Auditor’s Certificate

An Auditor’s certificate is a confirmation of the accuracy of the facts relating to the accounts for a particular time or to a specific matter.

D. Audit Planing and Reporting – iedunote.com

An Auditor’s certificate is a confirmation of the accuracy of the facts relating to the accounts for a particular time or to a specific matter.

Discover the meaning, advantages, and types of cost audit. Learn how cost audits improve management decisions and benefit shareholders and society.

Materiality is a concept within auditing and accounting relating to the importance and significance of an amount, transaction, or discrepancy.

Auditor’s 3 responsibilities in completing the audit involve; completing the fieldwork, evaluating the findings, and communicating with the client.

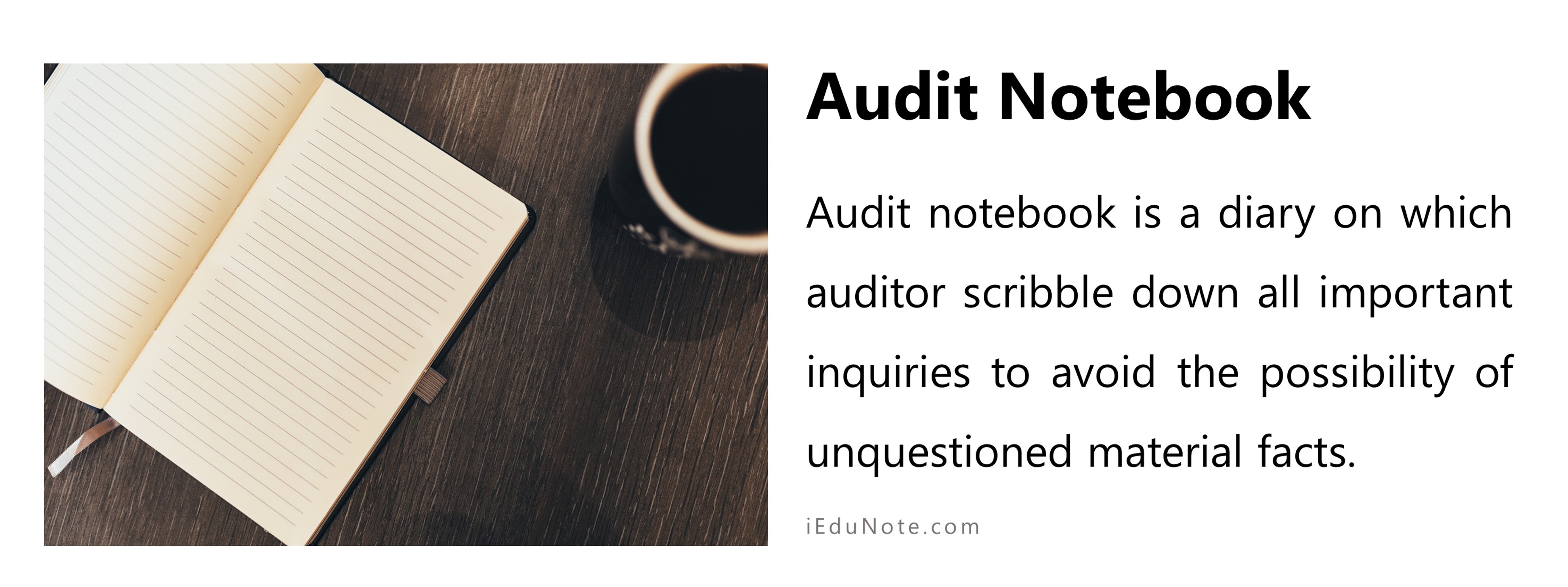

Audit Notebook is a diary for auditors to record observations, errors, doubtful queries, explanations, and clarifications to be received from the clients.

Professional ethics is the professionally accepted standards of personal and business behavior, values, and guiding principles.

An audit report is the auditor’s written opinion explaining if the financial statements are free of material misstatements and presented correctly.

