Auditor’s Certificate

An Auditor’s certificate is a confirmation of the accuracy of the facts relating to the accounts for a particular time or to a specific matter.

An audit is a thorough review of an organization’s financial records to ensure accuracy and compliance with laws. Auditors help identify risks, improve controls, and enhance efficiency by assessing financial health and understanding assets, liabilities, losses, and profits.

Learn about different types of audits (external, internal, government) and the skills auditors use, such as critical thinking and problem-solving.

An Auditor’s certificate is a confirmation of the accuracy of the facts relating to the accounts for a particular time or to a specific matter.

Discover the meaning, advantages, and types of cost audit. Learn how cost audits improve management decisions and benefit shareholders and society.

Materiality is a concept within auditing and accounting relating to the importance and significance of an amount, transaction, or discrepancy.

3 primary types of audits are; (1) financial audit, (2) operational audit, and (3) compliance audit. Based on the task, there are 11 types of audits.

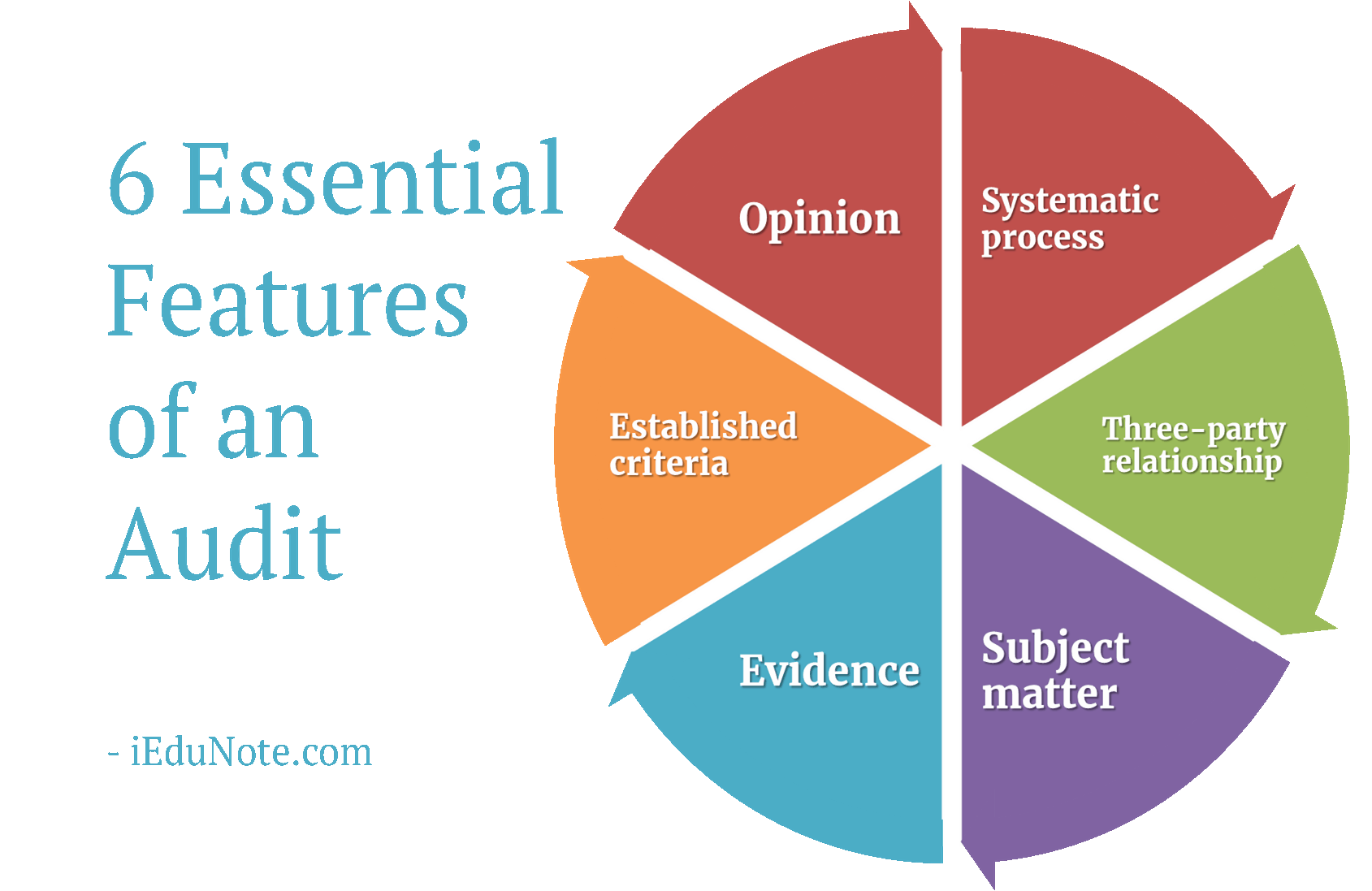

Discover the 6 Essential Features of an audit that Safeguard Financial Standing. Get Professional Insights and Expert Opinions.

A financial statement audit examines the financial statements to assess the correctness of financial statements and related disclosures.

Unlocking the Audit Scope: Discover the range of activities and records examined in an audit. Ensure compliance and gain valuable insights.

An internal check is a continuous process of the accounting system to check for errors or fraud in bookkeeping operations for early detection and prevention.

Auditor’s 3 responsibilities in completing the audit involve; completing the fieldwork, evaluating the findings, and communicating with the client.

Audit Notebook is a diary for auditors to record observations, errors, doubtful queries, explanations, and clarifications to be received from the clients.

Professional ethics is the professionally accepted standards of personal and business behavior, values, and guiding principles.

Detection risk is that material misstatements in financial statements through substantive tests and analysis will escape the auditor’s procedures.

An audit report is the auditor’s written opinion explaining if the financial statements are free of material misstatements and presented correctly.

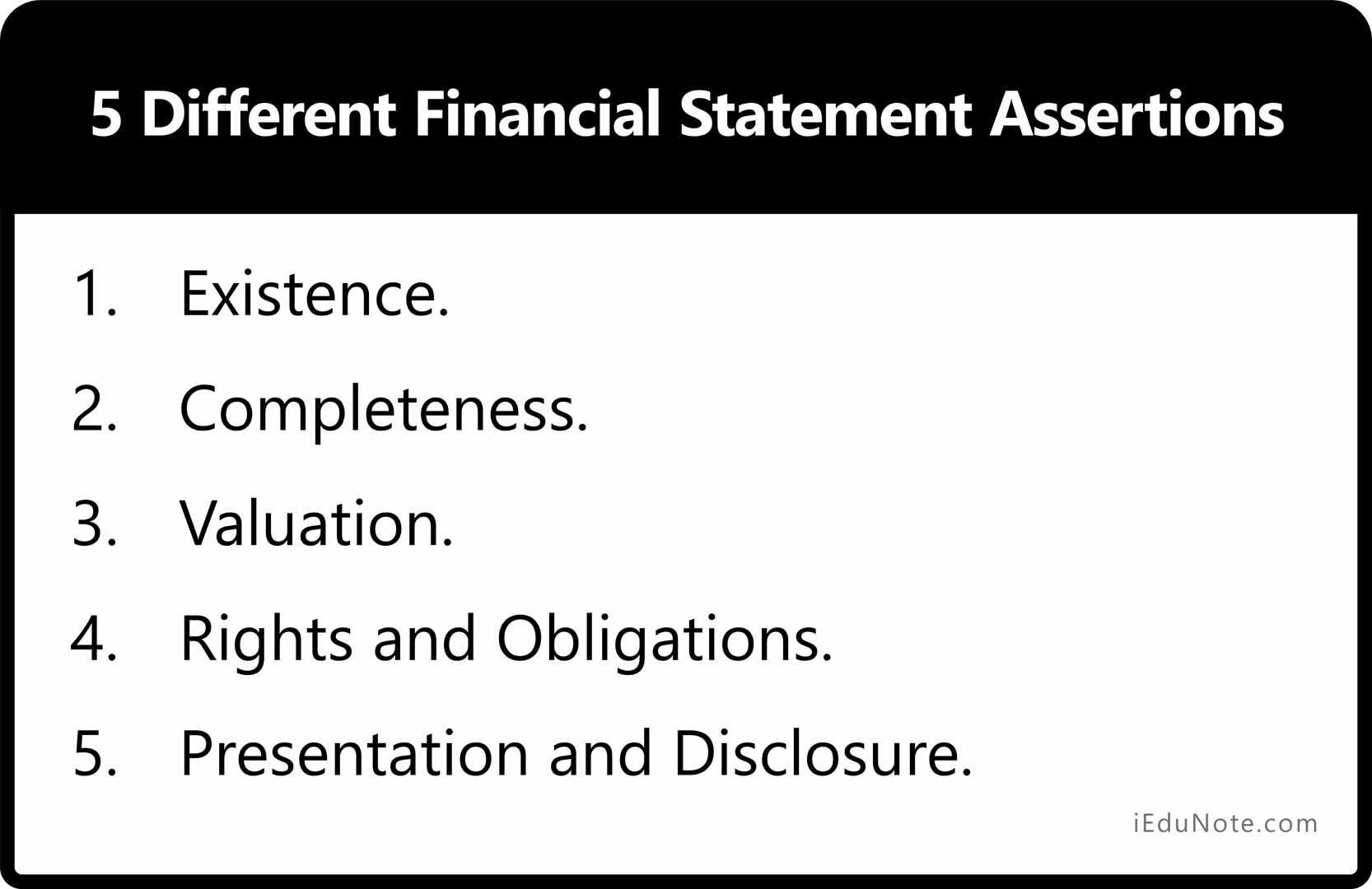

Learn five key financial statement assertions in auditing: existence, completeness, valuation, rights and obligations, and presentation and disclosure.

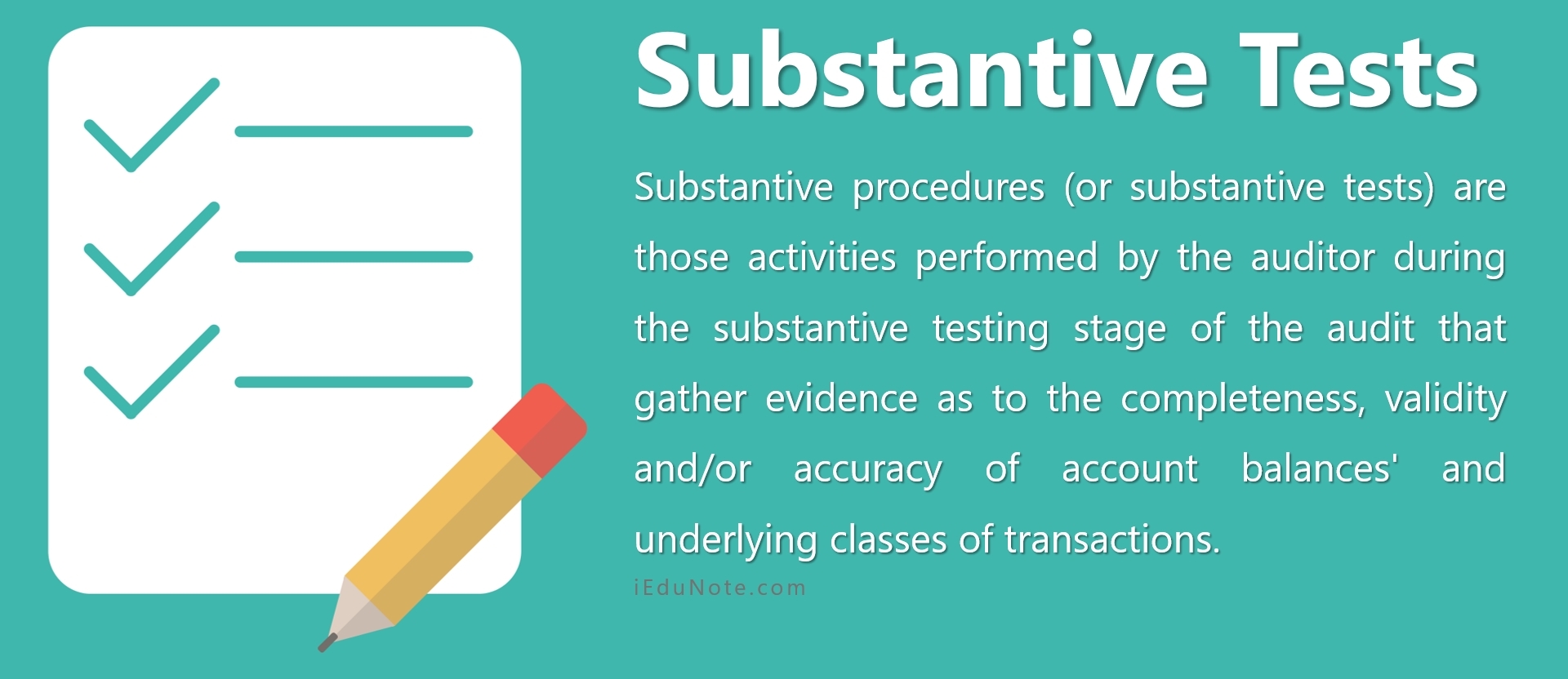

The substantive test is the process of obtaining audit evidence and checking the accounting system’s completeness, accuracy, and validity of data.

Discover the meaning and impact of the audit expectation gap. Learn how auditors and users can align their expectations for reliable financial statements.

The audit risk is the risk that the auditor will not discern errors or intentional miscalculations while reviewing the company’s financial statements.

