Reserves of the bank can be of two types: primary reserve and secondary reserve. The primary reserve usually ensures liquidity only apart from complying with legal requirements and does not contribute to profit earning. Secondary reserve contributes to a small part of profit earnings besides fulfilling the day-to-day liquidity requirement.

Understand Bank Reserve Management

What is Bank Reserve Management?

Reserve management is an important aspect of the daily activities of commercial banks. Primary reserve constitutes a certain portion of cash in hand, current deposits in the central bank, or other sister banks.

Short-term loans, treasury bills, short-term debentures, etc., are secondary reserve assets. The primary reserve serves two purposes: compliance with regulatory instructions and the other is meeting a part of the liquidity needs.

The secondary reserve also serves two purposes: meeting wide liquidity needs and earning a profit, however small it may be.

The primary and secondary reserves are always affected by internal and external factors. The bankers’ professionalism, skill, and experience can calculative manipulate the reserves to the best benefit of the bank.

The commercial bank operates its business based on the collected deposits. Maintaining adequate liquidity is indispensable to gratify the depositors’ timely demand for withdrawal. Considering this inevitability, bank regulatory authorities adopt different reserve management strategies.

Authorized officers of banks put most of their daily duties into maintaining statutory reserve in the central bank according to the daily fund position of the bank.

On the other hand, besides providing cash for meeting liquidity needs, the secondary reserve can be kept for profit in the form of short-term assets, which can be converted into cash within short notice and with insignificant or no loss of the capital sum of the securities held for the purpose.

The reserve amount can be increased or decreased by controlling and managing the daily cash or near-cash reserve.

What is Reserve?

The portion of the deposit that commercial banks must maintain in the central bank as per statutory requirements is generally called reserve. As stated earlier, this reserve is kept in cash or equivalent cash assets to maintain the liquidity of commercial banks.

A portion of the bank’s fund has been set aside to assure its ability to meet its liabilities to depositors in cash. Minimum reserves are to be maintained against demand, and time deposits are usually specialized banking laws.

The central bank can issue a circular, and thus it can increase or decrease the reserve rate/ratio as it thinks fit for the economy at a particular point in time. If the central bank increases this rate, commercial banks have to maintain more resources in reserve, whether in cash or near cash assets.

At this, the cash amount available to commercial banks will shrink. But when the central bank adopts the reverse action. It decreases the rate, cash amount available to commercial banks will increase, raising the loanable funds at the disposal of the banks.

It should be mentioned here that cash is a non-earning asset. Banks take cash from depositors and provide them an interest in return. So. it is not prudent for banks to keep a large amount of cash as a reserve.

As such, banks usually try to make at least a small amount of profit by investing the cash in easily convertible near cash assets. This type of investment also facilitates the banks to uphold goodwill by satisfying the liquidity requirement within short notice.