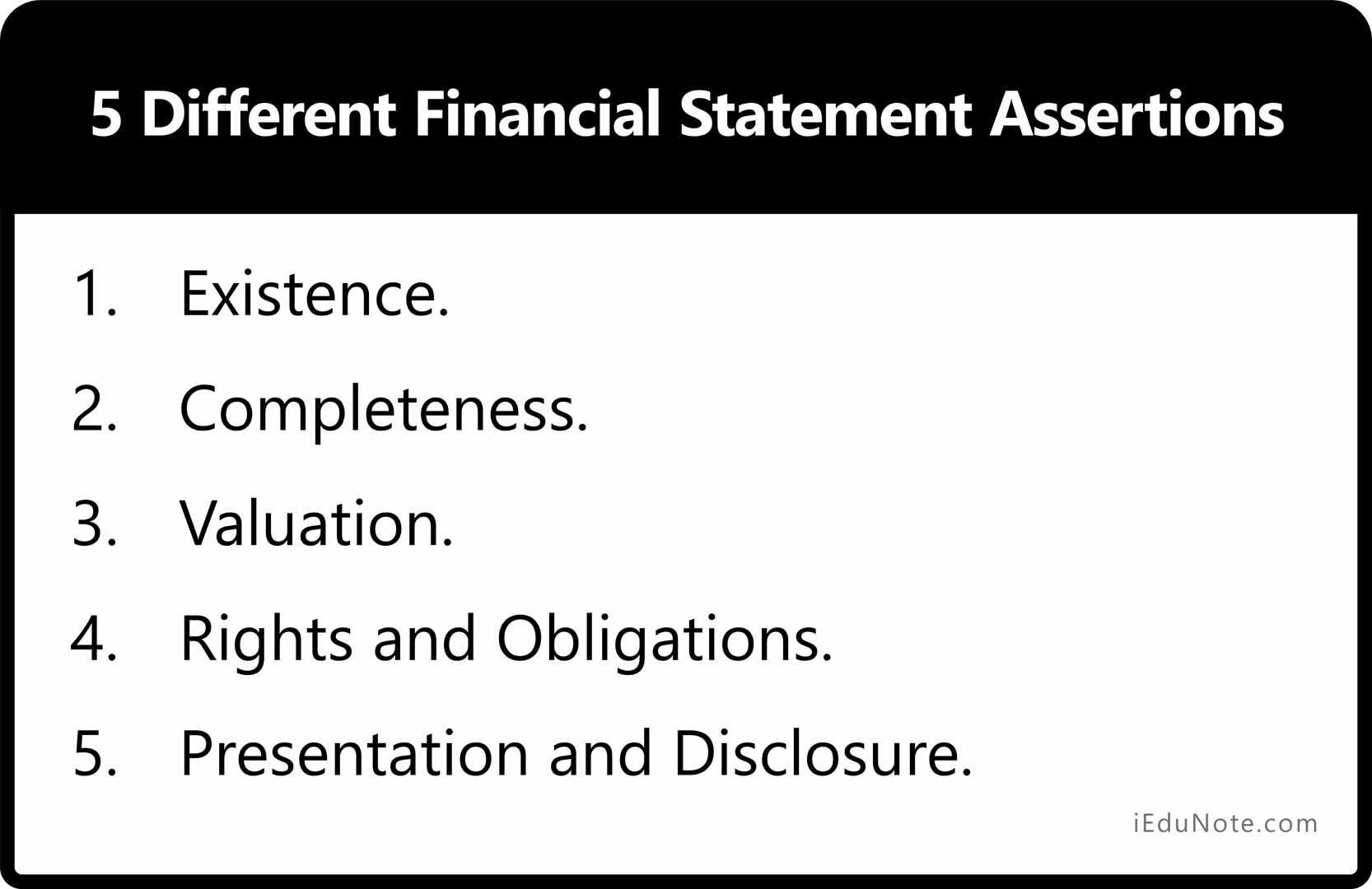

Learn five key financial statement assertions in auditing: existence, completeness, valuation, rights and obligations, and presentation and disclosure.

The audit risk is the risk that the auditor will not discern errors or intentional miscalculations while reviewing the company’s financial statements.