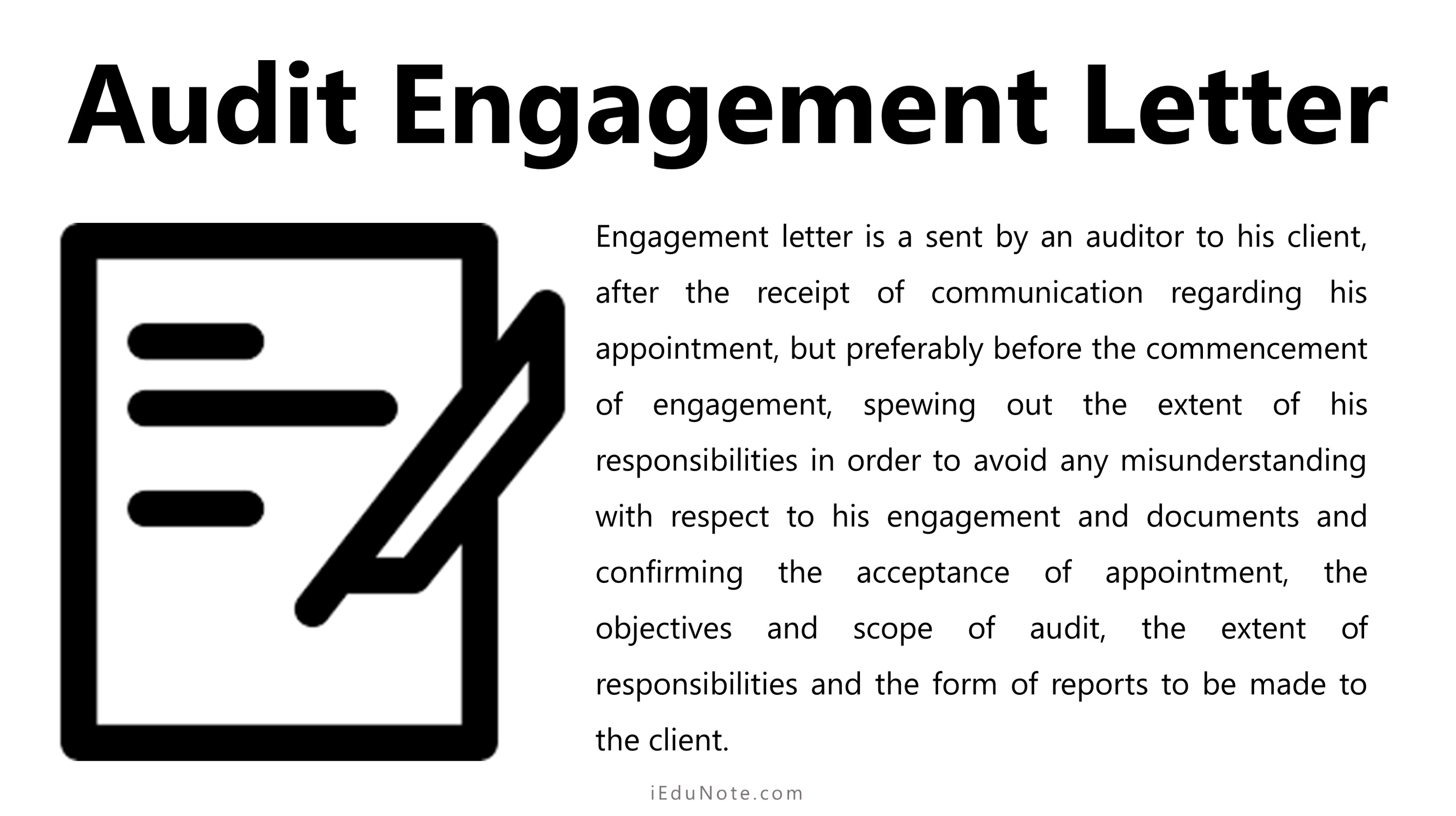

The audit engagement letter confirms the auditor’s acceptance of the audit and includes the responsibilities’ objective, scope, and extent of the audit.

Internal audit is the independent appraisal of an organization’s activity for critically reviewing accounting, financial, and other business practices.