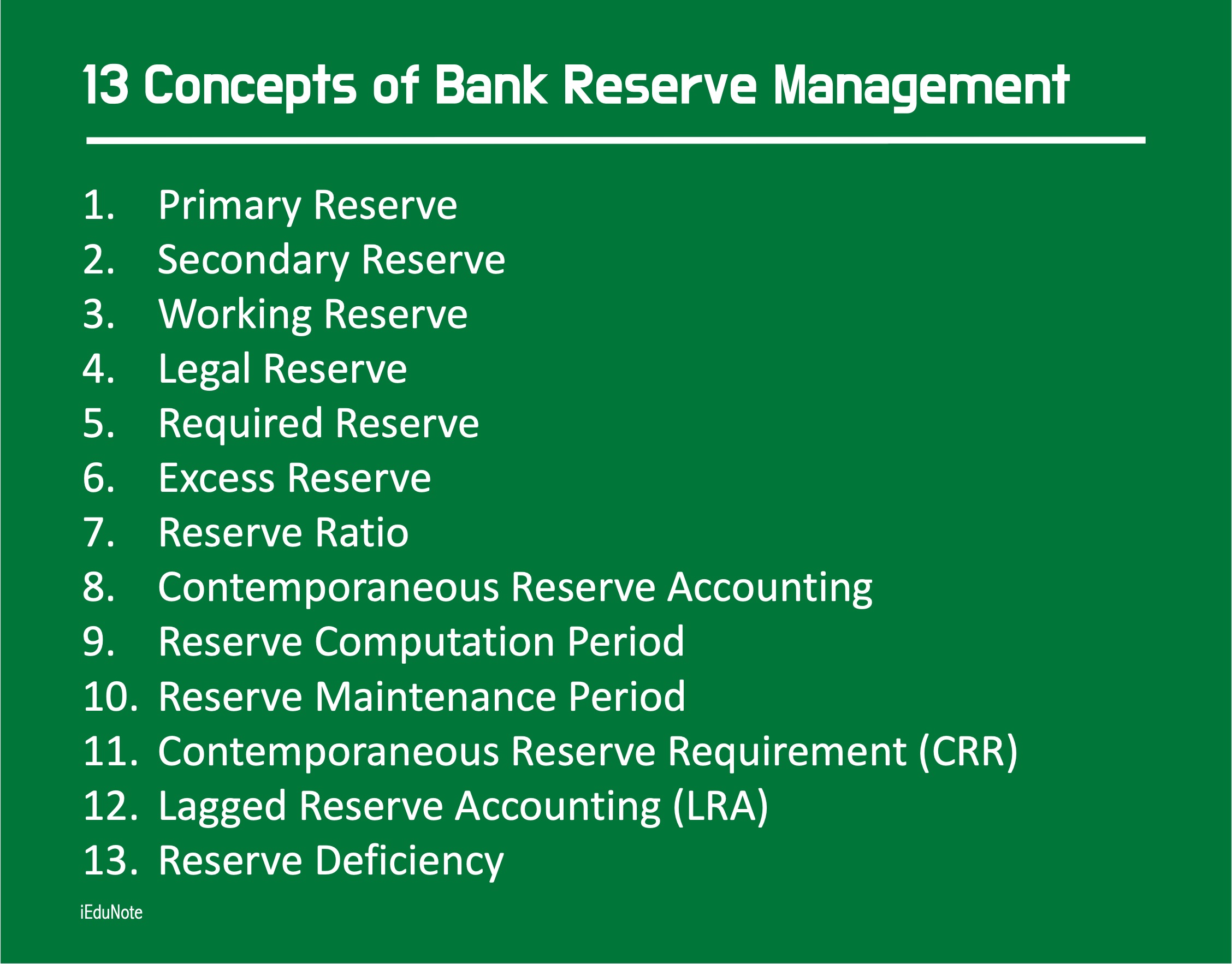

13 Concepts Relating To Bank Reserves

There are some frequently used concepts in reserve-related discussions. These are:

Primary Reserve

The primary reserve is that portion of deposits and other liabilities which is to be held in the central bank or the bank vault with the knowledge of the central bank.

Secondary Reserve

The secondary reserve is that portion of the deposits and liabilities which is to be held in the form of near-cash assets.

Working Reserve

Working reserve is that portion of the deposits and other liabilities that facilitate the bank’s daily operations.

Legal Reserve

The legal reserve is the assets that may be counted as reserves for purposes of meeting the central bank’s requirements.

Required Reserve

The required reserve is that portion of a bank’s legal reserves that must be held given the bank’s deposits and other liabilities along with the applicable central bank s reserve requirements.

The state superintendent of banking must maintain the liquid assets of chartered banks, and member banks must maintain by the Federal Reserve authorities.

Member banks must maintain their reserves most in deposits with their regional Federal Reserve Bank depending upon the type of deposits, time or demand, and central bank reserve of the country bank.

In addition, certain still cash may be counted as part of the required reserves.

Excess Reserve

The excess reserve is that portion of a bank’s legal reserves above its required reserves.

A term used to design the number of funds held in reserve more than the minimum legal requirements, whether the funds are deposited in the Federal Reserve Bank in a bank approved as a depository or in the cash reserve carried within its own vault.

Reserve Ratio

That percentage of the bank’s deposits or other liabilities, which must be held in the form of legal reserves to meet the central bank’s requirements, is called the reserve ratio.

Contemporaneous Reserve Accounting

This is the system begun by the Federal Reserve in 1984 for calculating each bank’s legal reserve requirements. The reserve computation and reserve maintenance periods for transaction deposits overlap.

Reserve Computation Period

This is the period of time established by the Federal Reserve System for certain depository institutions. The average daily amount of various deposits is computed to determine each institution’s legal reserve requirements.

Reserve Maintenance Period

According to federal law and regulations, it is a period of time spanning two weeks. A bank must hold the average daily amount of legal reserve. It is required to hold behind its deposits and other reservable liabilities.

Contemporaneous Reserve Requirement (CRR)

CRR calculates reserve requirements based on deposits held during the same period.

Lagged Reserve Accounting (LRA)

LRA is the process where reserve requirements are based on deposits held in some previous time period.

Reserve Deficiency

When the reserves maintained are less than the required level is called reserve deficiency.

From the above discussion, it can be realized that reserves can be of two types;

- Primary Reserve.

- Secondary Reserve.

Factors Causing Change in the Reserve Accounts Balance in the Central Bank

Every commercial bank is required to keep a statutory reserve in the central bank. To calculate such reserve requirements, the central bank records daily incoming-outgoing transactions of each commercial operating bank at the end of each working day.

Such balance of the reserve account thus calculated is informed to the bank concerned. Some such transactions by commercial banks are performed under the central bank’s control, while others are not. That is, member banks have nothing to do with the transactions done through the central bank.

However, the type of transactions in the central bank causing changes in the reserve accounts balance of member banks are presented in the following figure: