A banker is a person who is doing banking activities or business. A banker is an officer of a bank. In a broad sense, a banker conducts the business of banking. A banker is a person who is doing banking activities or business. To continue providing the best banking services to the customers, the banker has some rights and obligations that must be implemented and followed. Let’s take a look at all the rights and obligations of bankers.

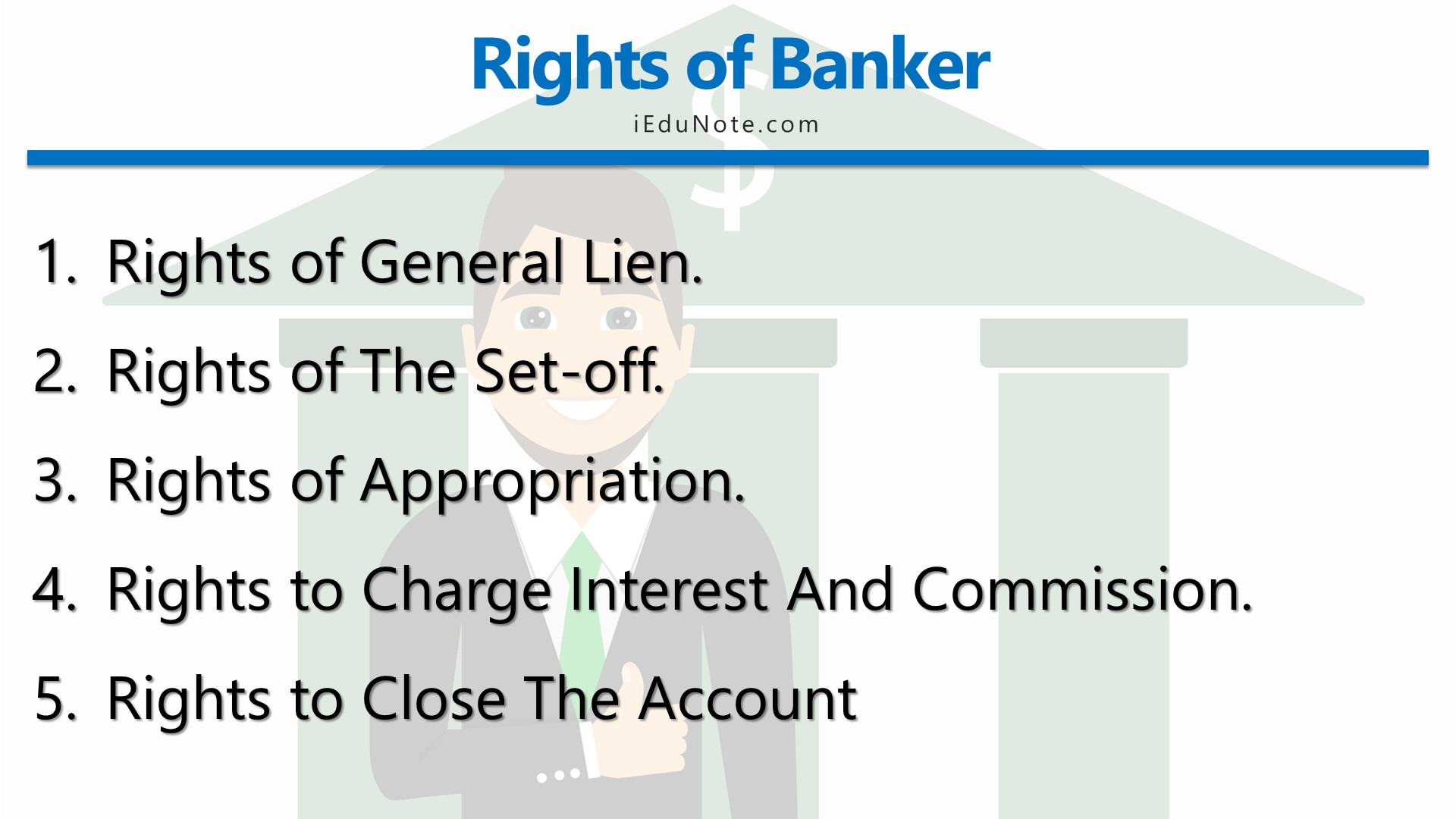

What are the 5 Rights of a Banker?