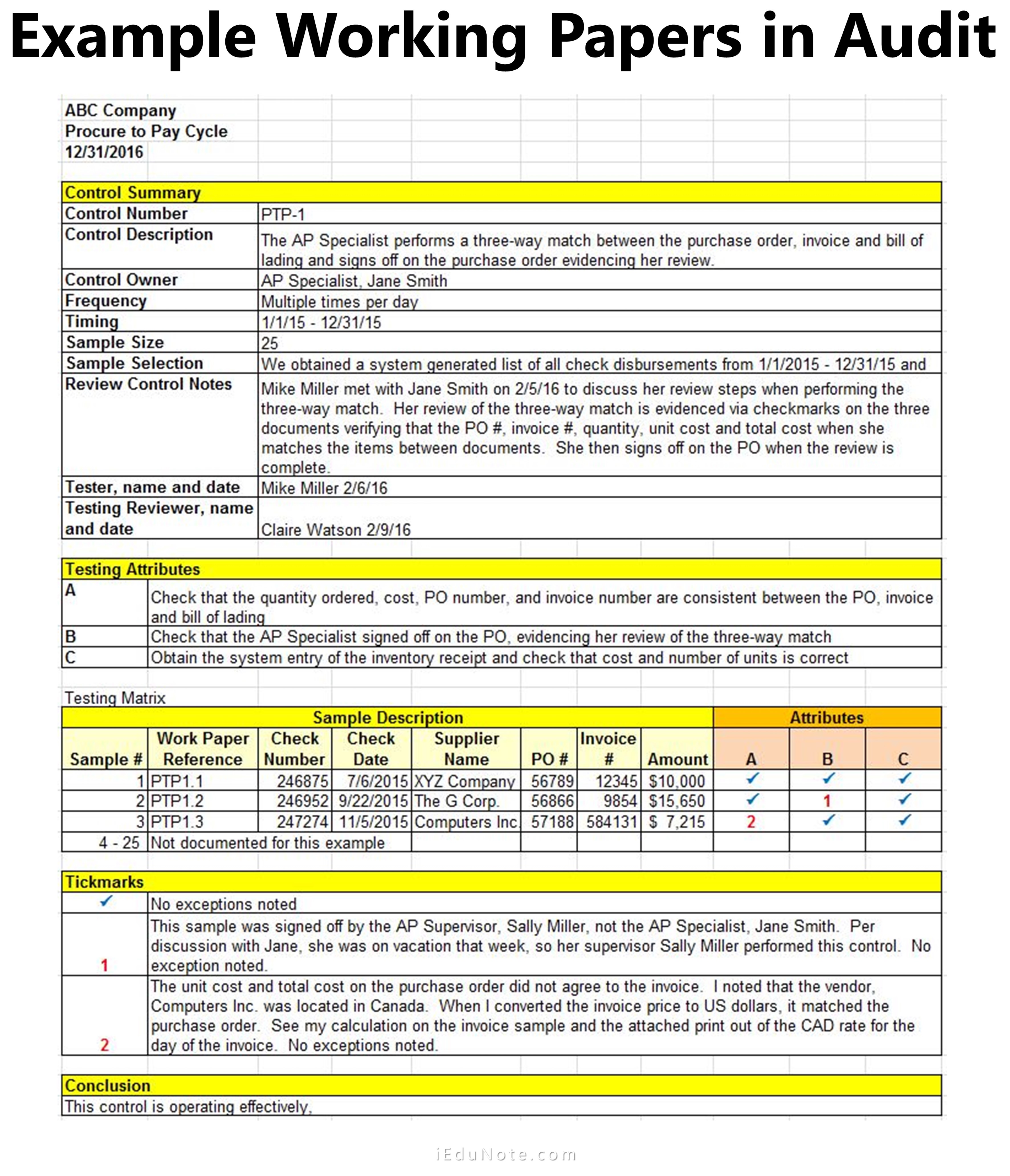

Audit working papers are essential records of evidence supporting auditing, ensuring adherence to relevant standards.

Control risk is the material misstatement in the accounting process that won’t be detected, prevented, or corrected by the internal control systems.

Understand ethics: its meaning, importance, and ethical dilemmas. Unveil the framework for making ethical choices and resolving moral conflicts effectively.