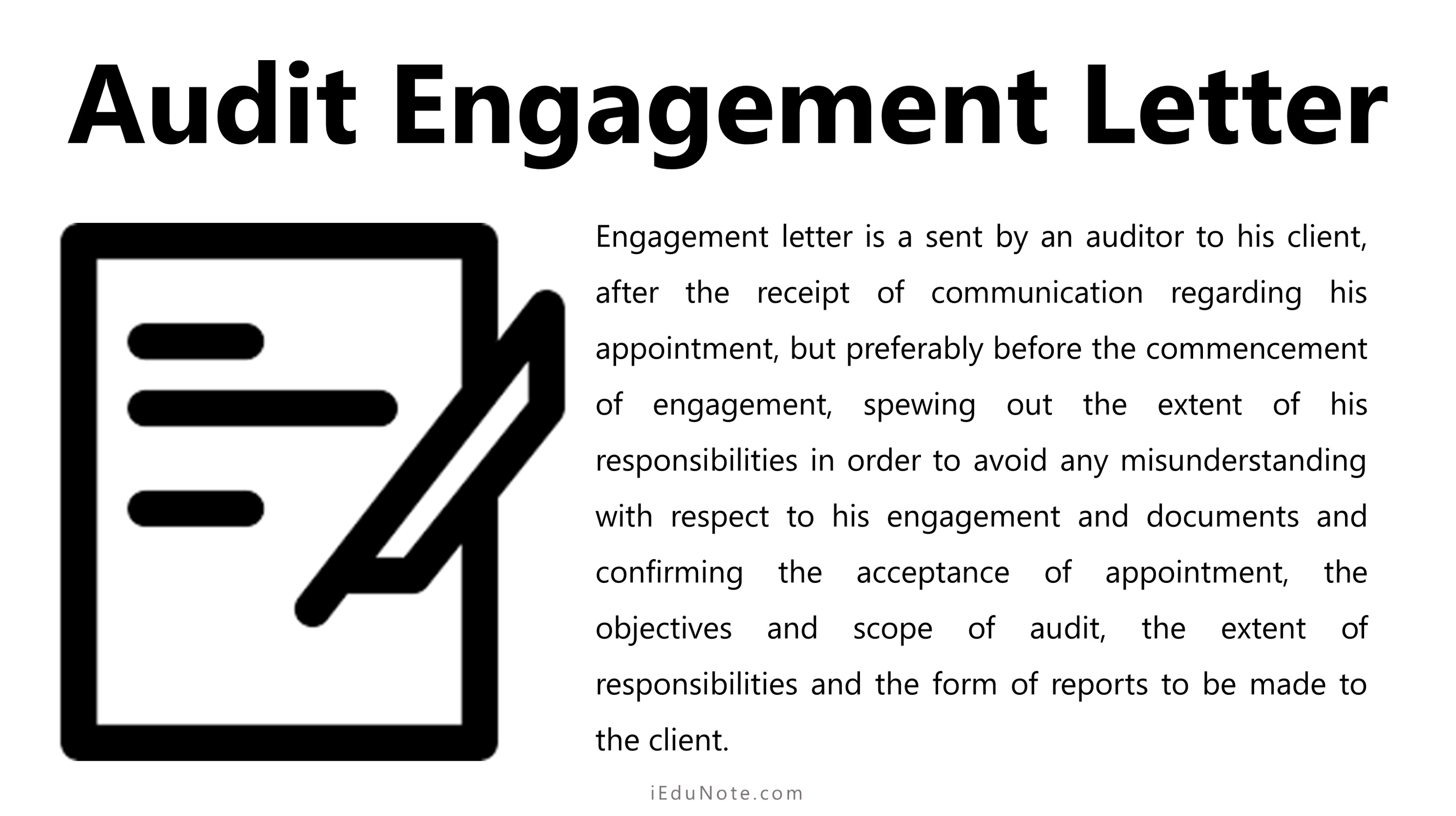

The audit engagement letter confirms the auditor’s acceptance of the audit and includes the responsibilities’ objective, scope, and extent of the audit.