The rights of a banker that the banker can enjoy are as follows:

Rights of General Lien

One of the most important rights enjoyed by a bank is the right of a general lien.

Lien means the right of the creditor to retain the goods or securities owned by the debtor until the debt due from him is repaid. In other words, the lien is a right of a person to retain goods belonging to another; until the demands of the person in possession are satisfied.

There are some exceptional cases in which the right of a general lien is not applicable. These are:

- Safe custody deposit.

- Documents deposited for a special purpose.

- Security is held in trust.

The Right of the Set-off

Right of set-off is the right of a debtor to adjust the amount due to him from a creditor against the amount payable by him to the creditor to determine the net balance payable by one to another. Like any other debtor, a bank also has a right to set off.

When a customer has two or more accounts in the same name and capacity in a bank, the bank has the right to adjust the amount standing to the customer’s credit against the debit balance in the other account. The bank has a right to combine the two accounts.

A banker possesses the right of set-off, which enables him to combine two accounts in the same customer’s name and adjust the debit balance in one account with the credit balance in the other. The right of set-off can be exercised subject to the fulfillment of the following conditions:

- The accounts must be in the same name on the same right.

- The right can be exercised regarding debts due only, not regarding future debts or contingent debts.

- The number of debts must be certain.

- The banker may exercise that right at his discretion.

Banker’s Right of Appropriation

A customer may owe several distinct debts to the bank when the customer deposits some money without specific instructions, and it is insufficient to discharge all debts. The problem arises as to which debt this amount should be adjusted.

In the absence of any specific instructions, the bank has the right to appropriate the deposited amount to any loan, even to a time-barred debt. But the banker must inform the customer about the appropriation.

If the customer has more than one account or has taken more than one loan from the banker, the banker can appropriate these loans by the accounts.

Right to Charge Interest and Commission

The bank has the implied right to charge interest on loans and advances and charge commission for services rendered by the bank, such as SMS notification service, retail banking, multi-city cheque service, etc. The bank can debit such charges to the customer’s account.

As a creditor, a banker has the implied right to charge interest on the loans granted to the customer. In the same way, incidental charges like service charges, processing fees, appraisal charges, and panel charges may be imposed by the banker on the customer.

Deposits are repayable on the term and made by the customer. Still, the period of limitation for the refund of bank deposit is three years, with effect from the date a customer made a demand for his money.

Right to Close the Account

If the bank believes that an account is not being operated properly, it may close the account by sending a written intimation to the customer. But the notice is mandatory. A banker cannot close any customer’s account without sending such notice.