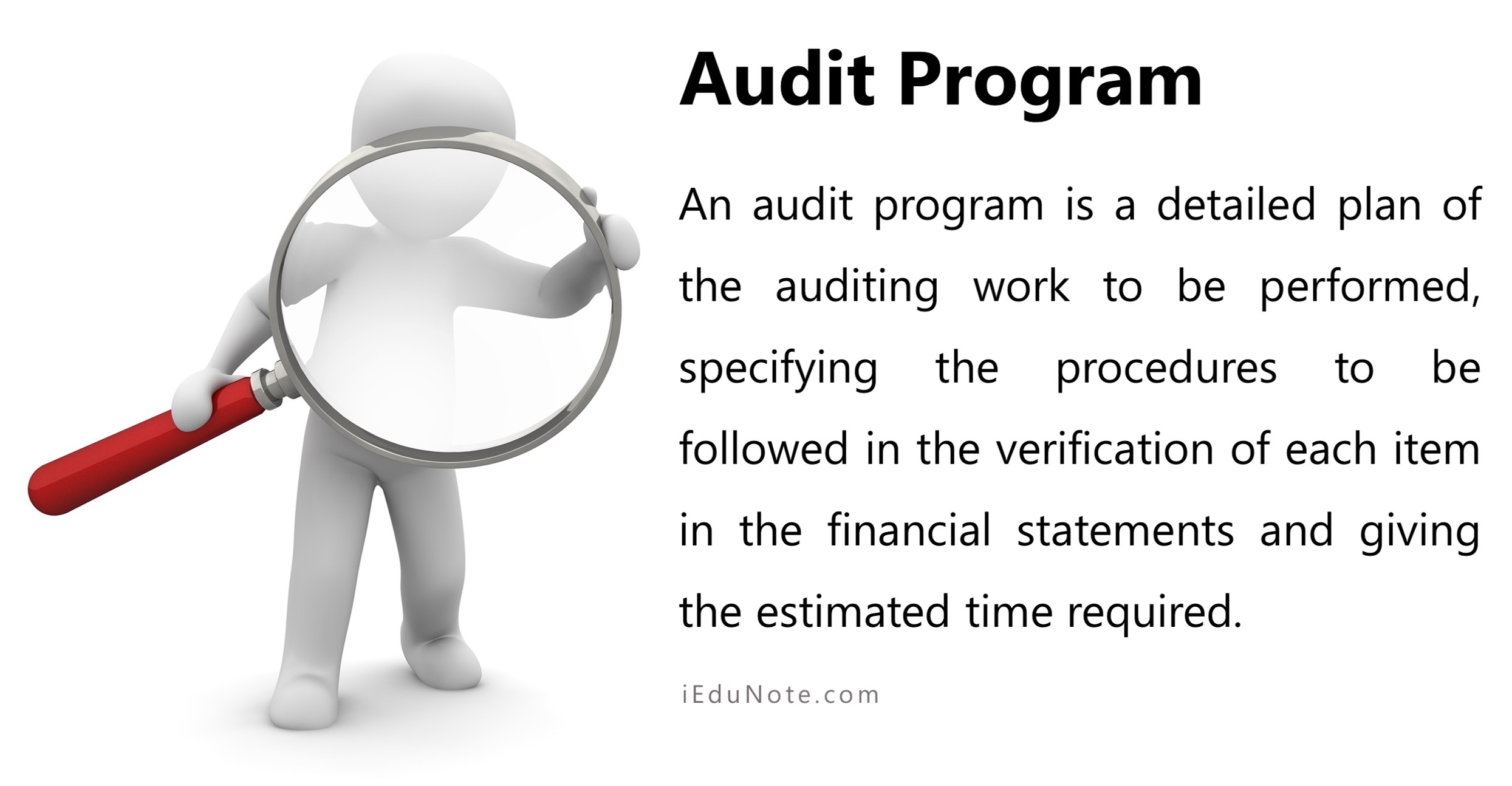

An audit program is a set of policies and procedures to perform and verify the auditing work to evaluate a business’s financial statements.

Learn Management Assertions in Auditing. Explore classifications, transaction-level assertions, and the role of auditors in financial verification.

An audit plan is a detailed strategy that sets the nature, timing, scope, and boundaries for the auditor to carry out the entire audit procedure.

Tests of Controls in audit test how effectively the operation runs compared to the controls (standards) set in the organization.

Audit evidence is all the information collected and used by the auditor in the audit to arrive at a conclusion and provide an audit opinion.

Get professional CPA services for audits, tax planning, business consulting, internal control, and more. Trust the expertise of certified public accountants.

Discover the fascinating origin and evolution of auditing as a financial accountability tool. Explore its historical significance and role in fraud prevention.

Internal control is designed and implemented to address identified business risks that threaten the achievement of any of these objectives.

An audit is an examination and verification of a company’s financial documents by an independent professional against established criteria.