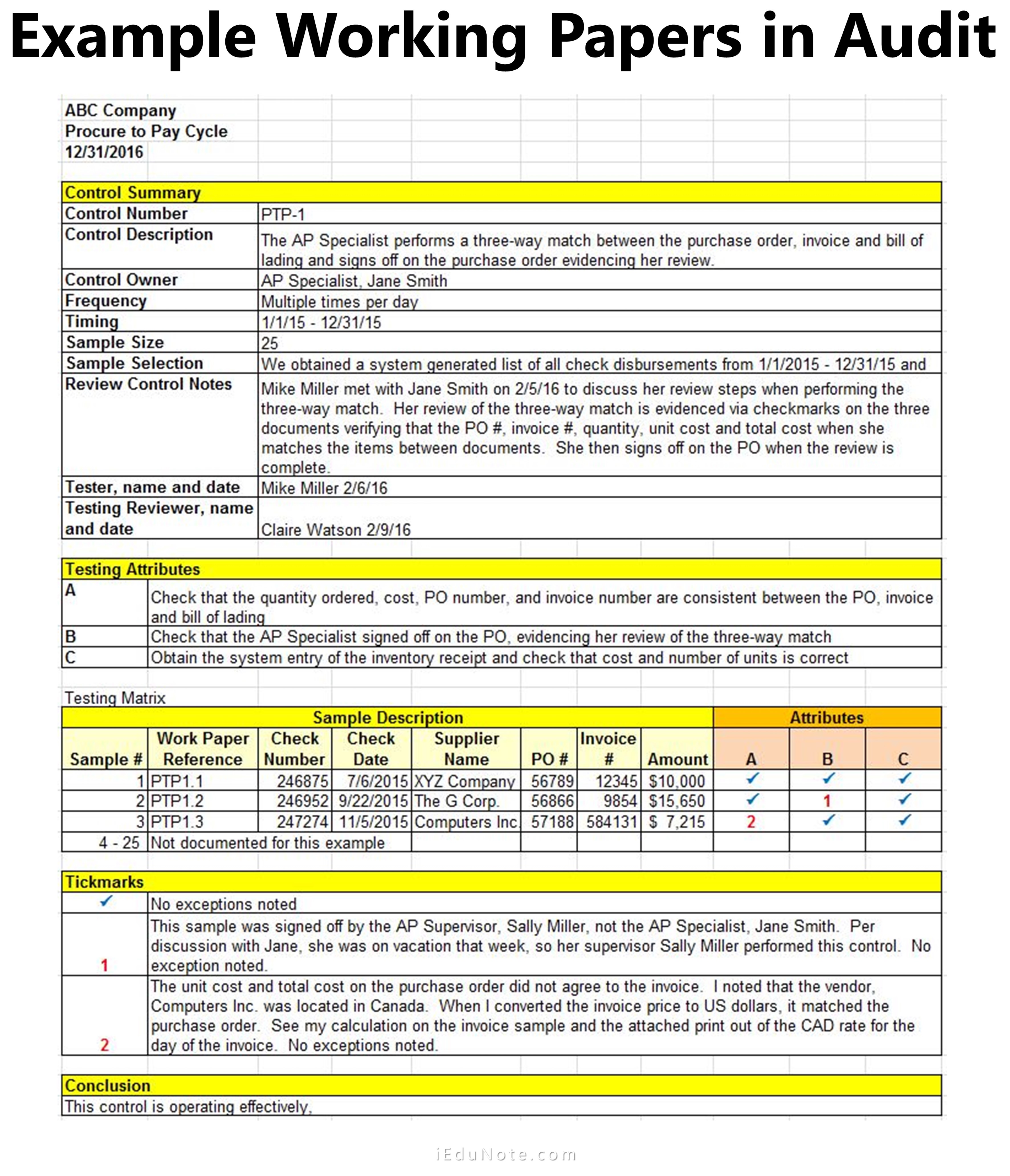

Audit working papers are essential records of evidence supporting auditing, ensuring adherence to relevant standards.

Understand ethics: its meaning, importance, and ethical dilemmas. Unveil the framework for making ethical choices and resolving moral conflicts effectively.

An audit program is a set of policies and procedures to perform and verify the auditing work to evaluate a business’s financial statements.

Learn Management Assertions in Auditing. Explore classifications, transaction-level assertions, and the role of auditors in financial verification.

An audit plan is a detailed strategy that sets the nature, timing, scope, and boundaries for the auditor to carry out the entire audit procedure.

Audit evidence is all the information collected and used by the auditor in the audit to arrive at a conclusion and provide an audit opinion.