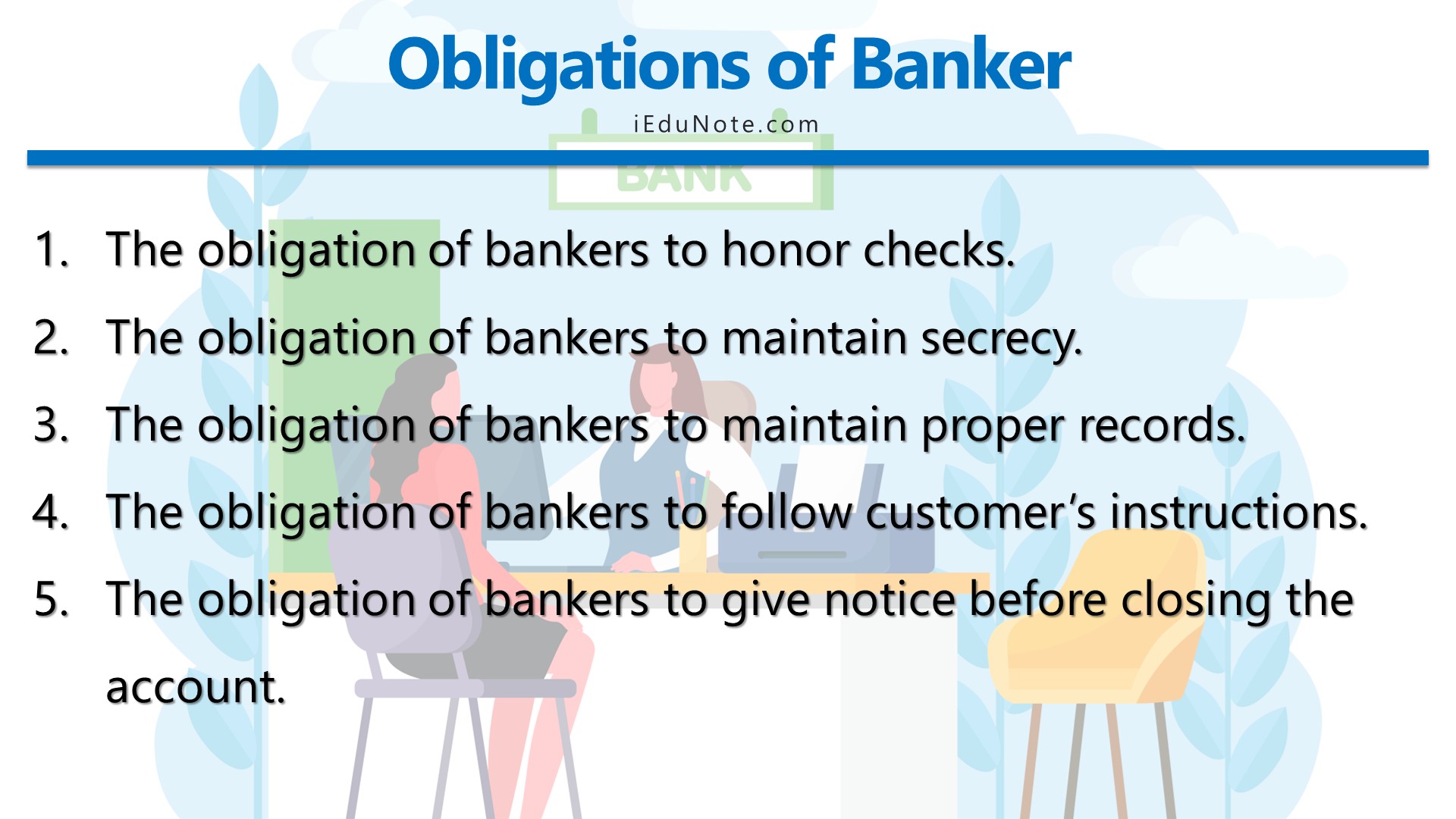

What are the Obligations of Bankers?

The relationship between the banker and customers creates some obligations on the part of a bank.

The obligation of Bankers to Honor Checks

The bank has a statutory obligation to honor the checks/cheques of its customers up to the amount standing to the credit of the customer’s account.

The obligation of bankers to Maintain Secrecy

The banker must not disclose to any outsider the details about the customer’s account, as such disclosures may adversely affect the credit and business of the customer.

The obligation of the Banker to Maintain Proper Records

The banker is obligated to maintain an accurate record of all the transactions(credits and debits) of the customers made with the bank.

The obligation of the Banker to Follow the Customer’s Instructions

The banker is legally obligated to follow the customer’s instructions. This is so because there is a contractual relationship between the bank and the customer.

The obligation of the Banker to give Notice before Closing the Account

If a banker wishes to close the customer’s account, it must give reasonable notice to this effect to the customer. Thus, a bank cannot close a customer’s account on its own wish because it may have serious consequences for the customer.