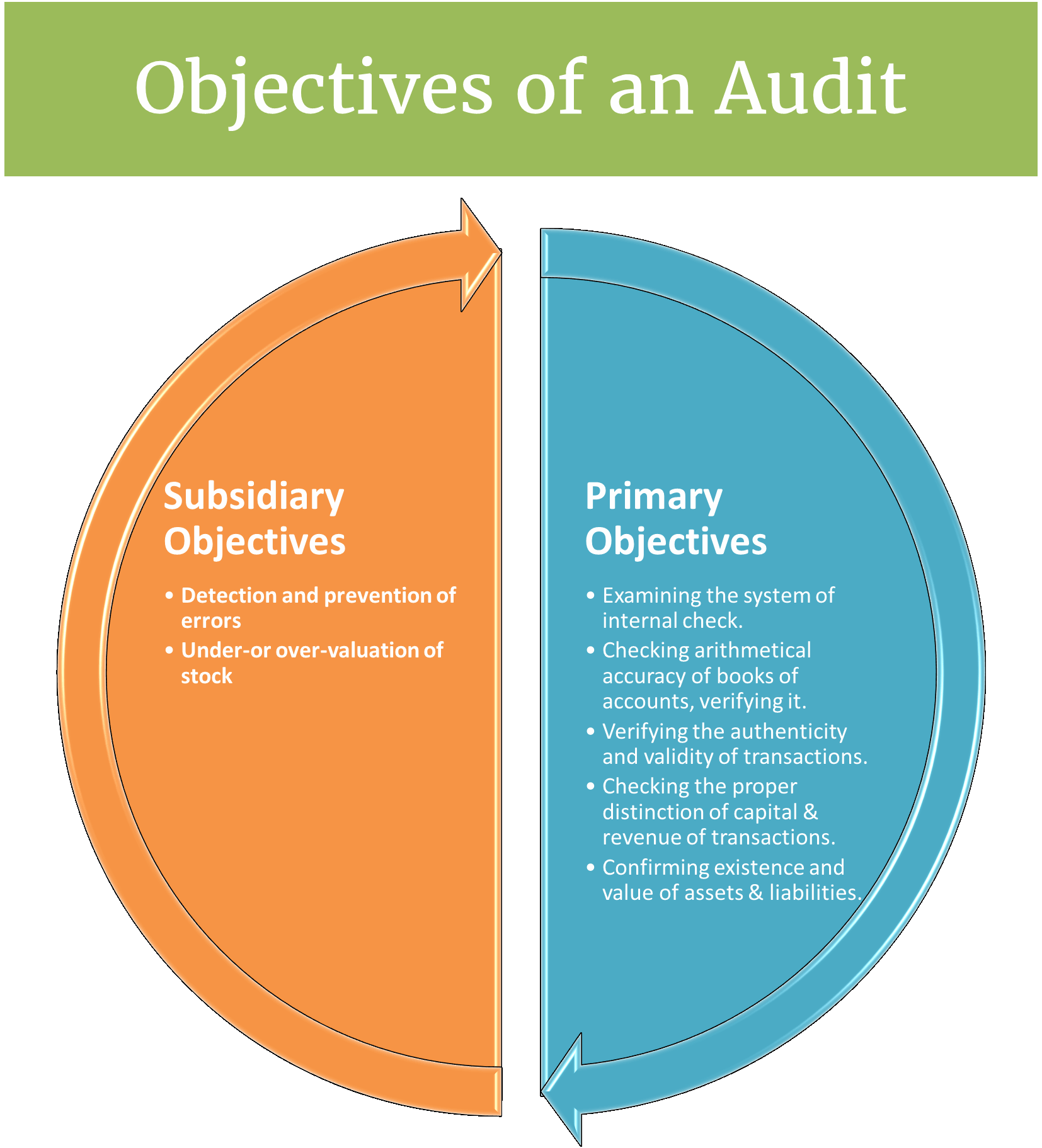

Unveiling audit objectives: verifying financial accuracy, detecting fraud, and ensuring compliance.