors’ strategies carefully.

If a company reduces its price, buyers will quickly switch to its products. The other companies must react by lowering their prices or increasing their services. In an oligopoly, a firm is never sure that it will achieve anything permanent through price reduction.

Reversely, if a firm raises its price, its competitors might not follow suit, and the firm would have to cancel its price increase or risk losing customers to competitors.

In a situation of pure monopoly, the market consists of one seller. The seller may be a government monopoly, a private regulated monopoly, or a private nonregulated monopoly.

Pricing is dealt with separately in each. A government monopoly can have various pricing objectives. It might set a price below cost because the product is needed by buyers who cannot pay for the full cost.

The price might be set either to cover costs or to generate handsome revenue. It can be set quite high to reduce consumption.

In a regulated monopoly, the government allows the company to set rates that will bring a fair return, which will enable the company to maintain and expand its operations as required. Nonregulated monopolies have the freedom to set prices at what the market will bear.

In practice, they do not always charge the full price for various reasons, such as reluctance to attract competitors, plan to enter the market faster with a low price, or apprehension of government regulation.

Consumer Perceptions of Price and Value

When setting a price, the company must consider consumer perceptions of price and how these perceptions influence consumers’ purchase decisions.

Pricing decisions, like other marketing-mix decisions, must center around the buyer. When consumers buy a product, they pay the price in exchange for the benefits of having or using the product.

Buyer- oriented pricing demand recognizing how much value consumers place on the benefits they received from the product and setting a price that equals this value. These benefits can be actual or perceived.

For example, estimating the cost of a food item in a restaurant is relatively easy. While determining the value of other satisfactions such as taste, environment, and conversation is very difficult.

Also, these values will vary both for different consumers and different situations.

Marketers often find it difficult to measure the values customers will attach to their products. But the consumers consider these values to evaluate a product’s price.

When customers perceive that the price is higher than the product’s value, they do not buy the product; when customers perceive that the price is smaller than the product’s value, they buy it, and the seller loses profits.

So, the marketers must try to identify the consumer’s reasons for buying the product and set the price according to consumers’ perceptions of the product’s value. Because consumers differ in the values, they attach to different product features. Marketers often adopt varying pricing strategies for different segments.

They offer different sets of product features at varying prices.