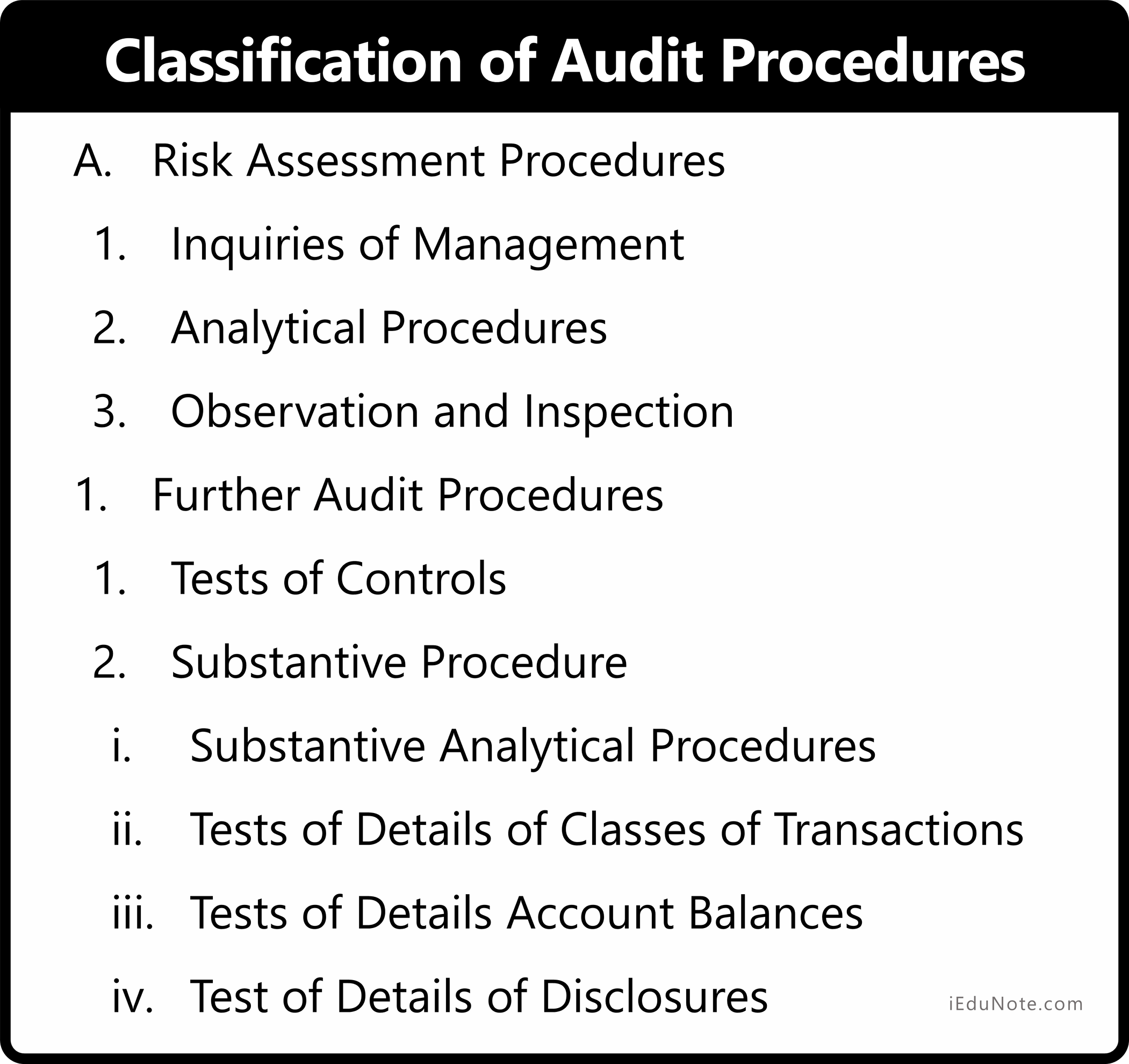

Audit procedures are the auditor’s methods or techniques to observe, gather, evaluate and verify the audit evidence for the audit.

Two types of events after the end of the reporting period in an audit are; adjusting events, and non-adjusting events.