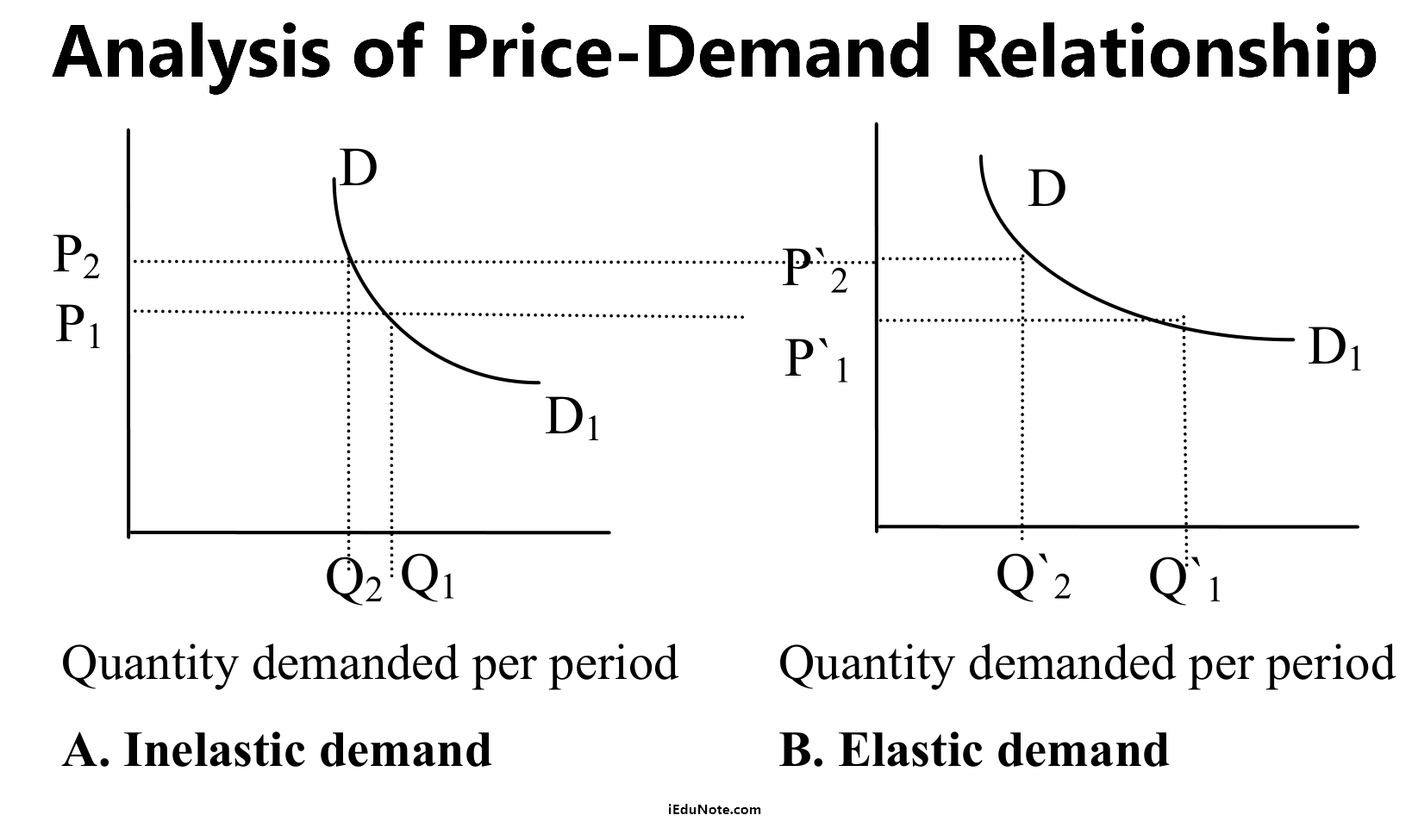

Analysis of Price-Demand Relationship

Each price the firm might charge will lead to a different level of demand. The relationship between the price charged and the consequent quantity demanded ‘is shown in the demand curve.

The demand curve shows the number of units the market will buy at different prices charged in a given time. Normally, demand and price are inversely related. The higher the price, the lower the demand.

Thus, the firm would sell less if it increased its price from p1 to p2. To sum up, consumers with limited budgets generally will buy less of a commodity if its price is exorbitant.

In the case of goods having prestige value, the demand curve sometimes slopes upward.

For example, a sunglass manufacturing firm found that by raising its price, it sold more sunglasses rather than less. Consumers thought the higher price meant a better or more desirable sunglass.

However, if the firm charges too high a price, the level of demand will be lower.

Most firms measure their demand curves by estimating demand at different prices. The type of market is responsible for varying demand levels at different prices.

In a monopoly, the demand curve indicates the total market demand resulting from different prices. If the firm faces competition, its demand from different prices will depend on whether competitors’ prices remain constant or change or with the firm’s prices. Here, the assumption is that competitors’ prices stay constant.

Price Elasticity of Demand

It is also important for a marketer to understand price elasticity, which indicates how responsive demand will be to a change in price.

In the figure-A above; a price increase from P1 to P2 leads to a relatively small fall in demand from Q1 to Q2.

In figure-B above, however, the same price increase leads to a large fall in demand from Q’1 to Q’2. The demand is inelastic if it hardly changes with a small price change.

The demand is elastic if it changes greatly. The following formula gives the price elasticity of demand:

| Price Elasticity of Demand = % Change in Quantity Demanded / % Change in Price |

Suppose demand falls by 15 percent when a seller raises the price by 5 percent. Price elasticity of demand is therefore 3 a demand is elastic. If demand falls by 5 percent with a 5 percent increase in price, then elasticity is 1. In this case, the seller’s total revenue remains the same.

The seller sells fewer items but at a higher price that keeps the total revenue the same. If demand falls by 1 percent when the price increases by 2 percent, then elasticity is -1/2, and demand is inelastic. The less elastic the demand, the more it is rewarding for the seller to raise the price.

Several factors determine the price elasticity of demand.

Buyers are less responsive to price when the product is unique, high in quality, prestige, or exclusiveness. Buyers are also less price-sensitive when substitute products are rare, and their quality can not be compared.

Finally, buyers are less price-sensitive when disposable income for buying the product is less relative to their total income or when the buyer alone does not bear the cost.

If demand is elastic rather than inelastic, sellers will decide on lowering their prices. A lower price will generate total revenue.

This practice can be considered wise as long as the extra costs of producing and selling more do not exceed the extra revenue.

2) Competition

Another important external factor affecting the firm’s pricing decisions is competitors’ costs and prices and probable competitor responses to its own pricing decisions.

A consumer who is contemplating buying a National micro oven will compare National’s price and value against the prices and values of micro ovens of Sharp, Toshiba, Sanyo, and others.

Moreover, a firm’s pricing strategy may affect the nature of the competition it meets. If national follows a high-price, high-margin strategy, it may invite the competition.

Reversely, a low-price, low-margin strategy may weaken competitors or eliminate them from the market.

A firm needs to benchmark its costs against its competitors’ costs to ascertain whether it operates at a cost advantage or disadvantage. It also should know the price and quality of each competitor’s offer.

This can be done in several ways. The firm can send out shoppers to compare to price and compare the product of its competitors.

It can obtain competitors’ price lists and buy competitors’ products. It can ask the opinion of the buyers about the price and quality of each competitor’s product.

Knowing the competitors’ prices and offers, a firm can use them as a starting point for its pricing.

If National’s micro ovens are similar to Toshiba’s, it will have to price close to Toshiba or lose sales. If National’s micro overs are not as good as Toshiba’s, the firm will not charge as much.

It National’s micro ovens are better than Toshiba’s, it can charge more. The National will use price to position its offer relative to the competitors’ price.

3) Environmental Elements

A firm must also consider other elements of its external environment while setting the price. A country’s economic milieu can have a strong impact on the firm’s pricing strategies.

Economic factors such as boom or recession, inflation, and interest rates influence pricing decisions because they affect both production costs and consumer perceptions of its price and value.

The firm also must consider the likely impact of its price on other parties in its environment. The firm should set prices that give intermediaries a reasonable profit, stimulate their support, and assist them in selling the product effectively. The government may also influence pricing decisions.

Finally, social concerns also deserve attention. In setting price, a firm’s short-term sales, market share, and profit goals may have to be subordinated to broader societal interests.